The economy & your investments

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

Has the demand for oil finally peaked?

Peak oil is a term that is increasingly used during discussions about reducing reliance on fossil fuels. The logic is that, as consumption of fossil fuels falls, we inevitably get closer to reaching peak oil and from then on, the amount of oil consumed each year will fall.

Data supports this, last year Americans clocked up more miles than they did in 2019 but only used 6% gasoline, reflecting greater efficiency and usage of alternative fuel sources. Electric and hybrid vehicles now make up 15% of car sales (May 2023), up from 4% in 2020.

While this evidence is only derived from the US, it is still significant as the US accounts for 34% of petrol consumption and 9% of oil demand. Understandably, data like this bodes ill for the oil price both in the short and longer term.

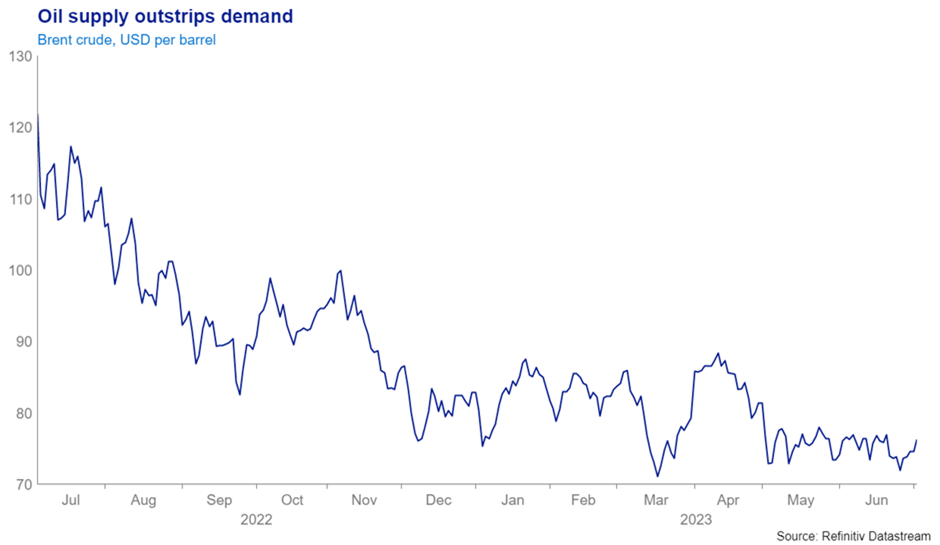

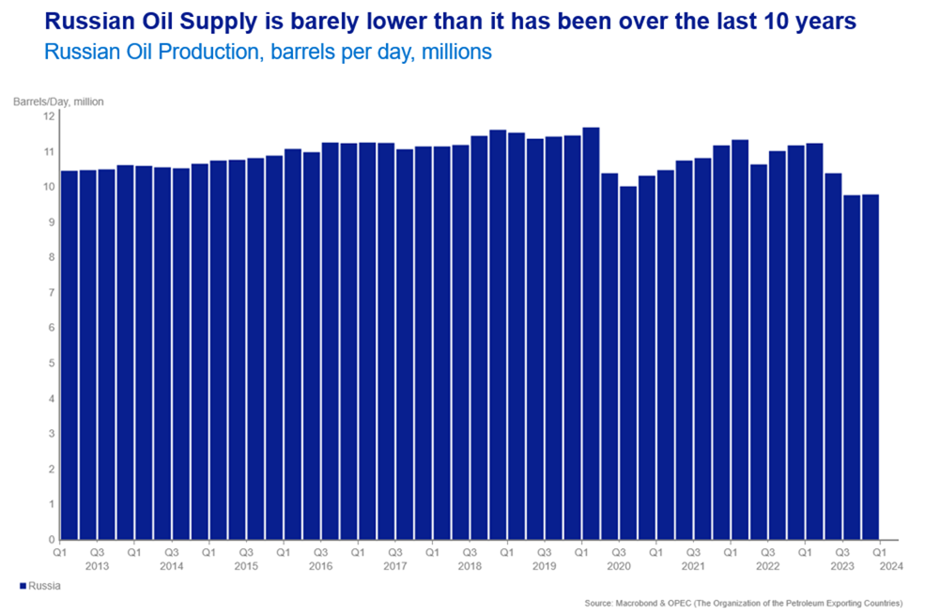

While the price of oil spiked in 2022, due to Russia’s war with Ukraine, the price has steadily declined. On two occasions in 2023, OPEC+ announced price cuts but this has failed to spur higher prices. One reason is resilient Russian production, Russian oil exports to Europe may have ceased in 2022 but exports to other countries, notably China and India have persisted, and at a discount to market prices.

Expectations for oil demand have also been falling as has global economic growth in 2023. China’s economy reopened at the end of 2022 to much fanfare from economists but the rebound in economic activity has remained elusive and oil demand from the Middle Kingdom will remain subdued.

One should not rule out price spikes though. Firstly, when there is little hope for an asset price, any positive news or change in sentiment can send the price higher as negative positioning reduces.

Secondly, the US could restore its strategic petroleum reserves. These were drawn down in 2022 to soften the impact of disruptions to Russian supply and were they to be replenished, the oil price would be sent higher.

Finally, producers may respond to the low prices and prepare for a world of decreasing oil demand. Any reduction in investment and a corresponding decrease in production could cause an imbalance that sends prices higher. Refiners are likely to switch their output to favour diesel over petrol, as cars are increasingly powered by electricity and again, a mismatch in supplies of products would push prices higher.

The moral of this story is that asset prices tend to defy conventional wisdom. Currently, the market is anticipating lower oil prices amid oversupply and lower future demand. Investors would be wise to be contrarian and hedge against an unexpected rise in the oil price.

James Hunter-Jones, Senior Investment Manager

On Wednesday 26 July, join our Chief Economist and Chief Investment Officer as they discuss the current economic landscape, both here in the UK and globally.

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

“What if I could tailor my investments to my needs?”

Read our latest news and analysis on the changing markets and economic environment.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.