What changes does the Basel 3.1 framework bring to the banking sector?

Basel 3.1 seeks to make two considerable adjustments to the regulatory landscape. The first will materially alter the composition of capital requirements by making major underlying changes in the calculation of Pillar 1 capital. In particular, this relates to credit, market and operational risk. While the second will make the capital regime more risk sensitive.

The aim of the regulations is to reduce the likelihood of future banking crises by encouraging transparency and more standardised practices, ensuring that banks have a more accurate and comparable assessment of their risk exposure.

Basel 3.1 is likely to have a significant impact on a large number of regulated banks and building societies in the UK. The scale of the changes being proposed, and their materiality, means this will be one of the most significant regulatory challenges facing firms in the medium term.

Who does Basel 3.1 apply to?

The PRA will replicate the scope of application currently in place under the CRR, with a few significant exceptions. The current framework applies to:

- PRA-authorised banks and building societies.

PRA-approved or PRA-designated holding companies and building societies. - Small domestic deposit takers (SDDTs) will be able to join the Strong and Simple Framework, a more proportionate prudential regime for less systemically important banks and building societies.

How will Basel 3.1 be implemented in the UK?

The current state of Basel 3.1 implementation in the UK is progressing steadily. The Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) have been working closely with banks to ensure a smooth transition and adherence to the new regulations.

Basel 3.1 has several impacts on the UK banking sector. One of the key objectives of the framework is to enhance the risk management practices of banks, particularly in relation to capital adequacy. Banks must therefore assess regulatory capital requirements more accurately, to absorb potential losses, reducing the risk of financial instability.

Basel 3.1 introduces stricter rules for measuring and managing risks, including credit, market, and operational risks. This encourages banks to adopt more robust risk management frameworks and processes to improve the sector’s overall resilience.

The implementation of Basel 3.1 also aims to promote transparency and accountability in the banking industry. Banks are required to enhance their reporting and disclosure practices, providing stakeholders with more comprehensive and timely information about their risk profiles and financial positions.

How did we get to Basel 3.1?

The Basel Framework can be traced back to four key instances. These are:

- The Basel Committee on Banking Supervision: The committee, comprising banking supervisors from various countries, responsible for developing and maintaining the Basel Framework.

- Basel I: The first iteration of the Basel Framework introduced in 1988 focused on credit risk and established minimum capital requirements for banks based on their risk-weighted assets.

- Basel II: Introduced in 2004, Basel II expanded on Basel I to introduce additional risk categories, including operational risk and market risk, providing more detailed guidance on how banks should assess and manage these risks.

- Basel III: Basel III, introduced in response to the 2008 financial crisis, further strengthened the regulatory framework by increasing the quality and quantity of regulatory capital banks are required to hold. It also introduced measures to address liquidity risk and leverage ratios.

