The economy & your investments

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

UK Asset Prices – what are they telling us?

Conventional thinking is illustrated within the following example: the global economy experiences a slowdown, and a company that is reliant on exports experiences a fall in sales, which leads to lower profits than the previous quarter. As lower profits are reported the event happens within the economy, and this affects corporate profitability, which gets reported, and one would expect the company’s value to fall accordingly.

This is a flawed understanding. Where asset prices are freely traded, they reflect what investors think will happen, not what has already happened. A lot of resources are dedicated to understanding what will happen and how that will affect asset prices, and a large volume of assets are traded based on that understanding. Less liquid assets do not allow for such free expression of expectations, as we shall see.

Another nuance is whether they reflect the UK economy, or something else. As the former leading global financial centre, the UK is where many multinational companies are headquartered, but they do not tell us about the UK economy.

Considering the above, we will look at the UK economy through the lenses of UK large & mid-cap company share prices, UK government bond yields & real estate prices.

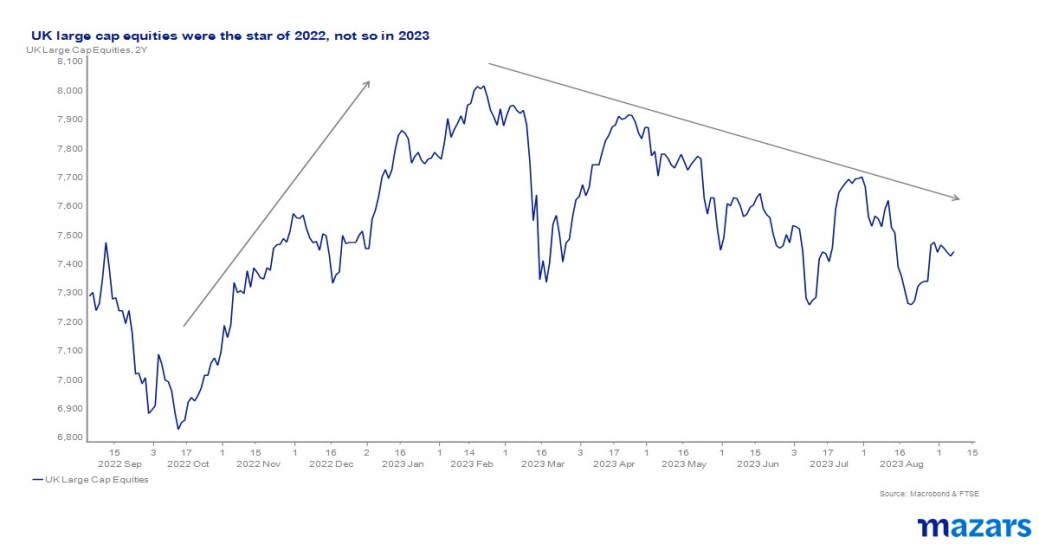

While the index of 100 UK largest shares is the most oft quoted share index linked to the UK, it is not a reflection of the UK economy. 70% of its revenues are generated abroad and the energy & basic materials sectors make up ~30% of the index. This means that a big driver of large “UK” companies is the energy price. This goes a long way to explaining the price performance of the index over the last 2 years as the oil price rose and fell.

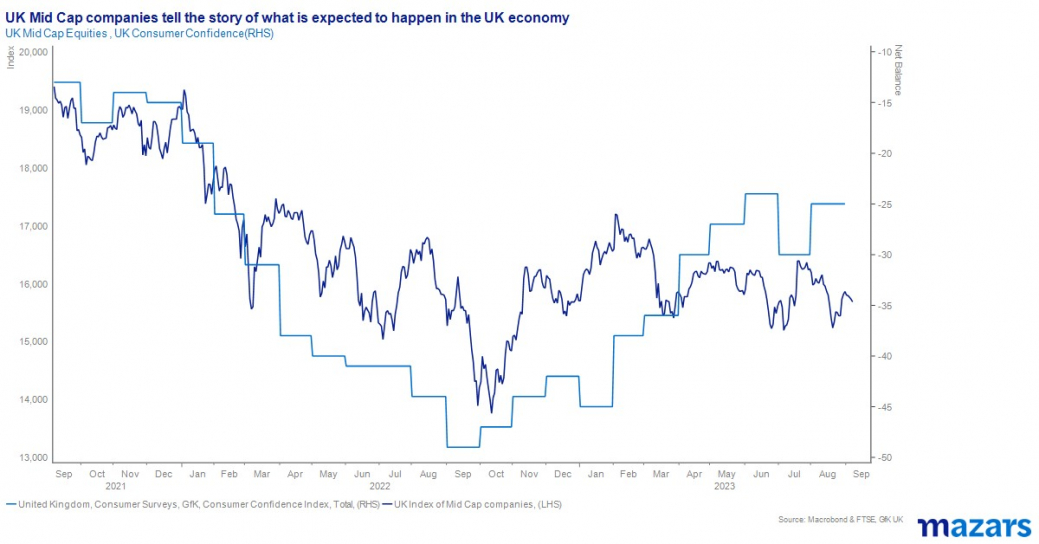

Medium sized listed companies are a better reflection of the UK domestic economy. The challenges facing the UK economy, coming from higher inflation and high interest rates, we well represented by consumer confidence. As UK consumers have been squeezed by higher costs, notably food & shelter prices the ability to the consumer is diminished.

The equity market bottomed in 2022 while pessimism was at a peak during the short reign of Liz Truss but the recovery has not been sustained, reflecting the challenging outlook that lies ahead for UK consumers as inflation remains elevated.

