Want to know more?

As published by the FED in a note on July 15, 2019, there are many ways to backfill the SOFR time series.

The publication of the pre-production estimates of SOFR going back to 1998 allows banks to study the SOFR data characteristics and to compare it to other rates, such as the US repo and the Effective Federal Funds Rate (EFFR).

Even though SOFR is a secured rate while EFFR is unsecured, it is expected that the SOFR daily moves will remain close to the EFFR’s: “Using this longer historical series, we can gain a greater understanding as to how a rate like SOFR should be expected to behave. […] despite the fact that it is a secured rate and has some day-to-day fluctuations, SOFR should be expected to move very closely with Federal Reserve policy and very closely with overnight unsecured rates like EFFR over time”.

In this context, Mazars implemented primary statistical studies in order to assess the relationship between SOFR and EFFR, based on the daily observations of the swap rates provided by Bloomberg. We noted that EFFR has a strong positive linear relationship with SOFR: the correlation coefficients exceed 90% for all the swap rate maturities. Additionally, the linear regression of SOFR over EFFR per swap underlying tenor shows that for all the tenors, the explanatory power (R2) of EFFR is higher than 70%. Following these results, Mazars supports the FED recommendations and expects SOFR backfilling methodologies by banks to be consistent with those for risk modelling purposes.

Building proxies on the implied volatilities of SOFR is important for both risk and pricing models. Unlike risk models, which aim to reconstruct the past for calibration purposes, pricing models intend to predict the future. However, whatever the methodologies, when building proxies to determine RFR volatility, consistency is of the utmost importance. Indeed, many risk models are based on historical scenarios and on portfolio sensitivities to risk factors: historical scenario modelling is derived from historical data, e.g. in the current case of the backfilled data, the sensitivities are computed based on pricing modelling. As a consequence, coordination is required among front office, quants, market experts, and risk modellers to define appropriate and meaningful estimates of SOFR volatility.

Inspired by Fabio Mercurio’s article ‘A Note on Building Proxy Volatility Cubes’ in which he explains the general dynamic model, we can make the following assumptions:

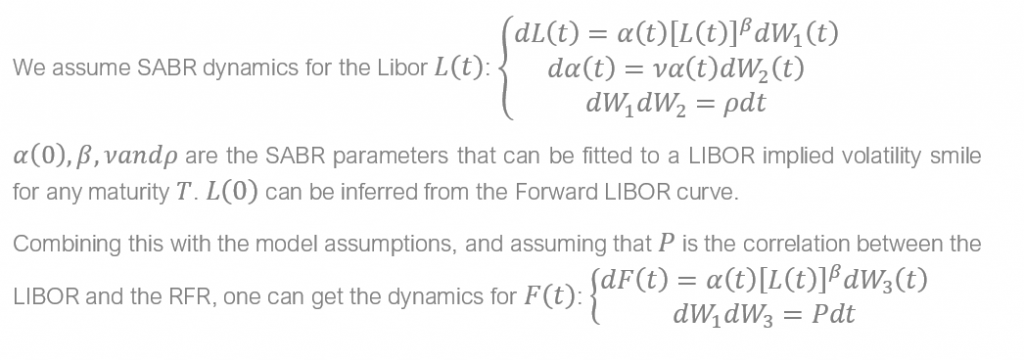

2.2.1 Model assumptions

2.2.2 Model outputs

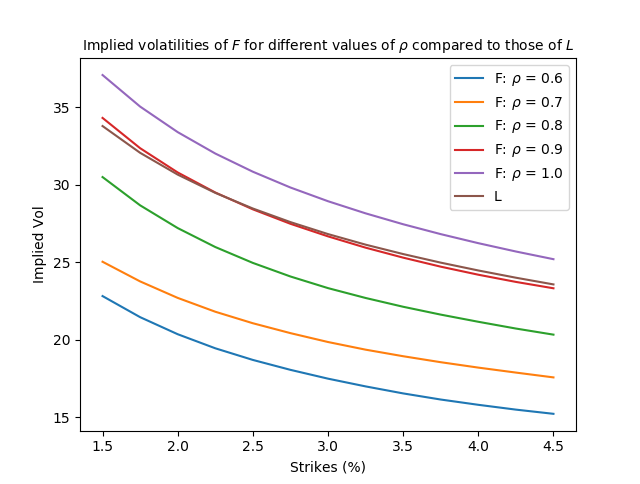

Figure 1: implied volatilities of aRFR for different values of, and implied volatilities of Libor.

