Strong and Simple regime

The PRA is expected to introduce a more proportionate prudential regime for less systemically important banks and building societies. This will be known as the ‘Strong and Simple’ regime.

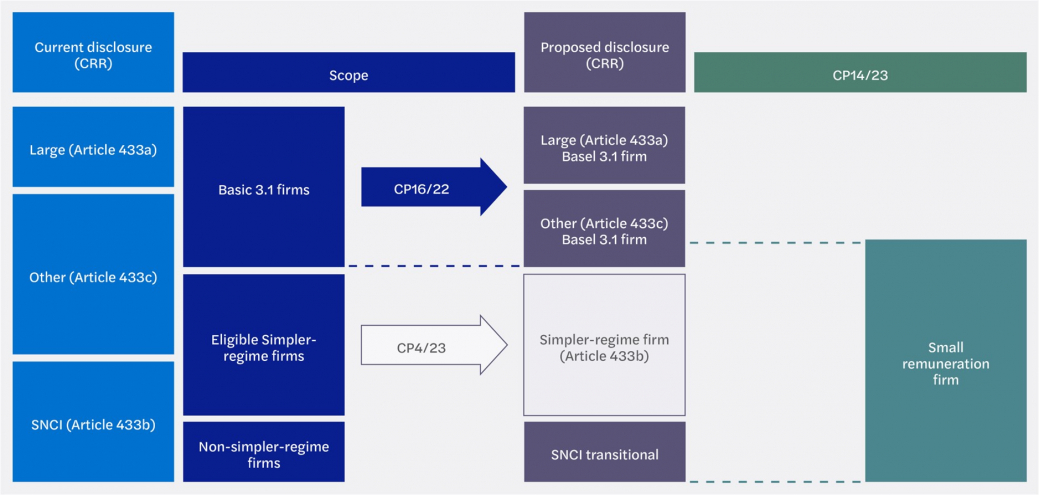

Pillar 3 Remuneration Disclosures (CP14/23 review)

Before the proposed changes by CP14/23, firms populated six templates: REMA and UK REM1 to UK REM5. These templates outlined the remuneration disclosures, including special payments and information for employees with a material impact on the institution’s risk profile and deferred remuneration.

The new changes, as outlined below, are expected to be published in the final policy on remuneration disclosures as part of the Strong and Simple framework in Q4 of 2023. The implementation date for these changes is expected in the second half of 2024.

The changes impact different types of firms depending on nature, size, and complexity. Below, the chart outlines the comparison of existing remuneration disclosure regulations on the different types of firms. These new proposed changes set out in CP14/23 are highlighted in green, whereas Simpler-regime firms are highlighted in white.

Other small firms, which also fall under Basic 3.1 but do not satisfy the small and non-complex institutions (SNCI) or Strong and Simple criteria, can also be included within the remuneration disclosure changes. These firms typically fall just outside the scope of the Strong and Simple bucket resulting from differences in the geography of firm assets, IRB approvals and group asset size. These are listed in more detail within CP5/23.

The PRA proposes the following remuneration templates should be completed by listed Simpler-regime firms:

Corresponding parts of article 450(1) of the CRR regarding UK REMA:

(a) Information regarding the decision-making process for the remuneration policy, including meeting oversight of the main body overseeing remuneration, compensation, and the mandate of the remuneration body. Additionally, information regarding any external consultancy usage within the remuneration policy creation and the role of any relevant stakeholders should be included.

(b) Information about the link between the pay of staff and their performance.

(c) The most important design characteristics of the remuneration system, including information on the criteria used for performance measurement and risk adjustment, deferral policy and vesting criteria.

(d) The ratios between fixed and variable remuneration set are in accordance with point (g) of Article 94(1) of Directive 2013/36/EU.

This is a significant reduction compared to what was previously required. Therefore, Simpler-regime firms will have cost benefits as fewer resources will be needed to complete the remuneration templates.

Despite only providing a basic overview of the remuneration policy, listed Simpler-regime firms would still deliver transparency to market participants. UK REM1 provides a breakdown of remuneration throughout the firm, helping market participants understand the incentives of the business. UK REMA explains the qualitative nature of the remuneration policy held by firms, outlining governance, risks, and structures.

The PRA proposes that non-listed simpler-regime firms are excluded from the requirement to disclose any information about their remuneration policy. Since market participants have limited availability to non-listed firm policies, the PRA found that the costs of disclosures would outweigh the benefits for the firm.

References

The PRA is expected to introduce a more proportionate prudential regime for less systemically important banks and building societies. This will be known as the ‘Strong and Simple’ regime.

The Strong and Simple regime could present potential advantages to firms, including cost reductions and increased competitiveness due to more proportionate regulatory requirements. This article aims to provide a clear understanding of which firms could be eligible for the new regime following PRA consultation (as of Q2 2023).

Strong and Simple seeks to simplify the prudential framework for non-systemic domestic banks and building societies. The framework is geared towards UK-headquartered firms, but the PRA acknowledges that some third-country firms may benefit. This article outlines how the PRA proposes to work with third-country firms to integrate them into the simpler regime.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.