Valuations

Understanding the value of business decisions

A management equity plan is a critical component of any private equity buyout. If effective, it aligns the interests of all stakeholders, drives desired behaviours amongst management teams, helps attract and retain talent over a deal lifecycle and provides a powerful incentive to maximise shareholder value over the period to exit.

As with any form of employee reward, there are tax implications to consider when issuing equity to management. In the UK, if an employee acquires equity for less than its unrestricted market value (UMV)* a tax charge will arise. Often, the tax must be collected via Pay-As-You-Earn (PAYE), and it is the Directors’ responsibility to ensure tax is levied on the correct amount.

Ensuring equity incentives are affordable for management is an important part of their design.

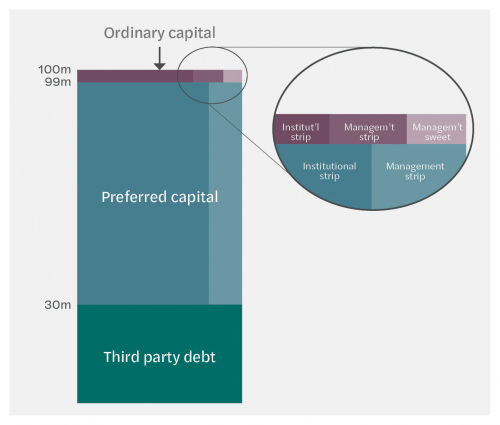

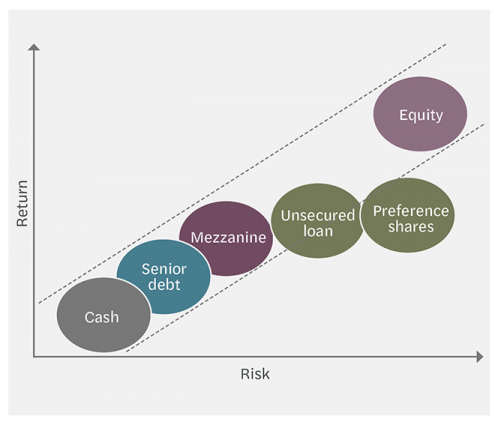

Most private equity buyouts are financed by a combination of third-party debt and shareholder capital. The shareholder capital is often split between preferred and ordinary capital. The rights of the preferred capital can vary, but often take the form of shareholder loan notes or preference shares with a coupon which accrues at a rate of between 8% and 12%. Most of the shareholder funding is preferred capital (for example, a ratio of 99:1) with relatively trivial amounts paid to subscribe for ordinary shares.

The shareholder capital is primarily funded by the private equity investor (‘institutional strip’) though management of the target will often roll a proportion of their existing equity into new preferred and ordinary capital (‘management strip’). This is typically required as a condition of the deal to assist with the retention of management.

A proportion of the ordinary shares is allocated to a management equity plan (‘sweet equity’). As it ranks behind the preferred capital, it incentivises management to grow shareholder value at a rate higher than the coupon on the preferred capital.

The sweet equity can have the same economic rights as the ordinary strip or can be designed to provide an additional reward for exceptional performance. This can be achieved through a ratchet mechanism, such that if the deal internal rate of return or multiple of money exceeds predetermined thresholds, management receive an enhanced return.

In the UK, a Memorandum of Understanding (MoU) was agreed between the British Private Equity & Venture Capital Association (BVCA) and HMRC such that if certain ‘safe harbour’ conditions are met, HMRC will accept that the price paid by management is equal to the initial UMV of the shares and no tax charge arises. Some of the key conditions are as follows:

If the transaction is structured in a way that meets the requirements of the MoU, a valuation for UK tax purposes is not required.

However, the MoU conditions are restrictive, limiting the opportunity to design bespoke and effective management equity plans. It can lead to unequal treatment for overseas managers who may be required to pay more for their shares than their UK equivalents. New joiners also cannot benefit, even if they acquire sweet equity just one day after completion of the transaction. The MoU also does not apply for financial reporting purposes, meaning share based payment charges may arise even where managers are considered to have paid UMV for tax purposes.

Therefore, even where the conditions of the MoU are expected to be met for some/all managers, it is still important to consider the value of the sweet equity ahead of issuing the shares.