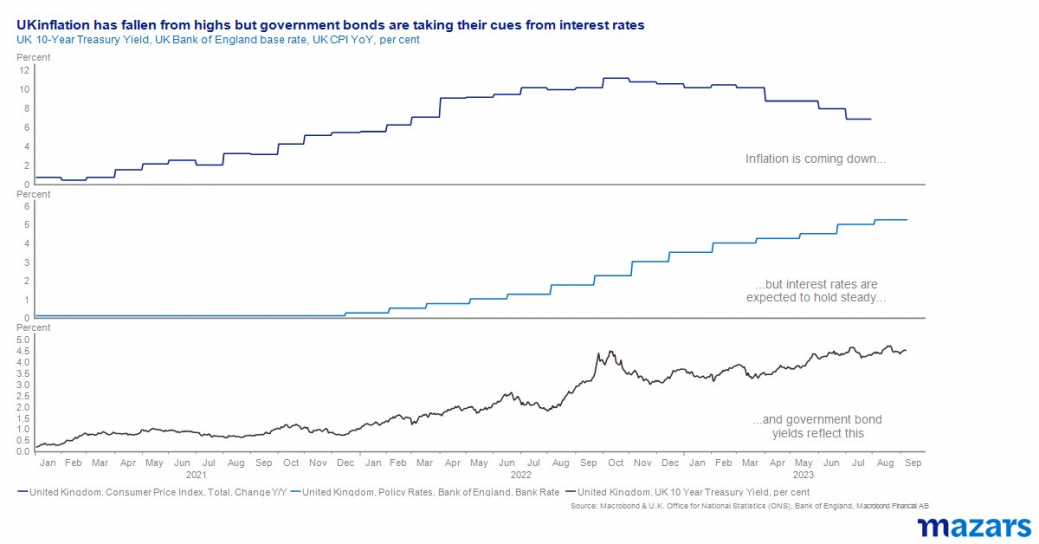

UK government bond yields are heavily governed by inflation & interest rate expectations. Inflation has been falling since November 2022 but remains well above the Bank of England’s target of 2%. While economic growth remains positive, although sluggish, the Bank of England will want to keep rates high to maintain downward pressure on inflation. UK government bonds are likely to continue to reflect that interest rates will remain high and will only come down in the event investors seek safety from volatility in other assets or when the economy weakens and inflation is under control and the Bank of England seeks to prop it up.

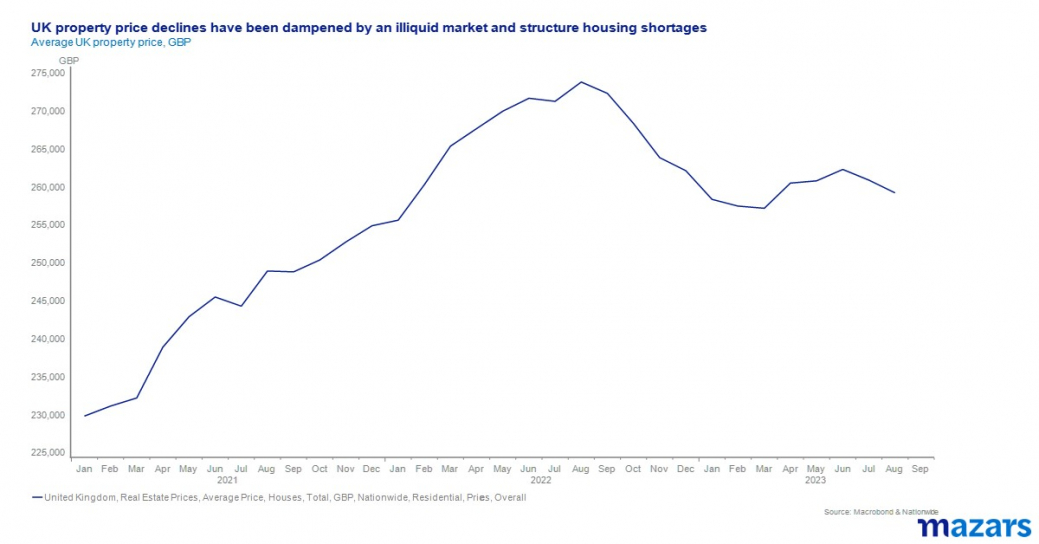

The residential property market has been under pressure following a rise in interest rates. The affordability of mortgages is a key driver of property values and so it follows that as UK interest rates rose from 0.1% to 5.25%, property prices should fall.

However, fixed terms on mortgages do not expire all at once, and sales do not go always through quickly, so the UK residential property market can reflect financial conditions with a lag. The residential market is also complicated by other factors, as only 30% of homes are owned with a mortgage and there is a chronic shortage of supply as the current government has consistently fallen short of its objective to build 300,000 new homes each year from 2017 to 2025.

We can infer from UK asset prices that an upswing in economic activity is not around the corner. Stagnant UK mid-cap company share prices do not speak of a return to robust consumer activity, while UK government borrowing costs remaining elevated tells us that interest rates are not forecast to fall soon. UK large cap companies should not be looked at as a barometer for the UK economy, and while house prices are not buoyant, there are factors which distort their reflection of the UK economy.

James Hunter-Jones, Senior Investment Manager

On the final Wednesday of every other month, our Chief Economist and Chief Investment officer discuss the current economic landscape and the impact on investors. Sign up below to join them at their next session.

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

“What if I could tailor my investments to my needs?”

Read our latest news and analysis on the changing markets and economic environment.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.