Restructuring and insolvency

Our restructuring and insolvency teams provide rapid support and creative solutions to help guide you through periods of financial uncertainty, preserving and maximising value for all stakeholders....

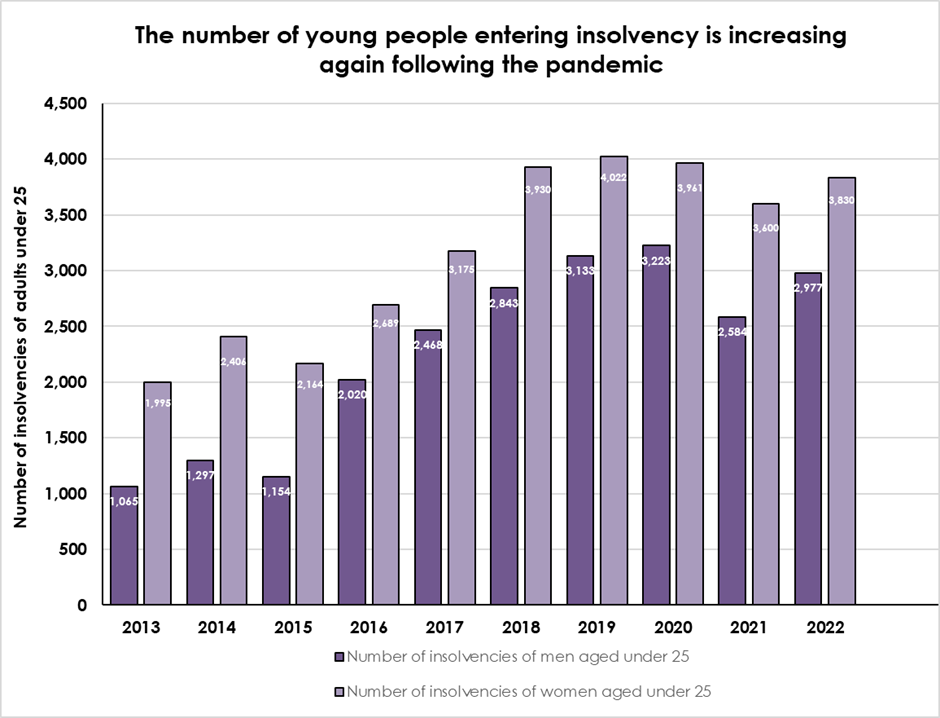

Insolvencies of young men increased 15% last year

Insolvencies of young men last year increased far more than all personal insolvencies in the UK, which rose by 9% in 2022. Insolvencies of young women under 25 increased by 6.4%, from 3,600 to 3,830.

Young people are more likely to live ‘paycheque to paycheque’ and may be more reliant on short term debt to cover their living costs. The median weekly income for males aged 18 to 21 (£294.90) and between 22 and 29 (£529.00) is less than half the median weekly income for all males (£622.90).

High inflation has stretched the finances of many younger men to breaking point and forced many into debt to pay their living expenses. As a result, they have been badly affected by hikes to the Bank of England’s interest rate over the last year, which has greatly increased the cost of debt.

As well as increasing the cost of finance from credit cards and overdrafts, higher interest rates have also increased the cost of the Buy Now Pay Later finance, which young people tend to be more frequent users of. In total, 54% of Millennials (those born between 1981 and 1996) and 50% of Generation Z (born from 1996) use Buy Now Pay Later products, much higher than compared to all age groups (12%)*. These products often charge much higher interest than other forms of borrowing and can charge very high fees for late payment.

Making matters worse, increases in rents across the country have put even more pressure on finances. UK average rents rose by 4.4%** last year, the highest annual rise on record with some estate agency reporting double digit increases in rents in London.

Young men have also been badly impacted by rising food prices and car finance costs. Food prices have increased substantially over the last year and increased by 19.1% in March 2023 alone, impacting young people who, like pensioners, tend to spend a larger share of their income on food.

In addition, there was a 70% rise in the number of adults under 25 who applied for car finance last year, which has become significantly more expensive***. Monthly car payments were said to be 40% higher in 2022 than in 2019****.

Ed Thomas, Director of Restructuring Services, says: “Young men up and down the country have found that their personal finances have been stretched by interest rate rises.”

“The young tend to earn less than the national average and are therefore being particularly impacted by the Cost of Living crisis, which still shows little sign of abating. In order to pay their living costs, some are building up debts quickly. That debt has become a lot more expensive to service over the last year.”

“Unfortunately, without the ability to either cut costs or increase their income, many more are likely to require some form of insolvency procedure.”

“Any individual struggling with their finances should take professional advice action early and speak with their creditors. This could provide someone in financial difficulty with more time to pay off their debts or agree more affordable repayment terms. Simply waiting for the problem to solve itself will only make the issue worse.”

Our restructuring and insolvency teams provide rapid support and creative solutions to help guide you through periods of financial uncertainty, preserving and maximising value for all stakeholders....

Topical updates from the world of Restructuring plus a monthly report on Insolvency Statistics for England and Wales.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.