Consumer insights

Expert analysis on the latest consumer industry insights in the UK.

| April 2024 | British retail data was soft again, for the second consecutive month. We are noticing much stronger data around sales seasons, and weakening in normal selling period. This suggests that consumers have become more aggressive in hunting for deals. Despite the weakness, there’s nothing in the data which would suggest that the technical recession will persist in the next few months or that the retail sector is in peril. Inflation is coming down and should come down further when energy price caps are lowered in April. External demand is weak but stable, and the Bank of England will likely begin rate cuts soon alleviating mortgaged households. |

| March 2024 | The British consumer remains resilient. While a 0.2% monthly rise in core retail sales may seem anaemic, it is still higher than expectations. With the exception of household goods and food stores, all categories, including clothing, saw rising volumes. Today’s number confirms that consumers are upbeat and gives confidence that Britain will likely not be too hard pressed to escape the technical recession. The figure is robust enough to suggest an economic rebound, but not strong enough to knock the Bank of England off its present course towards rate cuts. We thus believe rates will still come down probably during or slightly after the summer, further empowering British consumers. |

| February 2024 | The retail sales number -surprisingly- blew past expectations, rising at the fastest pace in nearly three years. As inflation moderated, consumers hit main street and opened their wallets in January, in every category of bar clothing. The data release is a very positive read for the UK economy going forward, and consistent with our view that a UK recession will not necessarily deepen or indeed last long. Slower online retail sales are a cause for concern, however, and we would expect this category to pick up too, before we talk about any sort of a sustainable bullish consumer trend. |

| January 2024 | "The number is perplexing to be sure. Stronger GDP and inflation data should have been accompanied by stronger consumption. Nevertheless, we remain positive. Higher prices have not made consumers disappear. But they have made them more selective. Consumption was higher last year when good opportunities arose, and of course during the festive season. The data is encouraging. Even though economic activity is projected to be more sluggish in the first six months of 2024, consumers are optimistic enough to keep the economy at an even keel, and contribute to a rebound when interest rates begin to drop."   |

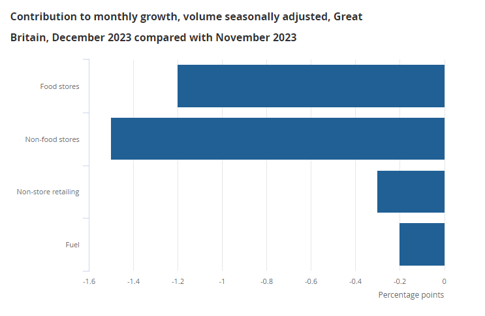

| December 2023 | "This is the first sign since the summer that consumers might be breaking free from their rut. With energy and transportation inflation cooling, consumers have more disposable income translating into increased retail sales during the busy season. Having said that, we are still sceptical about what lies ahead. Inflation remains volatile, forcing the Bank of England to maintain a tight grip on the economy. While consumers treated the inflation drop as a windfall and upped spending, we are very far from stable positive growth rates." |

