Latest economic, market and investment news

Read our latest news and analysis on the changing markets and economic environment.

The impact of geopolitics on markets

Trying to pinpoint when this changed is folly, the causes of much of the strife in the world today are millennia old, however, the Brexit vote and Trump’s victory in 2016 certainly felt like a period when geopolitics came back to the front of investors’ minds. Interestingly there was no market meltdown following those events, in fact, if you had known the results in advance you would likely have performed worse from an investment point of view.

There are two main reasons why geopolitics wasn’t much of a concern following the fall of the Soviet Union. The first is that this period was the height of the ‘Pax-Americana’, a unipolar world with one superpower: The United States. There can be many complaints about US foreign policy, but by and large the goals of the US for the past 30 years were, and still are, global stability. Yes, the US made some serious mistakes in their invasions of Iraq and Afghanistan, but human suffering aside, these were peripheral conflicts. This preference to maintain order generally makes sense for the country at the top of the food chain.

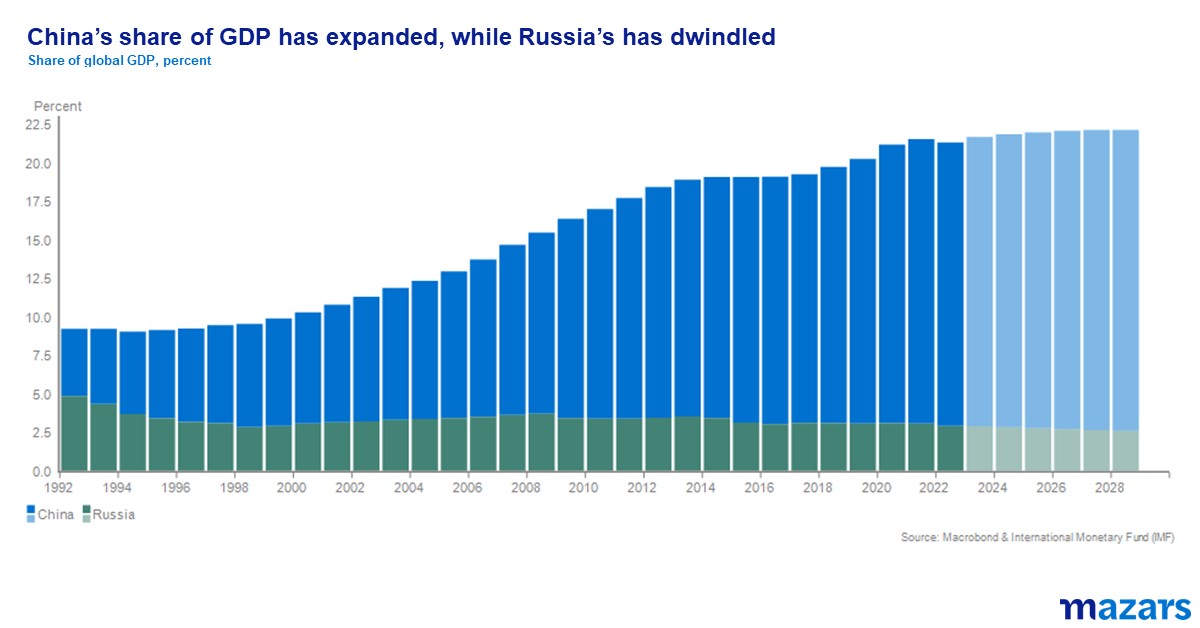

Why were we in a unipolar world? It was really a case of timing. When the Soviet Union collapsed in 1991 it was the only other superpower. It was always going to take time for another to emerge. The EU, with its fragmented democracies, is never likely to act as a unified superpower, and in any case, is an ally of the US. Meanwhile, until recently China just didn’t have the economy. This is on the cusp of changing, making it the only other country that could be described as a superpower, even though by formal definitions it is not quite there yet.

The second reason was that globalisation seemed to be on an ever-upward trajectory before the GFC in 2008. For decades there was growing trade and co-operation, and general consensus that this was positive for living standards. Countries that have close trade links tend to find ways to co-exist without conflict. However as has been well documented, electorates in liberal democracies have started to embrace more populist leaders in recent years in response to stagnating growth, concerns about levels of immigration and views that governments were happy to bail out ‘elites’ at the expense of the average person.