A common misconception is that if management pay the same price per share as the private equity investor (for shares with broadly similar rights) this will always be at least equal to UMV. However, this is only the case if the interest rate on the preferred capital is at least a market rate.

For many years, UK tax valuations could be agreed with HMRC under the Post Transaction Check (PTVC) procedure. Even where a transaction fell outside of the MoU it could often be agreed that the UMV of shares was no more than the price paid on the basis the transaction had been negotiated between third parties”. However, HMRC’s approach to valuations of highly leveraged shares has evolved in recent years and the PTVC service has since been withdrawn.

Whilst the private equity investment may be on arm’s length terms, this only means that the aggregate value of the private equity investor’s preferred and ordinary capital is equal to the aggregate price paid. How value is allocated between the preferred and ordinary capital depends on the coupon attaching to the preferred capital. If the coupon is less than a market rate, the value of the preferred capital is less than its face value. In turn, the value of the ordinary capital must be more than the price paid.

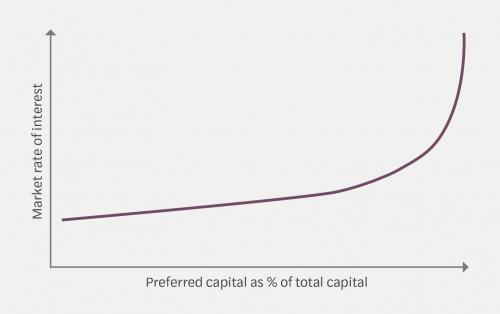

The BVCA’s guide to private equity notes that although the preferred capital carries much higher risk than third party debt, typically this is not fully reflected through the coupon**. This suggests the coupon on the preferred capital is typically less than a market rate.

The highly leveraged nature of the ordinary capital means even a small differential between the actual rate and a market rate can push significant value into the ordinary capital. It is no longer sufficient to simply assume the coupon on the preferred capital is a market rate just because it falls within the typical 8% to 12% range. A notional market rate of interest increases exponentially as the amount of preferred capital leverage increases.

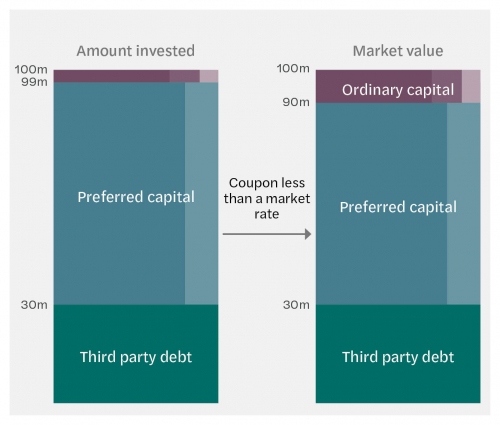

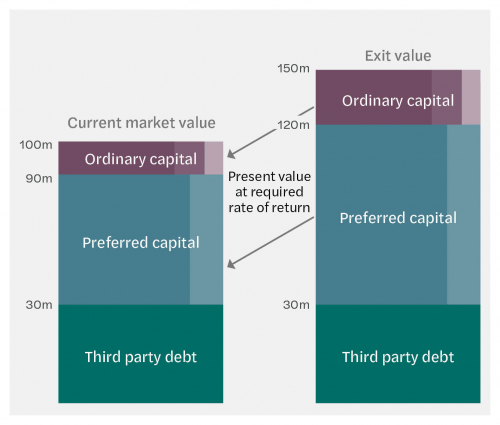

In the example illustrated below, the private equity investor has acquired preferred capital for its face value and ordinary capital for £1.00 per share. The coupon is slightly less than a market rate and the value of the preferred capital is therefore £60m rather than £69m (13% less than the price paid). In turn, the value of the ordinary capital is £10m rather than £1m (1,000% higher than the price paid). Were management to also pay £1.00 per share for shares with similar rights they may have significantly underpaid.

Whilst this is not necessarily a problem where management acquire preferred capital and ordinary capital in the same proportions as the private equity investor (as is usually the case for strip equity), where their investment is more heavily weighted to ordinary capital or additional sweet equity is acquired, this could result in an unexpected PAYE/income tax obligation.

