Consumer insights

Expert analysis on the latest consumer industry insights in the UK.

The FCA authorisation process requires firms to demonstrate that they can meet certain standards known as ‘Threshold Conditions’. Firms must have:

They must also comply with the applicable FCA rules in the FCA Handbook, including the twelve Principles for Businesses (PRIN). Principle 12 relates to the Consumer Duty and the supporting rules are set out in PRIN 2A.

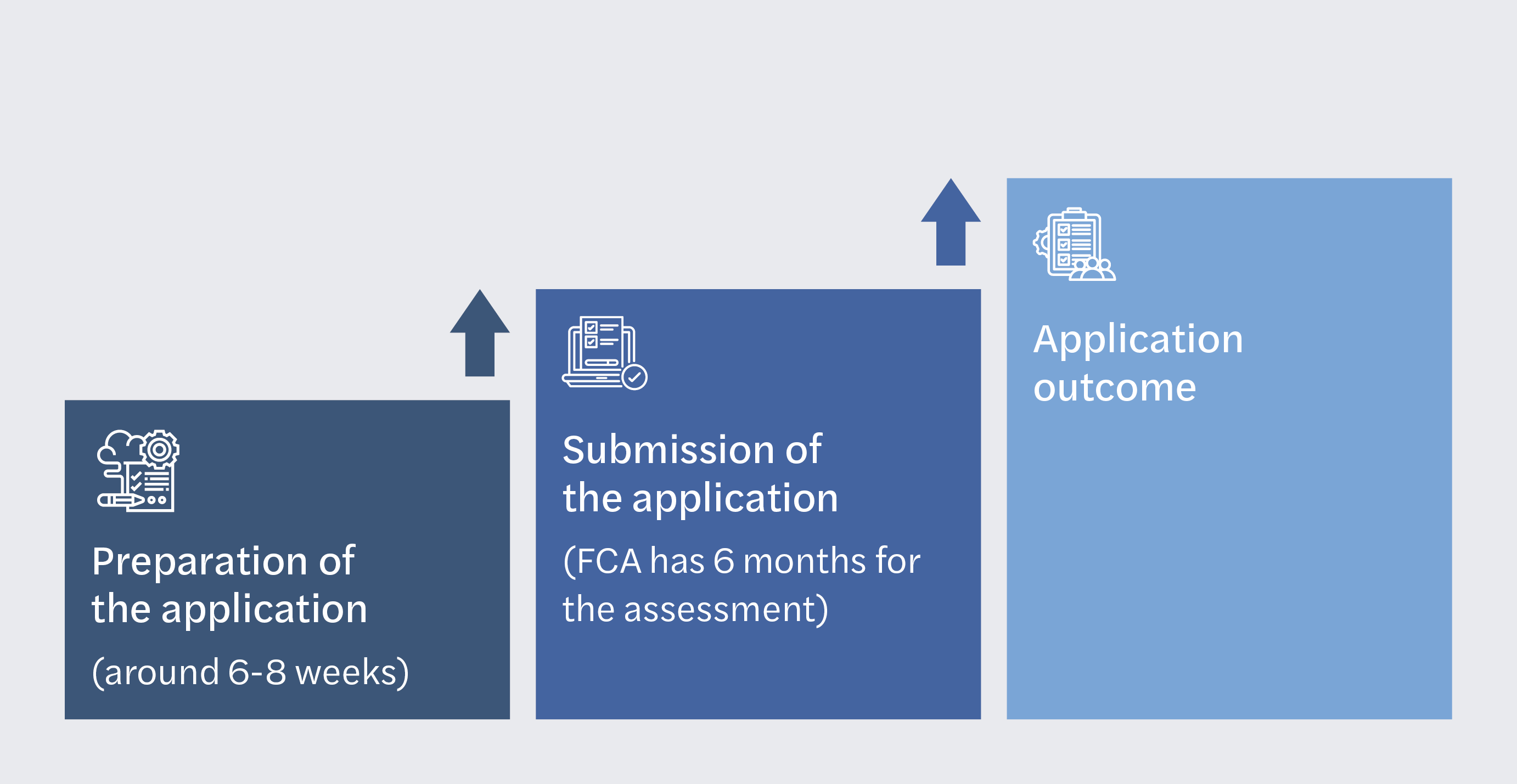

Retailers should allow sufficient time to prepare their application material. The application process includes the submission of a detailed regulatory business plan, an application form and supporting documentation through the FCA’s online Connect system. The FCA’s processing time can take up to six months, or more if the FCA requests further information or considers the application to be incomplete at the time of submission.

