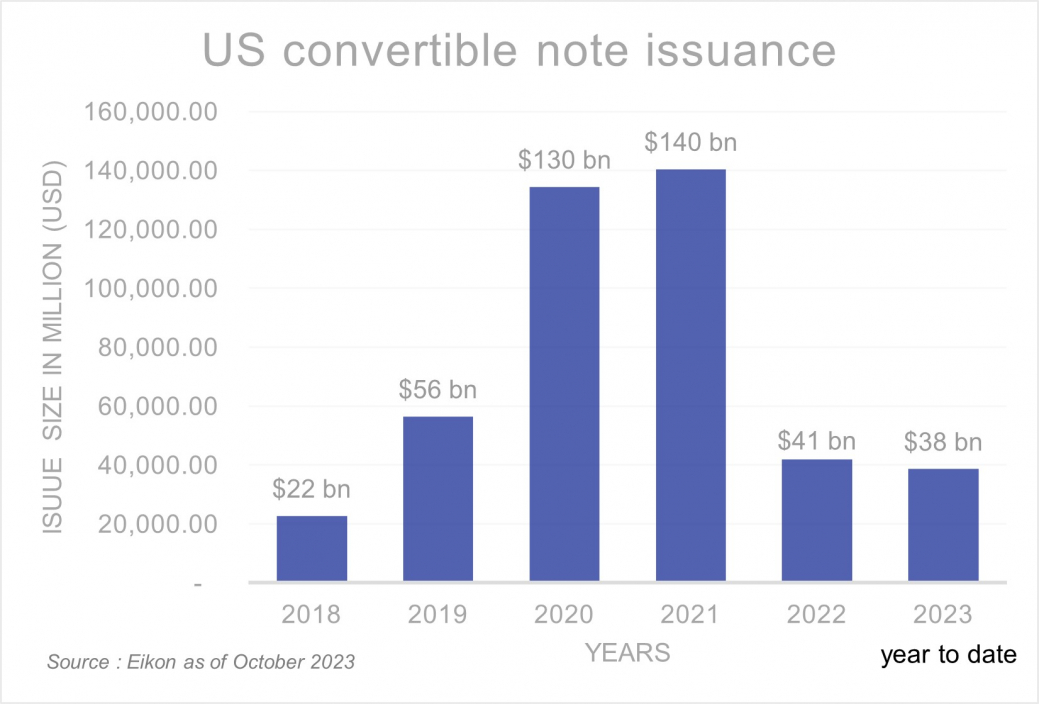

After a really slow year in 2022, convertible issuance is growing again and this trend is expected to accelerate in the next two years as a lot of companies have to refinance in optimal circumstances for convertible issuance.

What are the challenges that come with the convertible bond accounting?

Convertible debt instruments can present complexities from an accounting perspective, particularly from the issuer’s perspective. The use of complex and bespoke features, designed to address investor appetite, mean that the detail of the contractual terms and conditions must be analysed against the requirements of the relevant accounting framework, to ensure the appropriate accounting treatment.

Specific contractual terms may impact the accounting classification of an instrument between equity and debt, and/or between liability measurement bases, and can at times result in unexpected accounting consequences. These accounting classifications dictate the valuation basis upon at which instruments must be recognised and measured in the financial statements.

Where a company is sensitive to the accounting presentation and measurement of an instrument, it is always advisable to understand the required accounting for an instrument ahead of issue.

What are the challenges that come with the convertible bond valuation?

For larger companies, an active secondary market for convertible bonds may exist while for smaller companies this is typically not the case as most investors have a “buy and hold” strategy.

This means that companies have to mark-to-model their convertible instruments according to their relevant accounting standards.

Determining the fair value of convertible instruments according to accounting standards (for example in Europe according to IFRS9) is an exercise that requires technical expertise and knowledge of best market practices.

The optionality of conversion adds an element of complexity to the valuation process, as the value of the bond depends on various factors, including the future behaviour of the underlying share price, interest rate and credit spread movements, and the terms and conditions outlined in the bond prospectus. As such, while various models exist to value convertible bonds/loans, they all display the same features:

Risk factor

Modelling considerations & best practice

Equity (implied) volatility

Must have – whenever the implied option market is illiquid or non-existent, a simpler flat volatility proxied from historical returns can be appropriate

Equity spot and dividends

Must have – dividends (if any) impact the equity forward price and the model must account for them

Spot Interest rate curve

Must have – the spot interest rate curve with its term structure must be accounted for

Interest rate (implied) volatility

Depend on market – interest rate volatility impact convertible bond/loan valuation but to a lesser degree, more relevant for IG convertible bonds

Credit spread (typically Z-spread)

Must have –credit spread of the issuer must be accounted for, proxy might need to be used based on comparable issuers in case of illiquid market

Credit spread (or hazard rate) implied volatility

Depend on market – typically credit option market is illiquid, generally not accounted for

The conversion option requires a numerical method compatible with American option exercise such as a Tree, a lattice, or an American Monte Carlo.

Convertible bonds/loans can also display features such as callability, putability and barrier to conversion such as Parisian barriers. They must be accounted for in the pricing.

A team of accounting & valuation experts

1) Credentials in accounting and valuation of financial instruments

We have numerous references of helping businesses correctly account and acting as valuation agent to value convertible bonds, loans and other financial instruments (warrants, stock options, derivatives of any complexity level, ABS, mortgage bonds etc) according to their relevant accounting standards.

Our team are also acting as specialists within the context of external audit or large investment banks. We keep abreast of best market practices from active sell-side market makers and traders.

2) Multiple pricing libraries and data providers

We have external renowned pricing libraries such as Numerix but have also developed in-house pricing libraries. Similarly, we have access to various data provider such as Bloomberg and EIKON.

We therefore ensure the coherence of our prices via changing (suitable) pricing model and data.

3) Comprehensive accounting and valuation reports

We have experience in documenting our approach to allow companies to engage efficiently with their external auditors.

National contact

Nicolas Cerrajero

Partner - Co-head of Quantitative Solutions UK

London