The economy & your investments

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

Shadow banking and the risk to banks

What links the two is the involvement of shadow banks. Shadow banks, or nonbank financial institutions (NBFIs), are entities other than banks that manage household and corporate savings, deploying these to finance the economy. NBFIs include any investment funds, ETFs, insurance companies, or any entity which raises funds for investment.

The LDI crisis evolved as falling gilt prices in September 2022 sparked margin calls within pension funds. Pension funds take private savings and lend them out in the broader economy by purchasing government bonds and other securities. These NFBIs are systemically important in that they are large enough owners of government bonds that when they reduce their holdings this causes prices to fall, and if they were to fail this would also have wider ramifications in the economy.

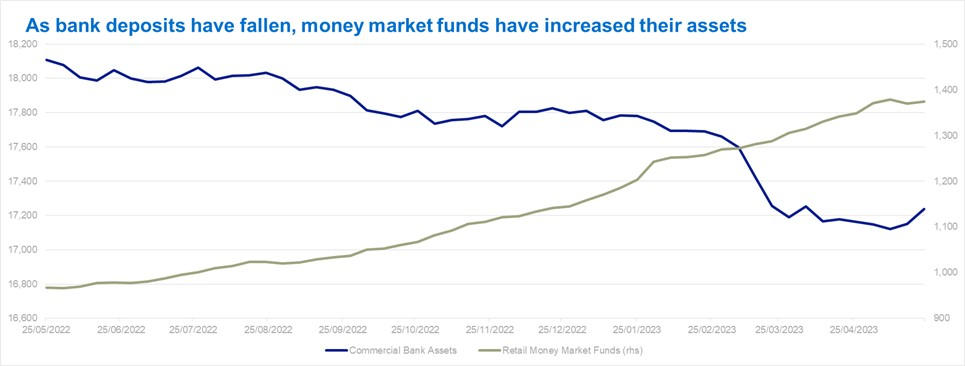

The link to NBFIs in the second example is more obscure but still relevant. Funds started leaving Silicon Valley Bank because the rates available to depositor holders did not reflect the increases in the US Federal Funds Rate or the returns available in other fixed interest instruments. Banks don’t pass on the market rate of interest in order to maximise the spread between their borrowing costs and lending rates. As interest rates have risen, deposits have made their way out of banks and into other institutions where better interest rates are available, including money market funds, an NBFI.

As is often the case these two instances seem distinct as they occur. However, over time they will be linked as people become increasingly aware of the risks posed by financial entities that are not comprehensively regulated. Given the size of NBFIs, the risks are considerable.

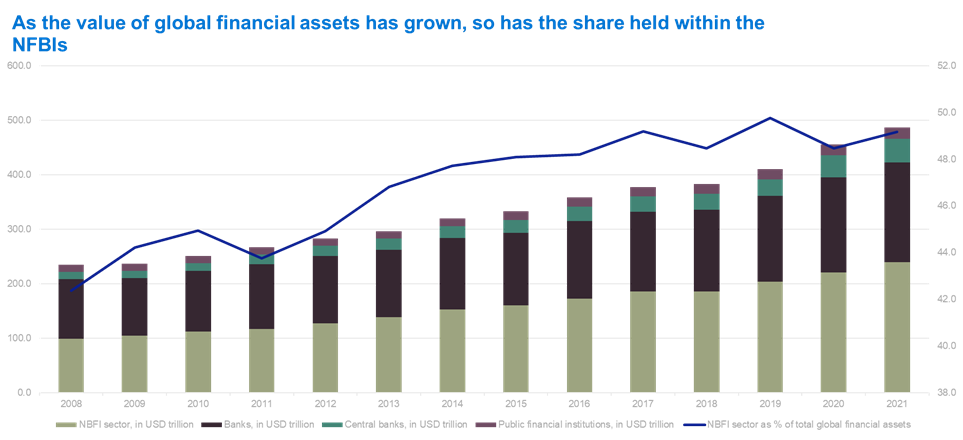

At the end of 2021, the total value of assets in NBFIs had grown 140% to $239bn from 2008 and the share of global financial was 49%, up from 42% over that period. As of 2021, the share of assets within NBFIs exceeds that in banks by one third. However, the regulatory regime and supervision for NBFIs are much less stringent and this can have unintended within both NBFI and banking sectors.

A paper from the New York Federal Reserve published in March tackles the hypothetical threat to banks from a fire sale of assets within an NBFI, similar to the LDI crisis in the UK.

An example of a first-order effect would be if a NBFI was a bank counterparty and failed meaning it was unable to honour its obligations. This would reduce bank profits and if the loss were large enough could impact the viability of the bank.

Second-order ramifications could be much wider in the event of a fire sale of assets, stemming from the falling price of the asset price. A forced sale of corporate bonds by an investment fund could heavily depress prices, this could cause losses directly with banks holding those same assets and could also impact life insurance companies holding those bonds in the same way. Life insurance companies could de-risk in this situation and reduce other assets, which the banks also hold, and again bank profits diminish by falling asset prices. Due to the interconnectedness of financial markets, these shockwaves can spread throughout the entire financial system.

The ECB’s most recent Financial Stability Review echoes the risk of contagion between NBFIs and banks and also highlights some of the key risks facing the sector. 18% of bond funds’ assets, including almost all of the banks’ contingent convertible bonds (such as those bonds that were wiped out when Credit Suisse was taken over by UBS this year), are held within NBFIs. It is also aware of concerns that we have raised previously where investment funds offer regular liquidity to investors, despite holding illiquid assets, such as commercial property or private equity. Redemptions of commercial property have been increasing since 2020 as valuations have been falling, which could trigger forced selling and a correction in real estate prices.

Against a backdrop of tighter central bank policy and economic uncertainty, it is not hard to see how issues could emerge within NBFIs and spread both to other NBFIs and the banking sector. While it is tempting to think that markets have turned a corner after 2022, central banks are clearly concerned about the risk of falling asset prices infecting the broader financial system and banks.

James Hunter-Jones, Senior Investment Manager

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

“What if I could tailor my investments to my needs?”

Read our latest news and analysis on the changing markets and economic environment.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.