Basel 3.1 – Understand the regulation

In this series of short articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

This will not apply to UK banks and building societies that meet the simpler regime criteria and choose to be subject to the Transactional Capital Regime proposals.

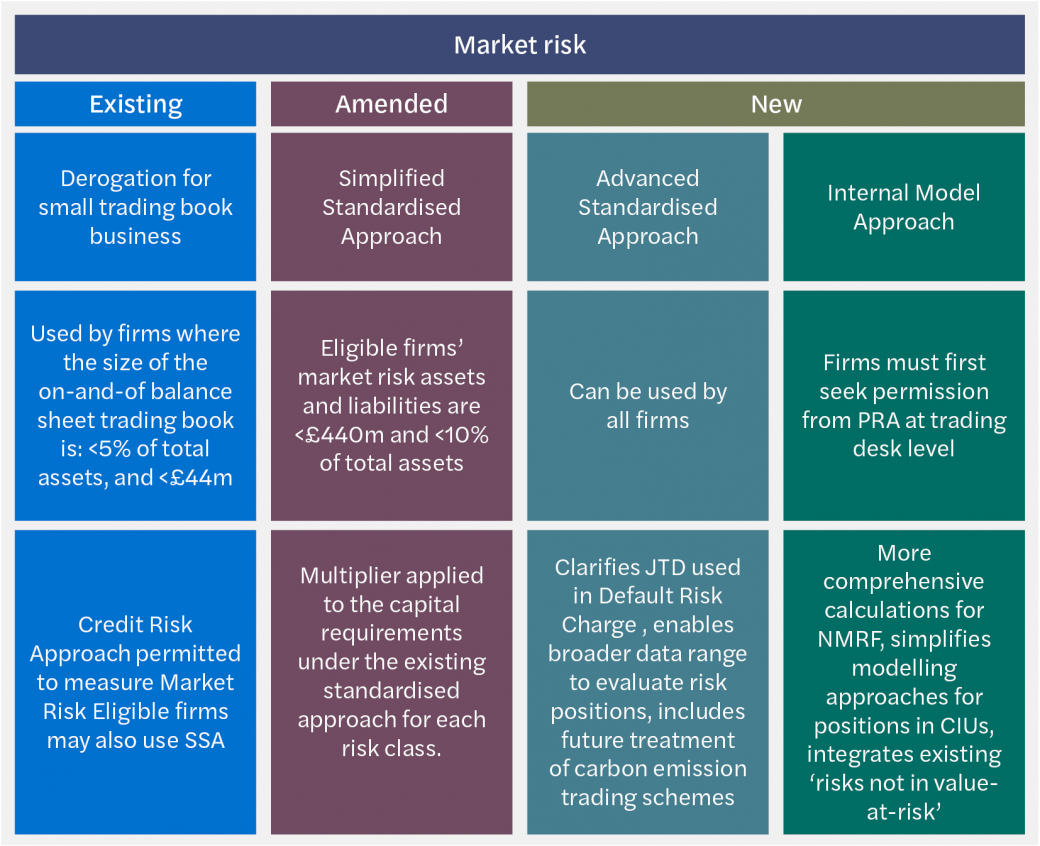

Figure 1: Overview of Market Risk Approaches Basel 3.1

Existing approach – small trading bookEligible firms for the derogation of small trading book businesses will be retained and not amended. These firms will continue to be permitted to use the credit risk approach to measure market risk, however, they may also elect to use the SSA. If a firm opts to use this derogation it needs to do so for its entire trading book. This provides operationally simple but conservative approaches for firms with limited market risks. Amended approach – simplified standardised approach (SSA)The SSA is a simplified and recalibrated version of the current standardised approach. A firm that opts for the SSA would need to do so for all its market risk positions. Firms with correlation trading portfolios (CTP securitisations) are not eligible due to the complexity of correlation trading. The SSA updates PRA’s expectations on the calculation of modified duration and incorporates the substantive elements of existing technical standards relating to the existing market risk standardised approach. Requirements are also outlined for the treatment of FX and Commodity positions in the banking book, increasing the frequency with which the value of these risks must be updated. New approachesAdvanced standardised approach (ASA) The ASA will be available to all firms due to its suitability for measuring complex trading risks and firms may elect to use the approach without PRA’s approval or notification. The PRA proposes that firms will be allowed to use a combination of IMA and ASA to calculate market risk capital requirements. Internal model approach (IMA) IMA provides an appropriate level of risk sensitivity for firms with material market risks with an additional safeguard of PRA scrutiny by means of the permissions process. To use IMA, firms must seek permission at the trading desk level thus reducing barriers for smaller firms to use the most risk-sensitive approach to calculating capital requirements. Any firm applying to use IMA must allow the PRA at least 12 months for any application to be processed, therefore firms needing to go live on 1 July 2025 must submit no later than 1 July 2024. Similarly, to the SSA, requirements are outlined for the treatment of FX and Commodity and the frequency with which the value of these risks must be updated is increased. |

What banks should consider The new proposals mean more comprehensive calculations for the standardised approach which may cause strain on firms as they navigate additional complexities and frequencies of calculations. Firms will need to design, implement, and monitor new controls to ensure that calculations are reflective and accurate to the new proposals in accordance with the market. This is likely to require new processes and training for employees. The aim of this proposal is to better reflect capital requirements in response to market changes. Depending on industry type market fluctuations may be extreme causing additional recalculations and the need for increased due diligence. Firms will need to meet eligibility criteria to use different approaches which may require external consideration. |

If you have any further questions regarding Basel 3.1, please contact us via the button below and a member of our team will be in touch.

In this series of short articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

Under Basel 3.1, all existing Pillar 1 operational risk approaches (basic indicator approach, standardised and advanced measurement) are being replaced by a new standardised approach which aims to encompass a firm’s size, complexity and historic operational risk performance. the latter is dictated by the internal loss multiplier (ILM) calculation.

The PRA has disclosed that they intend to review the Pillar 2 capital framework by 2024 at the latest. It is worth noting that these timelines are incredibly tight when aligned with the planned implementation of Basel 3.1 on 1 July 2025.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.