Once the FCA has approved the application, the firm will be added to the Financial Services Register and assigned a Firm Reference Number (FRN). Firms may find the FCA webpage ‘Information for newly authorised firms’ useful to refer to.

The Consumer Duty should be embedded throughout every aspect of the authorisation application. The FCA will assess the application for evidence that a firm has put the customer at the heart of what they do; from their culture, systems and controls to training and ultimately the design and distribution of products and services.

Firms need to demonstrate that they understand how the Consumer Duty applies to them and how they will act to deliver good customer outcomes by ensuring that:

Within the application form, retailers have the opportunity to highlight how their firm is structured in order to meet the standards expected under the Duty. For example, a robust risk management framework, strong systems and controls and comprehensive compliance procedures and monitoring plans will all contribute towards good outcomes.

The FCA’s sample business plan now includes a section on the Consumer Duty which retailers may find helpful to refer to for in-scope business. Key areas include:

Fair value: It is important that retailers invest adequate time into determining their specific target market and understanding relevant characteristics and behaviours. This will enable the retailer to design and complete relevant fair value assessments that consider the full benefits and costs to the consumer of the products and services it intends to provide. Customer segmentation, commission and profit margins throughout the distribution chain should be carefully factored into this assessment.

As an example, the FCA expressed concern that some Guaranteed Asset Protection (GAP) products do not offer fair value to customers. Only 6% of the amount customers paid in premiums were paid out in claims. Whereas some firms, such as motor dealerships, were seen to pay out up to 70% of the premiums in commission to parties within the distribution chain suggesting a systemic value issue. Retailers should consider the level of commissions paid throughout the distribution chain and ensure the amount can be justified.

Communications: For retailers, it will be crucial to have specific policies and procedures in place setting out how communications, marketing, financial promotions and T&Cs are tested and approved, taking into consideration the characteristics of the target market.

Retailers are increasingly providing customers with the option to split the cost of purchases into regular interest-free repayments through Buy Now Pay Later (BNPL) services, sometimes alongside other regulated lending products. While BNPL is not currently a regulated activity and retailers do not need to be authorised by the FCA to provide these services, it is an area with a high risk of harm to consumers. This is due to the rise of customers accessing these services and missing payments, potentially resulting in defaulted accounts, charges and additional interest. To mitigate the risk of harm from lending products, key communications need to be visible, timely and easily understandable for your audience. In particular, the terms of the product and interest rates added after the interest-free fixed period should be clearly communicated and accessible to the customer.

Monitoring outcomes: Having good quality data and the ability to monitor and analyse customer outcomes is central to the Duty. Firms should have established reporting capabilities to illustrate how management information (MI) will be escalated from frontline teams to committees and eventually, the Board for appropriate action to be taken where there is evidence of poor outcomes. If your business is not yet trading, it will not be possible to assess customer outcomes delivered yet. However, the FCA expects firms to demonstrate that they have the policies, processes, systems, controls and people to comply with the Consumer Duty.

For Big Tech retailers that are providing financial services, there is a concern that these types of firms might hold an unfair advantage due to their access to unlimited customer data and biometrics. The regulator believes this can pose various risks to the market, such as influencing the customer journey with the manipulation of data collected on behavioural biases through social media platforms. Within the application, retailers should be transparent about any plans to harness their data capabilities to monitor good outcomes and be open with the regulator (and consumers) on the data held and its use.

Consumer Duty Champion: If your firm has a board, then the regulator expects that an individual of significant seniority holds the role of the Consumer Duty Champion. Their role is to champion Consumer Duty across the business and provide a senior level of challenge around customer outcomes being provided - based on the MI and monitoring being conducted.

Supporting information may also include your firm’s financial forecast, fair value assessment framework, product testing arrangements, and other policies and processes, such as those relating to the identification of the target market.

We have a specialist Regulatory Compliance team, who are experienced in assisting firms throughout the authorisation process. We have proven experience in:

We have a wealth of experience in assisting firms to gain FCA authorisation and to meet the new Consumer Duty.

If you would like to speak with a member of our Financial Services team, please contact us or to submit Request for Proposal documents, use the link below.

Expert analysis on the latest consumer industry insights in the UK.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.