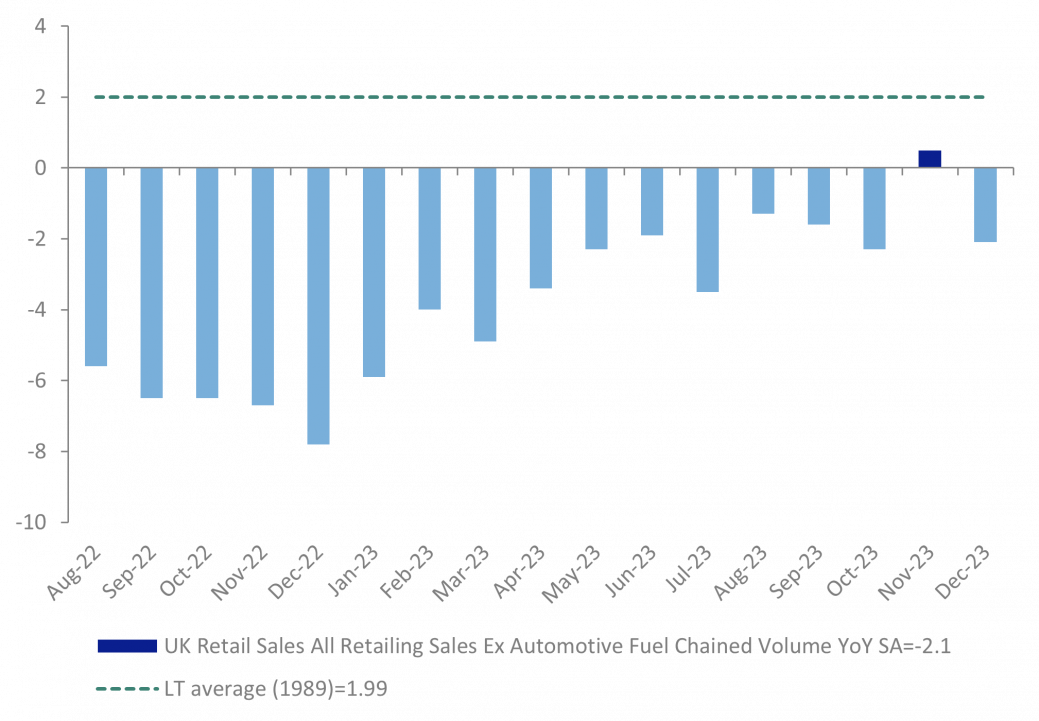

| November 2023 | "The number is certainly bad, but also consistent with the previous bad number, slower growth figures and lower inflation. We are therefore looking at one of two possibilities. As inflation falls to manageable levels and the US central bank has all but announced a stop to its rate hike cycle, we also expect the Bank of England to abstain from increasing rates. Consumers who won’t fear higher mortgage payments going forward could be more confident. Those who are increasingly looking for better deals might just be saving ahead of Black Friday and Christmas. However, we could be at a breakpoint in terms of consumption across all sectors. We, thus, believe that instead of basing our predictions on the current number and the November figure, we should wait and gain a clearer picture of consumer appetite after January." |

| October 2023 | “Retail sales for September were expected to slow down; however they were significantly weaker than predicted. Despite the robust wage growth, consumers are growing weary of paying higher price tags for products and services. With oil prices increasing and rising tensions in the Middle East, inflation continues to eat away at real incomes. We expect that consumer spending will continue to slow down, across the board. Higher-end retail may continue to buck the trend, as it does even in times of crisis, but we expect most households to pull back on further spending as their heating bills rise. The next two months leading up to Christmas are crucial for retailers and we expect fierce competition with early promotions and significant discounting to attract customers.” |

| September 2023 | “Retail sales are slowing, but remain above expectations. Despite high interest rates and inflation eating away at real incomes, consumers are showing resilience. Given that we are very close to the end of the rate hike cycle, we expect this resilience to persist across most categories. Retailers will remain focused on cutting costs and creating value deals in the lead up to the bumper Christmas period.” |

| July 2023 | "UK consumers appear to be resilient as sales unexpectedly increased for a second month, despite the sticky inflation. However, the odds are stacked against them. Despite a drop in inflation figures, interest rates are expected will probably continue to continue affecting the nation in the next few months, further depressing consumption and possibly leading the UK into a recession. The slowdown is expected to be broad-based. As household budgets continue to be squeezed, retailers need to acknowledge that customers are affected in different ways and will need to be more innovative on sales offers and discounting." |

| June 2023 | "Sales surprisingly grew helped by the warm weather and extra May bank holiday for the Coronation weekend. Whilst confidence rose, the outlook is bleaker with inflation much too high for comfort and a continued tightening of household budgets. The central banks appear to be pulling out all stops in order to curtail consumption and bring prices down and we don’t expect any giveaways from the government. The economic environment will remain challenging over the summer for retailers who will need to focus on reducing costs, increasing promotions and bundling great product offers to attract customers". |

| May 2023 | “We saw the anticipated return to strong growth for footfall and sales volumes in April after stubbornly high inflation and poor weather caused a drop in March. However, food prices continue to surge to historic highs, which is concerning for households. The cost-of-living crisis is not going away and we expect consumers to continue tightening their budgets and delaying big ticket purchases. In the following months, we anticipate that retailers will continue to focus on reducing costs, and fight against these challenges, bundling for value and driving efficiencies across the business”. |

Expert analysis on the latest consumer industry insights in the UK.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.