Latest economic, market and investment news

Read our latest news and analysis on the changing markets and economic environment.

Managing your wealth during times of volatility

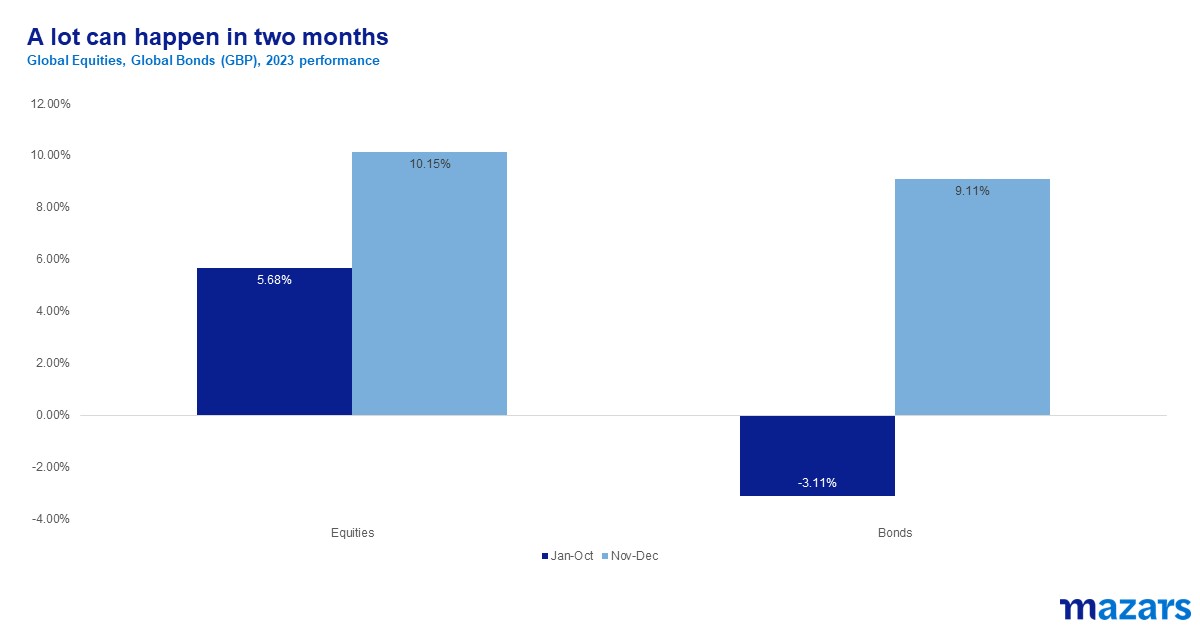

Global equities posted strong returns for 2023, boosted by technology stocks. Bonds were posting a loss up to the end of October but staged a remarkable comeback by the end of the year as the lower interest rates in 2024 became increasingly priced-in. As concerns have eased, we see reduced desire to lock in cash rates.

While the sun is shining it is worthwhile reflecting on the volatility of the last 2 years and the emotional pitfalls that volatility presents.

As is always the case, there are multiple lessons that one can take away from 2023. The rise of the so-called Magnificent Seven reminds us that we should not underestimate the rate at which technology can be absorbed and start benefiting companies’ profits; the robust global economy, which continues to defy recession fears, tells us that economists’ forecasts can materialize late or not at all, and that positioning needs to reflect this; and the exact timing of interest rate cuts is virtually impossible to predict, but if you get the direction of travel right, you can still make money.

For those who work with an adviser to manage their money, the above lessons are somewhat academic as you would expect said adviser to navigate these issues. However, delegating the task of managing money doesn’t mean that you lose all decision-making capacity, as you must still decide whether you continue to use an investment manager, whether you alter the investment strategy, or even encash the investments completely.

For those in this position, the lessons are not economic, but emotional. The importance is around your response to economic and market conditions rather than predicting them but mastering one’s response to them in the below situations can save time, effort, and money.

