National contact

The consultation paper CP9/20 ‘Non-systemic UK banks: the PRA’s approach to new and growing banks’, published in July 2020 and closed in October 2020, is relevant to UK banks that are:

The PRA has observed a number of issues and proposes to clarify its expectations with regards to new banks, as they grow and mature. In doing this, the PRA hopes to promote a positive regulatory relationship with those banks through open, constructive, and forward-looking communication.

The PRA has noticed inconsistent approaches in the calculation of the PRA capital buffer. It is currently based on wind down costs and it is proposed that new banks:

This could prove to be a disincentive to invest, as higher expenses lead to higher requirements. However, this is not the main concern of the regulator as financial stability remains their focus.

As the likelihood of failure may be higher during the early years of a bank’s development, new banks are expected to have and maintain credible and comprehensive recovery and solvent wind down plans. This is expected to minimise disruption and impact on financial stability and depositors, should they fail. This proposed requirement will need to be satisfied at the point of authorisation or upon exit from mobilisation.

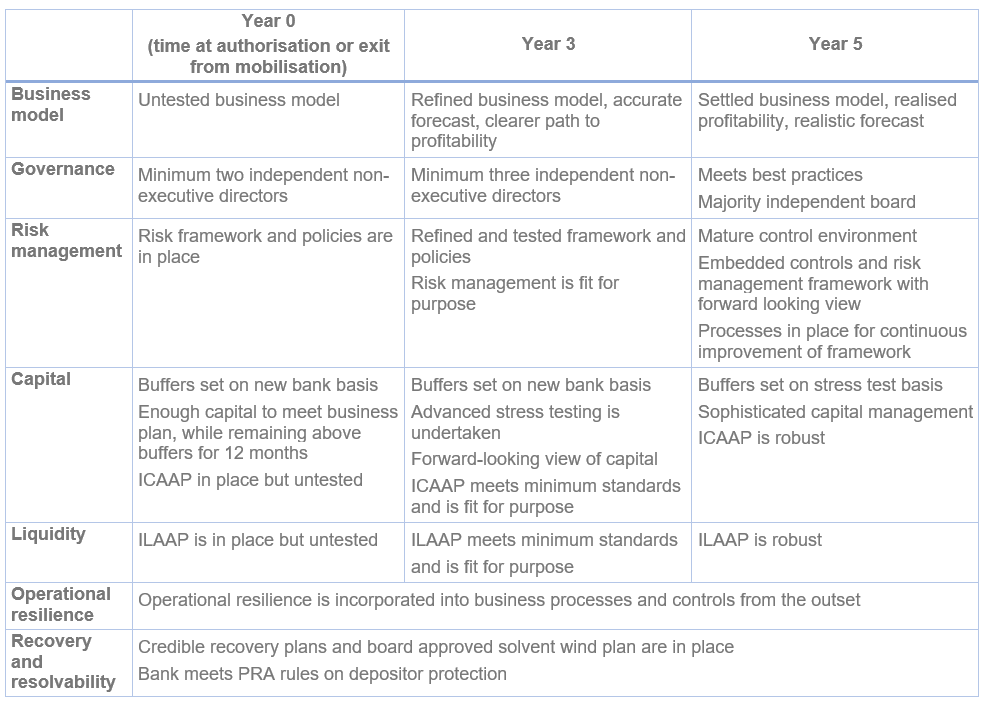

The PRA has noticed that while efforts on getting authorised are significant, many new banks underestimate the subsequent development required to become a successful and established institution.

The PRA appreciates that new banks need time to build and demonstrate capabilities and expects them to gradually:

CP9/20 is the follow-up of a joint publication of the Bank of England / FSA dated 2013: ‘A review of requirements for firms entering into or expanding in the banking sector’. Whilst there are not fundamental changes, the current PRA supervisory approach should be read in conjunction with the following existing documents:

The PRA knows that banks may already meet the expectations set out in the above and the draft Supervisory Statement associated with CP9/20 and if this is the case, costs resulting from the proposals are likely be minimal.

Expert analysis on the latest regulatory insights in the UK.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.