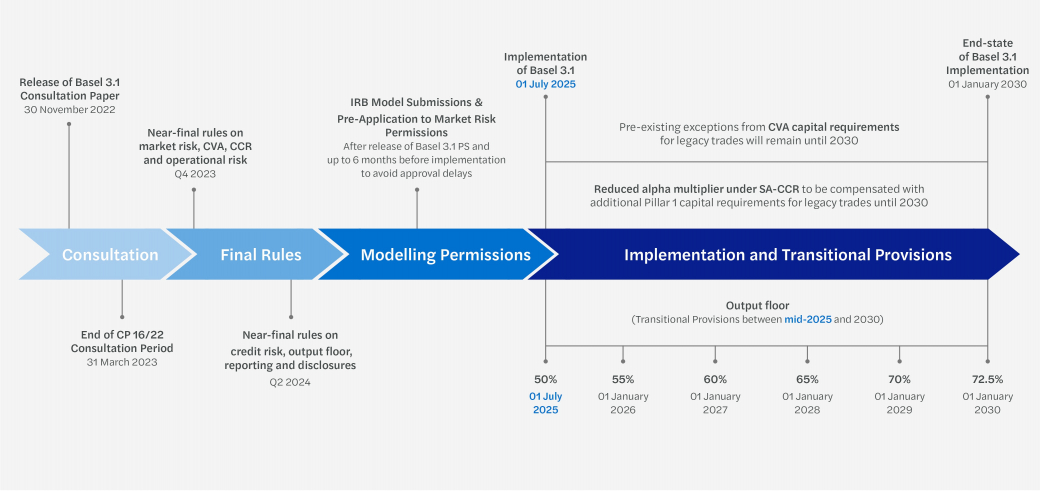

Expectations ahead of final Basel 3.1 rules

Pending the release of the PRA’s Basel 3.1 final rules, our banking risk experts discuss the proposed changes to credit risk and output floor rules, as well as the near-final rules relating to market risk and operational risk.

Data implications of Basel 3.1

The Prudential Regulation Authority (PRA) continues to emphasise the importance of the reliability and accuracy of regulatory data for banks and building societies. Data risk is named a main priority within the 2024 Dear CEO Letter and through the Transforming Data Collection initiative between the Bank of England and the Financial Conduct Authority.

Basel 3.1 – Near-final rules part 1

Policy statement 17/23 (PS17/23) contains Basel 3.1 near-final policy materials for market risk, credit valuation adjustment (CVA) risk, counterparty credit risk and operational risk.

Basel 3.1 – Understand the regulation

In this series of short articles, our Prudential Regulation Consulting team delves into the implications of Basel 3.1 changes on banks.

Basel 3.1 video series

Basel 3.1 is the final set of amendments to the capital regime for banks after the Global Financial Crisis. The Prudential Regulation Authority (PRA) proposed that the implementation date for the changes would be 1 July 2025. In this series, we take a closer look at what firms need to consider before these reforms will be live in the UK.

Credit Risk – Standardised Approach

The PRA has proposed several changes to the Standardised Approach for credit risk which could have a significant impact on the risk-weighted assets (RWAs) of UK CRR firms.

Credit Risk - IRB

The Prudential Regulation Authority’s (PRA) internal ratings based (IRB) proposals largely align with the Basel standards and there is limited divergence between the PRA and the European Central Bank (ECB) on this topic.

Operational Risk

Let us help ensure that the proper procedures, processes, systems and external providers are in place to help manage risks and maximise opportunities in your business.

Market risk

Under Basel 3.1, the Prudential Regulation Authority has proposed to implement changes to how firms measure market risk. These include an amended version of the preexisting simplified standardised approach (SSA) and two new calculation methodologies – an advanced standardised approach (ASA), and a new internal model approach (IMA).

Pillar 2

You will find here a series of articles on Pillar 2. Enjoy reading.

Removal of the SME support factor

The PRA intends to remove the CRR SME supporting factor under the Standardised and IRB approaches to credit risk. This discount factor was introduced to limit disruption to the flow of credit to SMEs when stricter requirements were introduced after the Global Financial Crisis, in 2008.

Disclosures and Regulatory reporting

Under Basel 3.1, firms are classified based on a range of criteria, such as retail deposits, total assets, derivatives, complexity, or processes.

UK vs EU Basel comparison

Both the UK and the EU are consulting on the next wave of iterations to the Basel reforms. Whilst the focus of these consultations has been relatively broad, the rules around the computation of Pillar 1 Credit Risk RWAs seen the most significant change. This article outlines some of the main differences between the UK and EU approaches on this topic, along with our thoughts on these divergences.

UK vs US - Comparing Basel 3.1 implementations

The US unveiled its take on the BCBS Basel reforms on July 27th, 2023, calling it the “Basel III Endgame” (referred to as Basel 3.1 in the UK). This article outlines the key disparities between the US and UK approaches to implementing these reforms.

National contacts

Gregory Marchat Partner – Head of UK Financial Services - London

Huseyin Sahin Partner - Banking Risk Consulting London

Anindya Ghosh Chowdhury Director - Financial Services Consulting London

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

-

This website cannot function properly without these cookies.

-

Analytical cookies help us enhance our website by collecting information on its usage.

-

We use marketing cookies to increase the relevancy of our advertising campaigns.