Basel 3.1 – Understand the regulation

In this series of short articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

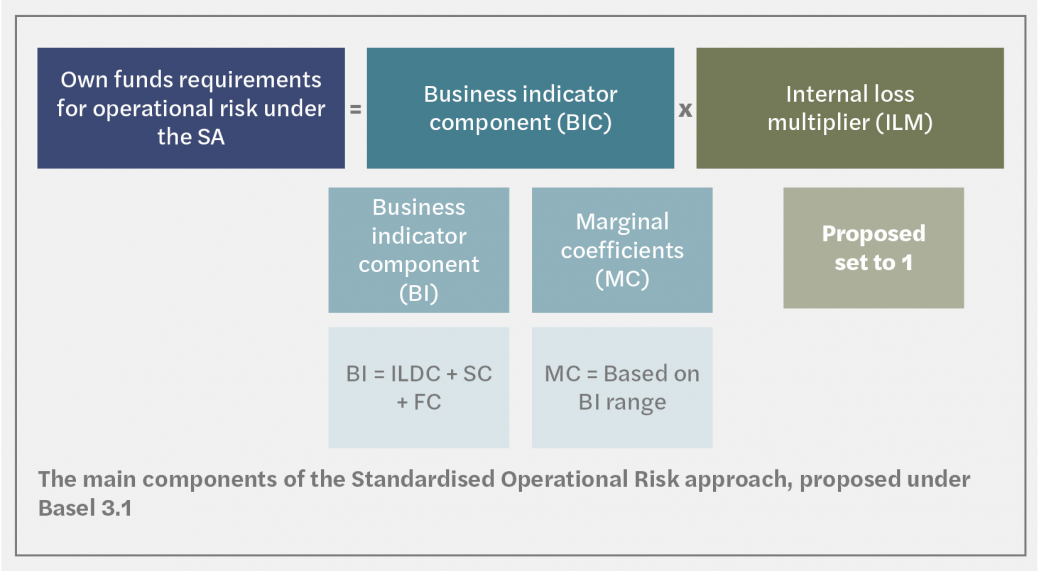

The expectation is that this, more sophisticated approach, is likely to increase Pillar 1 operational risk capital. The standardised approach is calculated as below:

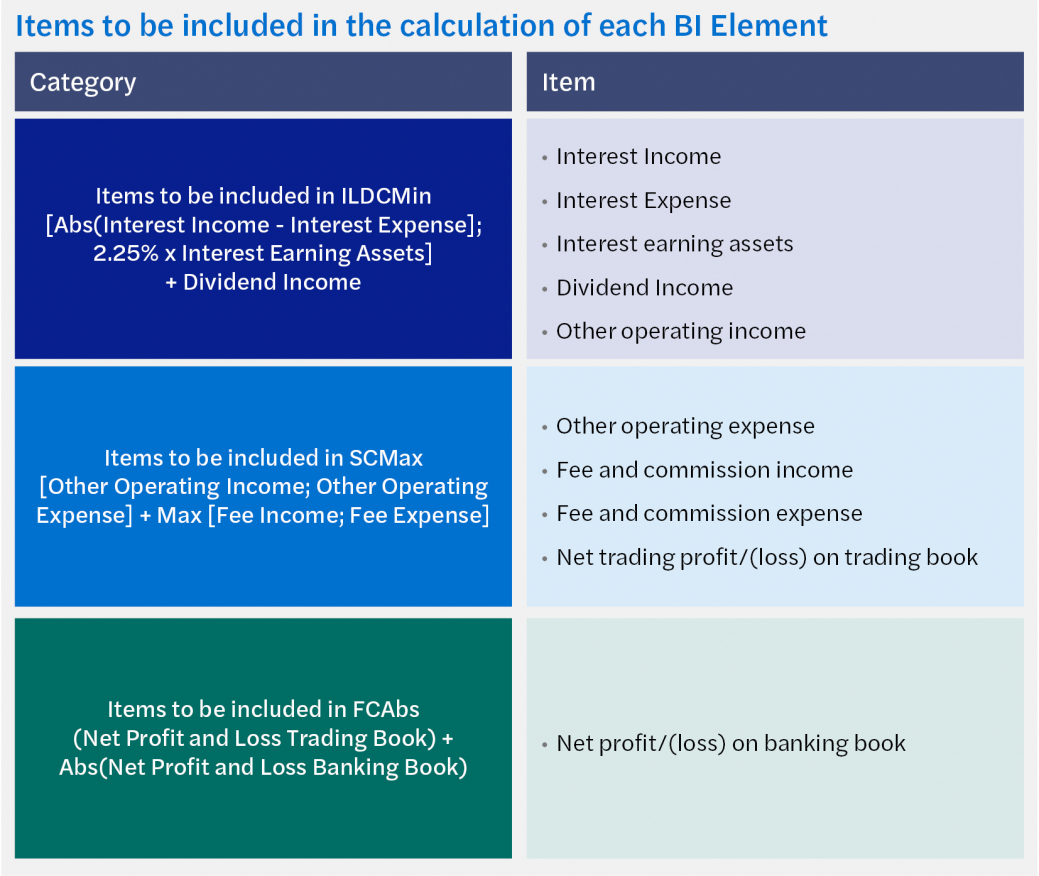

The business indicator component (BIC) is equal to the sum of ILDC (interest, leases and dividend component), services component (SC) and financial component (FC). Items included are displayed in the table.

However, the PRA has decided to set the ILM to one. By setting the ILM to one the PRA are essentially trying to smooth the capital impact of the new requirements. This decision has the effect of neutering a key element of the new standardised approach to operational risk, its risk sensitivity.

Consequently, it is highly likely this will mean that firms will have to continue to hold heightened levels of Pillar 2 Operational Risk capital to compensate. It is worth noting that the PRA is not proposing to hardcode the ILM to one. Meaning that there is a possibility this figure will change in the future and essentially ‘turn on’ the risk-sensitive element of the standardised approach.

|

What banks should consider

|

If you have any further questions regarding Basel 3.1, please contact us via the button below and a member of our team will be in touch.

In this series of short articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

The Prudential Regulation Authority’s (PRA) internal ratings based (IRB) proposals largely align with the Basel standards and there is limited divergence between the PRA and the European Central Bank (ECB) on this topic.

Under Basel 3.1, the Prudential Regulation Authority has proposed to implement changes to how firms measure market risk. These include an amended version of the preexisting simplified standardised approach (SSA) and two new calculation methodologies – an advanced standardised approach (ASA), and a new internal model approach (IMA).

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.