According to the IMF, globalisation has at best plateaued since 2008. Meanwhile, isolationism, particularly in the US, is on the rise. MAGA is not just a populist, but also an isolationist message, with the difficulties the US House is having passing further aid to Ukraine a clear example.

It is not just liberal democracies that have changed their tune. There was a long period where countries such as China and Russia seemed to be improving their relations with the US, something that certainly isn’t the case now. Why not – improved relations lead to more trade, especially beneficial to China, and so stronger economies. There was even talk of Russia joining NATO at one point.

Trying to dig too deeply into the strategic goals of the leaders of these countries is often an exercise in guesswork even for subject matter experts. However as discussed in the book Rise and Fall of Nations by Ruchir Sharma, countries often experience the greatest growth when their leadership is relatively new with fresh ideas. This is a real benefit of genuine democracies, where the turnover of leadership is fairly frequent (although this can go too far, for example in Australia where elections are every three years and the political process is rather chaotic). It is fair to say that leadership in both Russia and China is somewhat stale and lacking ideas, and both Putin and Xi have had to change their constitutions in order to maintain power. There may be genuine strategic or even security concerns for both the invasion of Ukraine and China’s increased sabre-rattling around Taiwan, but both fit the pattern of seeking greater conflict to diminish internal dissent.

Russia’s invasion of Ukraine may make it appear, based on the daily news, that it is the main geopolitical risk from the point of view of Western markets. However, both Russia’s GDP (2.2% of global GDP and falling) and population (1.8% of the global population) mean that absent a nuclear conflict, it is, as Barack Obama might wish he hadn’t said, a ‘regional power’ that is of less strategic concern. Instead, it is the rise of China to a level that can compete economically and in terms of global influence with the US, and so upend the ‘Pax-Americana’, that has helped to usher in the multi-polar order that is emerging. With another power to strap themselves to, other countries who weren’t too enamoured with US hegemony have more freedom to act as they see fit. One area where this is particularly obvious is Africa, where China has been able to develop significant economic ties and influence.

As with many phenomena, the move away from a unipolar world started as a trickle but now is in danger of becoming a torrent. It is becoming clear that a multi-polar world is not incrementally, but fundamentally different from a unipolar world. Aside from the concern that the general trend of de-globalisation could affect trade and growth, several risks/events are both already contributing to, and would significantly inflame, risks in global markets:

The first thing to note is that almost all of these scenarios are or would be inflationary, whether through the impact of conflict on raw materials pricing or because they are de-globalisation events that are likely to push up costs. Also, a lack of global co-operation is likely to hamper attempts to mitigate the worst effect of climate change.

And whether just by their inflationary effects, or their effects on investor confidence (de-dollarisation and US isolationism would certainly push up the US risk-free rate), almost all these events have or would be expected to have an upward effect on global yields, albeit Treasury yields would likely fall in the short term for some of the scenarios as investors seek safe havens. And these risks don’t include other factors which I believe are likely to place upward pressure on risk-free rates such as the move away from just-in-time stock control, rising government debt and interest payments in the Western world, and the way that the use of drones in warfare could challenge traditional forces.

To the relief of almost everyone, inflation has been moderating in recent months, to the extent that the December Fed ‘Dot Plot’ had median expectations of three rate cuts in 2024. Markets went further and started to price in six rate cuts and a first rate cut in March, however, marginally stronger than expected inflation data for December across the US, EU and UK have seen expectations moderate closer to four rate cuts at the time of writing. Although inflation has moderated, we are almost certainly in an era where inflation will be more volatile. We will need to stop thinking in unipolar terms. Much like during the Cold War, it might now be time to think in terms of balance rather than dominance. Greater commodity exposure, awareness that inflation has more potential to eat into nominal bond returns, and a move away from global investments being quite so US centric could be key to weathering less predictable markets. Despite its continued overarching military power, it is unlikely the US will be able to put the genie back in the bottle, to stop the torrent.

James Rowlinson, Senior Investment Manager

Read our latest news and analysis on the changing markets and economic environment.

Global equity and bond markets enter 2024 with significant momentum from the last two months of 2023 fuelled by falling inflation and subsequent dovish projections from the US Federal Reserve.

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.