This example shows how an implied volatility smile for the RFR can be produced based on given LIBOR smiles in a consistent and arbitrage-free manner. However, even though the shifted-lognormal model can well approximate smiles around the ATM level, it cannot capture the richness of observed volatility smiles in practice. It is our opinion that the special assessment baseline review (SABR) model which attempts to capture the volatility smile in derivatives markets, could help improve this result.

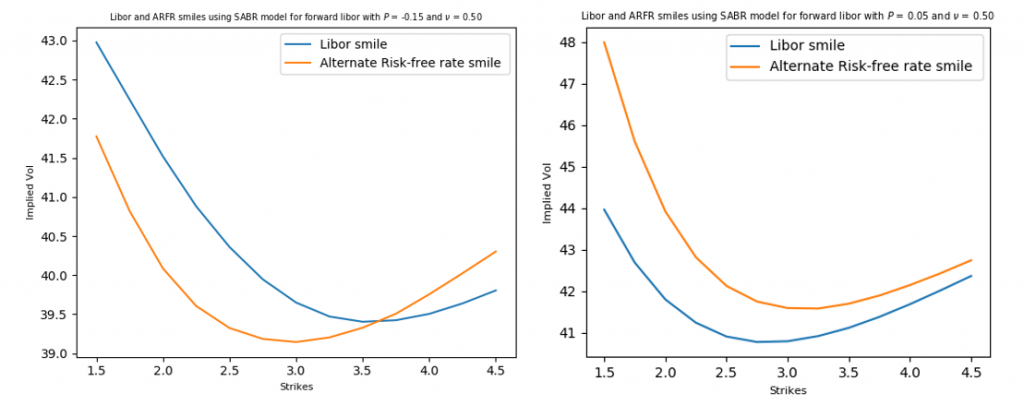

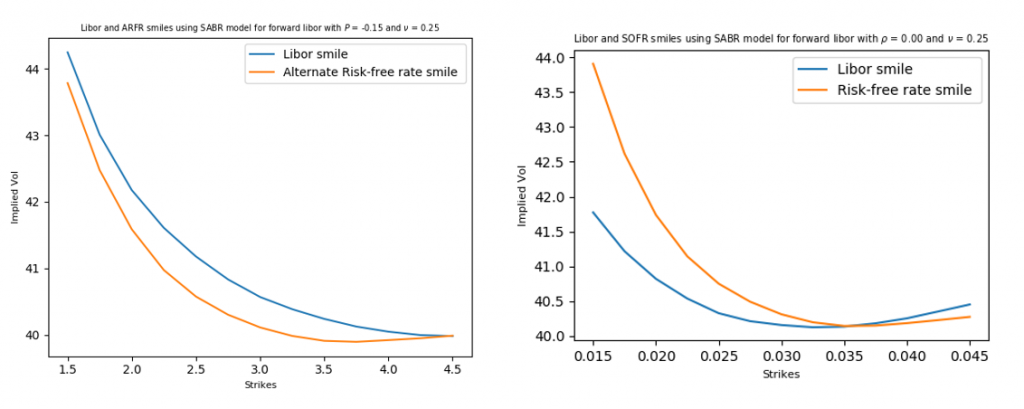

2.3.1 Model Assumptions

2.3.2 Model Outputs

Figure 2: Outputs of SARB model

While the shifted-lognormal was restrictive in terms of the shapes of volatility smiles, the SABR model returns different implied volatility shapes (smile as well as skew) by varying the SABR parameters. Correspondingly, we get the implied volatility smile for the RFR.

Proxying the risk factors of the RFR is required to build and calibrate interest rate (IR) risk models. These proxies must be aligned with the Fundamental Review of the Trading Book (FRTB) regulation and are determinant of the definitions and assumptions of the methodologies designed under the Internal Model Approach (IMA) requirements.

RFRs will be the reference rates when FRTB-IMA comes into effect and should be considered as the reference rates in the IR risk factor definition under FRTB. Hence, institutions need to have adequate IT resources and systems as well as quantitative skills to take into account the IBOR transition impact on the FRTB implementation. This includes the design and implementation of libraries relating to RFR curve construction, calibration of the Expected Shortfall (ES) IR models and assessment of potential Non-Modellable Risk Factor computation arising from the use of the data proxies for modelling of either LIBOR or RFRs risk factors). For further examples of data proxies, please refer to our article.

Article written by Mariem Bouchaala.

6 August 2020

Paving the way for transition towards an IBOR-free world.

The revised market risk framework – also known as the Fundamental Review of the Trading Book (‘FRTB’) – not only impacts an institution’s regulatory capital charge calculation for market risk, but also affects operational, governance and business strategies.

The latest IBOR related insights and analysis

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.