Recent changes in macro-economic conditions and the response of central banks to increase interest rates means that yields available on corporate bonds have increased significantly over the last 18 months.

This is impacting the rates at which third party debt financing can be obtained by private equity investors. Whilst interest rates will vary from deal to deal (depending on, inter alia, the stability of cash flows, the interest coverage ratio, the proportion of enterprise value, the seniority of the tranche and whether it is secured), yields available on 10-year sterling denominated BBB rated corporate bonds are currently in excess of 5% compared to less than 2% at the start of 2022.

However, in many deals we have seen this has not flowed through to corresponding increase in the coupon on the preferred capital. The coupon now appears cheap on an increasing number of deals, suggesting the value of management’s ordinary capital may be higher than first apparent.

The value of management equity in highly leveraged capital structures is estimated based on its expected future cash flows. This is typically a single cash flow on a future exit event. For the most highly leveraged structures it is usually necessary to consider a range of potential exit proceeds to ensure the returns profile of the sweet equity is appropriately reflected in the valuation. The expected returns are probability weighted and discounted to present value at a required rate of return which reflects the business’s underlying cost of capital and the leverage in the structure. This is commonly referred to as a probability weighted expected returns methodology (PWERM).

An option pricing methodology (OPM) can also be used as an alternative. Despite its limitations when applied to the valuation of equity in private companies, it inherently reflects a wide range of potential exit scenarios and does not require an estimate of the required rate of return, which in certain circumstances can make it a more appropriate valuation approach.

The coupon on the preferred capital is reflected in both valuation methodologies. However, despite circumstances where the interest rate on the preferred capital is less than a market rate, it is not always the case the value of management’s ordinary capital will be higher than the price paid by the private equity investor. This is because the valuation should apply discounts to the reflect the fact that:

It is important discounts are only applied where it is reasonable to do so, as certain restrictions and conditions that attach to management’s shares which may reduce their commercial value are disregarded for tax purposes.

The price at which management acquire equity is an issue of increasing focus for tax due diligence exercises. Expert tax valuation advice should always be taken where shares are acquired by management outside the safe harbour provisions of the MoU.

Where the value of management equity is considered unaffordable for management, adjustments to the deal structure can be made to reduce the value of management’s ordinary equity. For example, the coupon on the preferred capital can be increased.

A similar effect can be achieved by adjusting the rights of the sweet equity. For deal structures where the shareholder capital is provided exclusively in the form of ordinary capital, a popular management incentive is a ‘growth share’, which only participates in returns once a pre-determined equity threshold has been exceeded. Growth shares can be used in combination with preferred capital to create a more challenging target, reducing the upfront value of the sweet equity.

Clearly, introducing more challenging targets can reduce the attractiveness of the sweet equity to management. The returns profile of the sweet equity should be carefully designed to balance both the upfront cost and its effectiveness as a tool to retain, incentivise and reward management.

If management acquire equity for less than its tax market value, a PAYE obligation may arise. The price paid for shares acquired outside the safe harbour provisions of the MoU is an issue of increasing focus for tax due diligence exercises.

Recent changes in HMRC approach have made the valuation of management equity plans more complex. Even where management pay the same price as the private equity investor for the same class of shares, this could still be considered less than market value. Recent rises in interest rates have exacerbated this issue.

Expert tax valuation advice should be taken as part of the design phase to ensure unexpected PAYE obligations do not arise. Adjustments can be made to the deal structure or the rights of management’s shares to reduce their upfront cost whilst maintaining an attractive returns profile thereby retaining, incentivising, and rewarding management.

Mazars has a wealth of experience relating to the design and tax valuation of management equity plans and frequently advises businesses, private equity investors and management teams on the commercial, tax and valuation considerations related to their implementation.

If you’d like to know more about any of the topics discussed in this article, our team of advisors can assist, please use the contact form below.

* Assuming a valid section 431(1) ITEPA 2003 election is in effect.

** British Private Equity and Venture Capital Association (2010) A Guide to Private Equity (pp 34).

Understanding the value of business decisions

Bespoke advice in all areas of taxation, helping businesses and individuals make appropriately informed decisions about their tax position.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.