The importance of long-term investing

October 2023. When it comes to our emotions, we can honestly say that sometimes they make us a bit irrational, meaning we are more likely to make biased decisions.

Asset prices and the economy - where are we headed

However, history can provide us with clues as to how asset prices will respond to external influences and help guide our decision-making process. Let’s look across notable periods in recent history and examine the impact of two key economic factors, inflation, and growth, on asset prices.

We’ll start with the period immediately following the initial outbreak of Covid-19. Loose monetary policy succeeded in rebooting economic activity and consumers, many of whom were put on furlough schemes by their employers, took to spending their new-found time (and money) on hobbies and other discretionary items, leading to a surge in demand for goods (and later services).

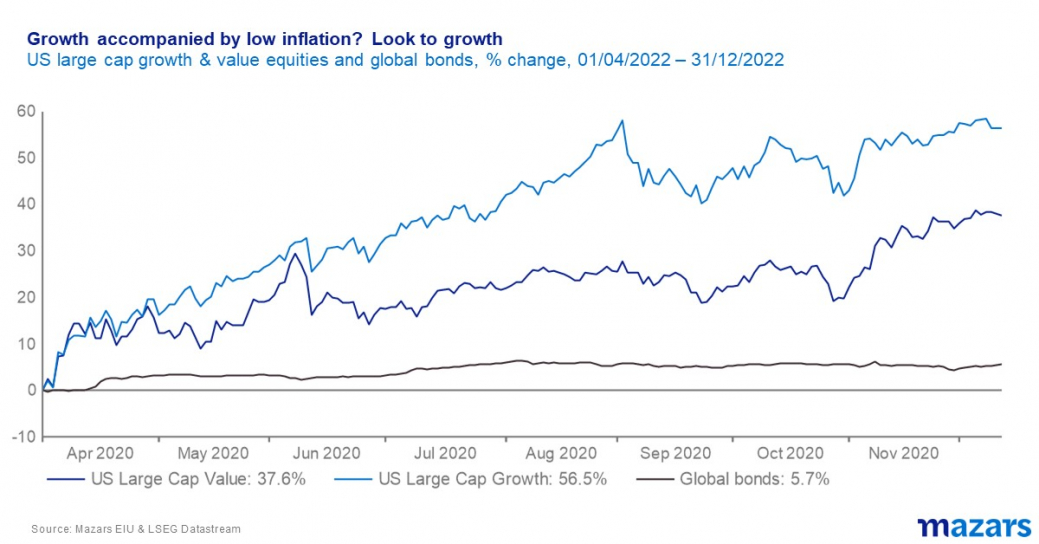

Despite global supply chains grinding to a halt, inflation expectations remained low, and the initial wave of supply-side inflation would take time to become embedded and translate into demand-led inflation. This combination of restarting economic growth and low inflation was particularly favourable for pioneering growth equities; US large cap growth equities outperformed the more traditionally stable, value focused equities by almost 20% between April - Dec 2022. Global bonds fared much worse, returning 5.7% over the same period.

Granted, this is an extreme example skewed by a massive influx of quantitative easing into markets and a decade of ultra-low interest rates, so let’s look at a slightly different period with similar growth and inflation prospects. As well as producing arguably the most iconic sitcom of all time, Friends, the mid 1990’s was a period of technological advancement and globalisation, driving down inflation and stimulating growth. Again, equities significantly outperformed bonds. From 1993-98, US large cap equities outperformed bonds by a staggering 140%.

Okay, but high growth and low inflation paint a picture of a rosy economy. What about when things take a turn for the worse? Enter the Global Financial Crisis. What started as a downturn in the US housing market quickly spiralled into a catastrophe as banks incurred massive losses and had to be bailed out.

US real GDP plummeted by 4.0% and unemployment skyrocketed, while deflation reared its ugly head. So, what do you do when the economy is expected to spiral out of control and inflation is non-existent? You attempt to prevent losses. This tends to be very difficult in a crisis as investors can sell assets indiscriminately to generate liquidity - particularly in the initial panic. However, if you’re looking for safety, then government bonds in stable, developed economies have historically been reliable. While short-dated US Treasury bonds are frequently used as a proxy for the ‘risk-free’ asset, US Treasuries of all maturities significantly outperformed equities in 2008.

But none of the aforementioned scenarios describe where we are today. Inflation has declined from the peaks seen earlier this year, but remains embedded, while there are concerns about a resurgence of supply side inflation as oil prices tick higher. Geopolitical tensions have resurfaced, igniting a trend towards deglobalisation and therefore, higher inflation and lower expected growth, a combination that is relatively unappealing for most financial assets. Meanwhile, central banks are desperately trying to achieve the almost mythical ‘soft landing’; taming inflation while attempting not to destroy demand, thereby tipping the economy into a deep recession in the process.

The problem is that the global economic outlook is more unclear today than it has been for a long time. If interest rates are to be held ‘higher for longer’, does this push the economy into a deep recession, kill inflation and point us in the direction of US Treasuries? Or does the economic growth limp along while inflation remains robust thanks to wage pressures in developed economies and a tight labour market? Or do we experience a resurgence of supply side inflation thanks to rising geopolitical tensions? No one truly knows. What we can conclude though is that the chances that we head back towards an era of low inflation and strong economic growth looks slim for now despite rapid technological advancements due to unapologetically tight monetary policy.

At our September Investment Committee meeting, we voted to maintain our defensive position within fixed income through our shorter duration position and limited exposure to lower quality bonds. We also limited exposure to the technology sector where valuations appear relatively unattractive given the global backdrop. In line with our new strategic asset allocation, we also introduced energy equities to the portfolios as a diversification asset, to protect against the inflationary impact of higher energy prices.

If you are interested in reading more about our current views on growth and inflation, I highly recommend our latest global economic outlook.

Adam Fisher, Investment Analyst

October 2023. When it comes to our emotions, we can honestly say that sometimes they make us a bit irrational, meaning we are more likely to make biased decisions.

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

Read our latest news and analysis on the changing markets and economic environment.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.