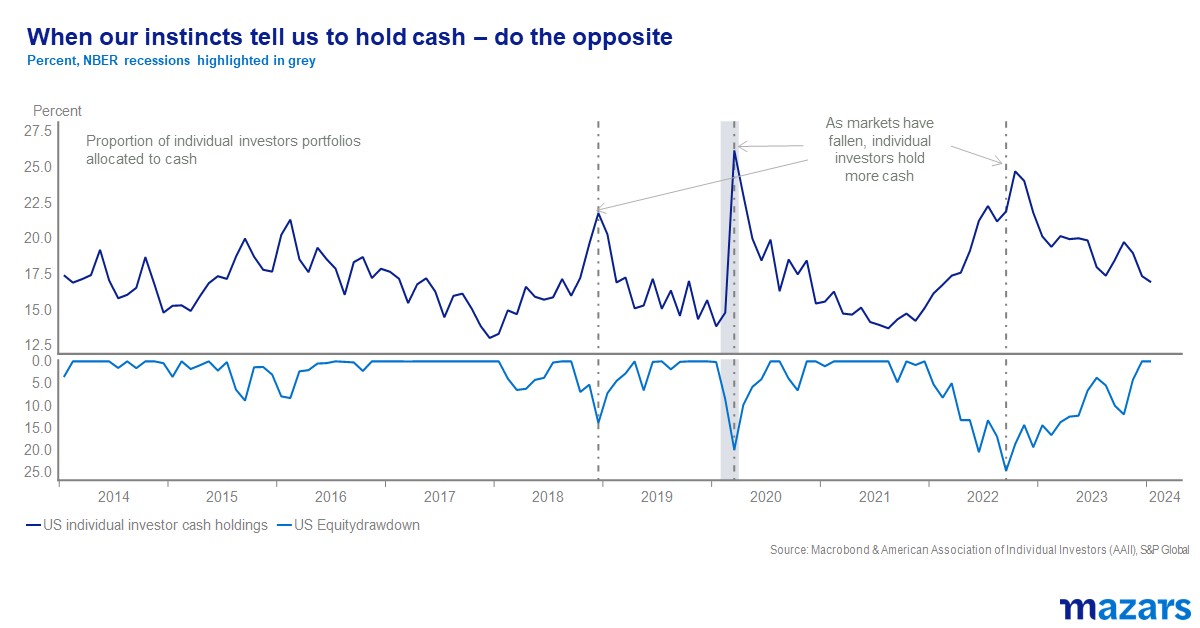

The considerable temptation that some face is selling investments as asset prices fall. From what I see when discussing this question with clients, some volatility tends to be tolerable but once the downdraft reaches a certain magnitude, the pain can become too much to bear, and selling is the only way to alleviate it. When investors reduce risk at the same time as everyone else in the market, they often have already endured the fall in asset prices and then do not participate once the recovery comes.

You convince yourself that you can sell now, avoid further decline in asset prices, and repurchase once things stabilise, but this is not borne out in the data. Aggregate data of past performances is a much more reliable indicator of the outcome you are likely to achieve and the below evidence this.

The chart shows that as US equities fall from their peak, retail investors’ allocation to cash increases. What you can also discern is by the time the market regains its previous peak, retail investors have a higher allocation to cash than when the drop first started.

This is evidence that cognitive biases and the efforts you make to avoid losing money in the short term detract from returns over time so there is a need to challenge what your emotions are telling you.

Another pitfall is mixing up what is happening in markets with the actions of the investment manager. This can happen in rising and falling markets and can lead to poor outcomes in both cases. In a rising market, investors are pleased with positive absolute returns and are not inclined to scratch beneath the surface to find out how good the performance is relative to the underlying benchmark. A fund appreciating by +10% in 12 months is welcome news, but not if the underlying benchmark has increased by +20% over the same period. The result is an investment manager not being challenged on their relative performance and, in the worst case, left in place when they ought to have been replaced.

On the downside, there is a similar requirement for understanding the full picture of an investment manager’s performance. When equities and bonds are falling, and the overall portfolio records a negative return I hear the question, “What is no longer working in your process, which worked so well before, as I have previously only seen positive annual returns?” What is often not well understood is that when asset prices in general are falling it is very unlikely that an investment manager will be able to defy gravity and avoid a negative return. Appreciation of this reality would prevent removing an investment manager who had performed well relative to their benchmark yet delivered a negative return.

There are lots of emotional responses to investments which are flawed, but these are among the most common. By understanding these and looking out for the symptoms in your thinking, you can reduce the risk of making one of these errors and focus on making more informed, rational investment decisions. Managing your emotions is not always the first thing that comes to mind when considering profitable investing but these cases above demonstrate that it might be more important than you previously thought.

James Hunter-Jones, Senior Investment Manager

Read our latest news and analysis on the changing markets and economic environment.

Global equity and bond markets enter 2024 with significant momentum from the last two months of 2023 fuelled by falling inflation and subsequent dovish projections from the US Federal Reserve.

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.