The economy & your investments

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

Demographics, debt and interest rates

When applied to other major economies – that worsening demographics (defined as a household that has less than 60% of median income) will mean, long term, interest rates have to remain low – how else will we afford to manage the rising debts?

There is certainly a correlation between low growth and low-interest rates. Low growth is likely to lead to less inflationary pressures, leading to the need for high-interest rates. Similarly, productivity is a long-term determinant of return on capital and thereby influences interest rates.

This makes sense in a low-inflation environment, but it may not make sense if the world experiences a prolonged period of heightened inflation.

I think we need to examine this question from another perspective. Usually, when you lend to a person or company who you consider more ‘risky’, due to a combination of higher existing debt and lower income, you would want a higher rate of return to compensate for the risk that you will not get the money back in full.

Now when a country issues debt in their own currency, the risk is not that they won’t repay the debt, but rather that they will have to print money and inflate away the value of the debt they owe, but it is a similar risk in reality. So the logic that as demographics in the West worsen, causing muted productivity growth and ballooning debts, which will become more difficult to repay through taxes alone, yields and interest rates will move lower seems frankly ridiculous.

This belief has possibly arisen due to the aforementioned experience in Japan. However, Japan experienced this change during a time of increased globalisation and at points of historically low global inflation as China exported deflation to the rest of the world. This era appears to now be at an end.

In reality, there has to be an inflection point, at which the downward pressure on rates from slow growth is overcome by the upward pressure associated with being less reliable lenders. In essence, a lot of developed nations could start to face issues also faced by emerging economies.

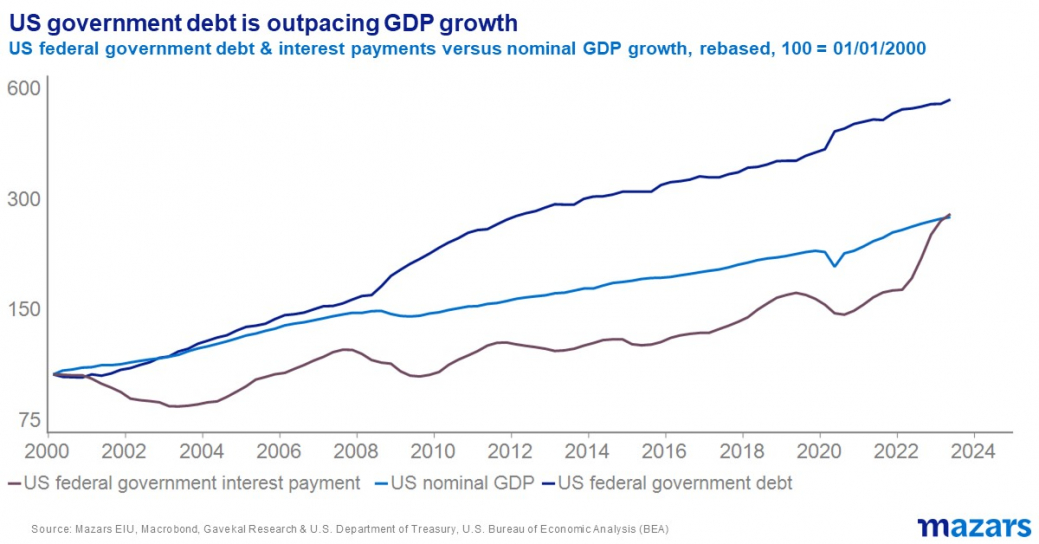

Looking at the US, since 2000 US nominal GDP has risen 2.7x. Meanwhile, US federal government debt has risen 5.6x. Due to interest rates falling over the period, interest payments have only risen 2.7x – in line with GDP. But with global yields now significantly higher, Treasuries will have to be issued with higher coupons, which will push the interest costs higher at a faster rate.

In a non-inflationary world, this might not be a problem – the Fed could buy this debt and keep yields and interest payment rates down. But that doesn’t seem to be the case. In fact, the Fed is reducing its balance sheet in part to help reduce inflation.

So, we could be entering a situation in the US, and the collective West, where:

Measuring the strength of the deflationary forces pulling yields lower vs. the debt forces pushing them higher is extremely difficult, and predicting the timing of inflexion is almost impossible. And counter to my argument, Japan has faced very little inflation and has been able to control its yield curve.

Perhaps the deflationary forces of worsening demographics will always offset concerns about deficit repayments sufficiently to keep interest rates/yields down. And perhaps Japan is a special case, with a less consumer-led economy which is less prone to inflation.

The point remains, I don’t think enough airtime is given to the possibility of worsening demographics resulting in higher long-term interest rates.

James Rowlinson, Senior Investment Analyst

On the final Wednesday of every other month, our Chief Economist and Chief Investment officer discuss the current economic landscape and the impact on investors. Sign up below to join them at their next session.

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

“What if I could tailor my investments to my needs?”

Read our latest news and analysis on the changing markets and economic environment.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.