Basel 3.1 – Understand the regulation

In this series of short articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

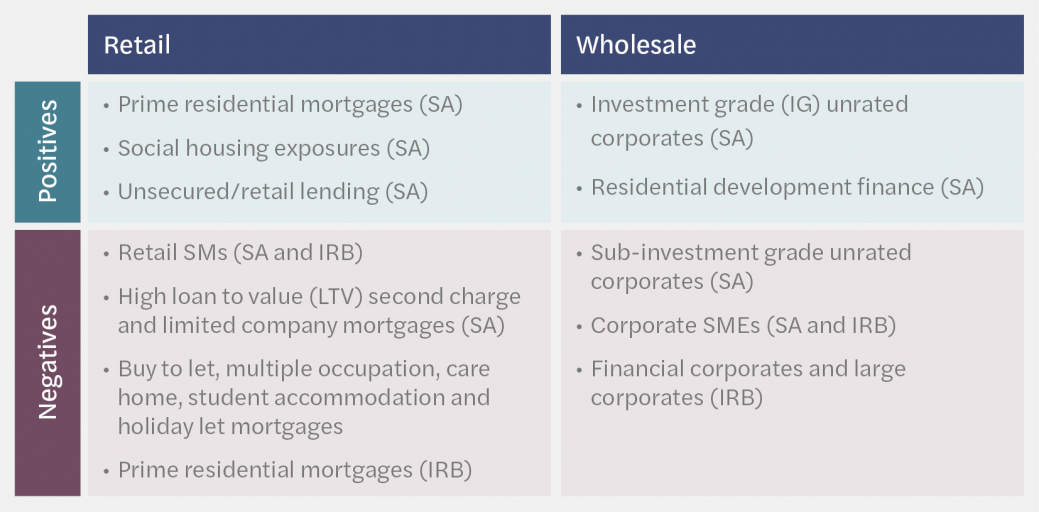

Credit Risk – Standardised Approach

These changes have been designed to address over-reliance on external credit ratings, increase risk sensitivity and promote effective competition between SA and IRB firms. This includes additional exposure sub-classes; a grading mechanism for unrated corporates; due diligence requirements on the use of external credit ratings; removal of the small and medium-sized enterprise (SME) support factor and reclassification of real estate exposure risk weights. While it is business model dependent, the proposed changes are likely to have a material impact for several small and large banks.

Overall, the changes in credit risk can be bucketed into two separate camps. Those that are likely to have a positive (lower) impact on bank capital requirements and changes which are expected to have a negative (higher) capital impact. We’ve set this out in a table below:

There are two changes that appear to be most vexing for firms. The first is the removal of the SME Support Factor. This is likely to increase the cost of capital for lending into this market. The second is the reclassification of mortgages which will move some subclasses of mortgages from residential into commercial (higher) risk weights. Reclassification of Retail and Commercial MortgagesThe PRA also proposes to clarify the definition of ‘regulatory real estate’. A change that has received less commentary than the removal of the SME supporting factor but appears likely to have a more material impact on risk weights across the entire industry. Under the new rules, the regulatory real estate exposure risk weights will be determined based on the type of property, the loan-to-value (LTV) ratio and whether repayments are ‘materially dependent on the cash flows generated by the property’. The PRA has decided that houses in multiple occupation should be treated as materially dependent on the cash flows generated by the property. Buy to Let exposures to individuals with three or less mortgaged residential properties will receive a carve out. The PRA has further clarified the definition of residential property, excluding care homes, purpose-built student accommodation and holiday lets, which would all be treated as commercial. These changes will result in upward revisions to the underlying risk weights associated with those categories of lending. As part of all these proposals, the understanding is that the value of the property is fixed at the origination date. This has been done to reduce the risk of excessive cyclicality in property values. |

What banks should consider:

|

If you have any further questions regarding Basel 3.1, please contact us via the button below and a member of our team will be in touch.

In this series of short articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

Under Basel 3.1, all existing Pillar 1 operational risk approaches (basic indicator approach, standardised and advanced measurement) are being replaced by a new standardised approach which aims to encompass a firm’s size, complexity and historic operational risk performance. the latter is dictated by the internal loss multiplier (ILM) calculation.

The Prudential Regulation Authority’s (PRA) internal ratings based (IRB) proposals largely align with the Basel standards and there is limited divergence between the PRA and the European Central Bank (ECB) on this topic.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.