December 2023. Given the stock and bond market volatility, it’s hard to know what the starting point for equity valuations and rates as we enter 2024. At the beginning of the year, we said that volatility and geopolitical uncertainty will persist. Stocks and bonds were nearly flat by the end of October and are now up 10% and 5% respectively in just thirty days.

That’s volatility.

We now have not one, but two wars with potential geopolitical consequences.

That’s uncertainty.

While this Santa rally was, somewhat, anticipated, we don’t expect it to continue at its current breakneck pace. Quantitative Tightening (QT), the Fed’s practice of draining c. $80bn per month from financial markets and the continuous rise of real rates (ex-inflation) prohibit a lasting bull market.

And while one may argue that markets will rightly price in rate cuts mid-next year, it is exactly that pricing which brought the US 10y yield down from 5% to 4.3% and may end up nudging the Fed on a more hawkish path and they may want to omit phrases like “the market has done the tightening for us” in the future. Unlike the economy, markets move fast and can force the Fed to reverse course quickly, once again risking credibility.

Our projections are longer-term and apply to the whole of 2024.

1. Geopolitical tensions and geoeconomic fragmentation will linger.

We finish 2023 with two major wars that have geopolitical implications, as well as increasingly tighter global trade conditions. Slow growth and increasing borrowing needs will conserve the competition between key economic actors, incentivising governments to use any economic means at their disposal. As the pursuit of economic influence and the technological edge between China and the US intensifies, western-based supply chains will continue to shift away from China (a very long and arduous process) and into other countries, such as India.

On the other hand, China’s lacklustre economic growth may serve as an incentive towards reducing geopolitical entropy. All other things being equal, given current tensions, we think fragmentation will persist, but this will also lead to the formation of new alliances.

2. No sustainable bull market until Quantitative Tightening stops.

While we don’t often notice a bull market until mid-way through the next bear market, we feel that Quantitative Tightening prevents sustainably high equity returns. Quantitative Easing was the foremost driver of equity performance for the fourteen years prior to 2022. It stands to reason that the opposite, Quantitative Tightening, by and large, precludes a lasting equity bull market.

With rate cuts now considerably priced in, it would take a significant catalyst to bring equities near their all-time highs.

As conditions aren’t dire enough to initiate a bear market (bar a serious financial accident) and Quantitative Tightening prevents a lasting bull market, we believe that equity markets will likely continue to range-trade, even with a slight upward tilt.

The movement is likely to have a clear floor due to residual liquidity and decent fundamentals and a clear ceiling as animal spirits remain caged due to the persistent liquidity drain. The same rings true for bond markets. With inflation still volatile and central banks data-dependent, we should expect bond yields to oscillate. That bond volatility is the bigger problem for central banks. When long rates rise, so do mortgage costs. It does not matter whether they fall, even in the next few days, once they have risen past certain levels. Banks will retain the higher rate to guard themselves against further spikes that could increase their own financing costs.

Businesses and consumers will refrain from major spending decisions, for fear that costs might rise significantly during implementation. Apart from reigning in inflation, central banks will have to do a lot more to reduce macroeconomic volatility, which causes spikes in financing costs, ultimately hurting business investment.

While it is possible, of course, to have intervening rallies, as long as Quantitative Tightening persists we think it is highly unlikely we will see a sustainable, and broad-based equity rally.

3. Something may yet break. Central banks will probably react fast.

Real rates (ex-inflation), which matter for the economy, continue to rise, as nominal rates stay steady and inflation is falling. All other things being equal, monetary conditions should thus continue to tighten until inflation has dropped sufficiently to force central banks to climb down from the peak, towards the natural rate of interest.

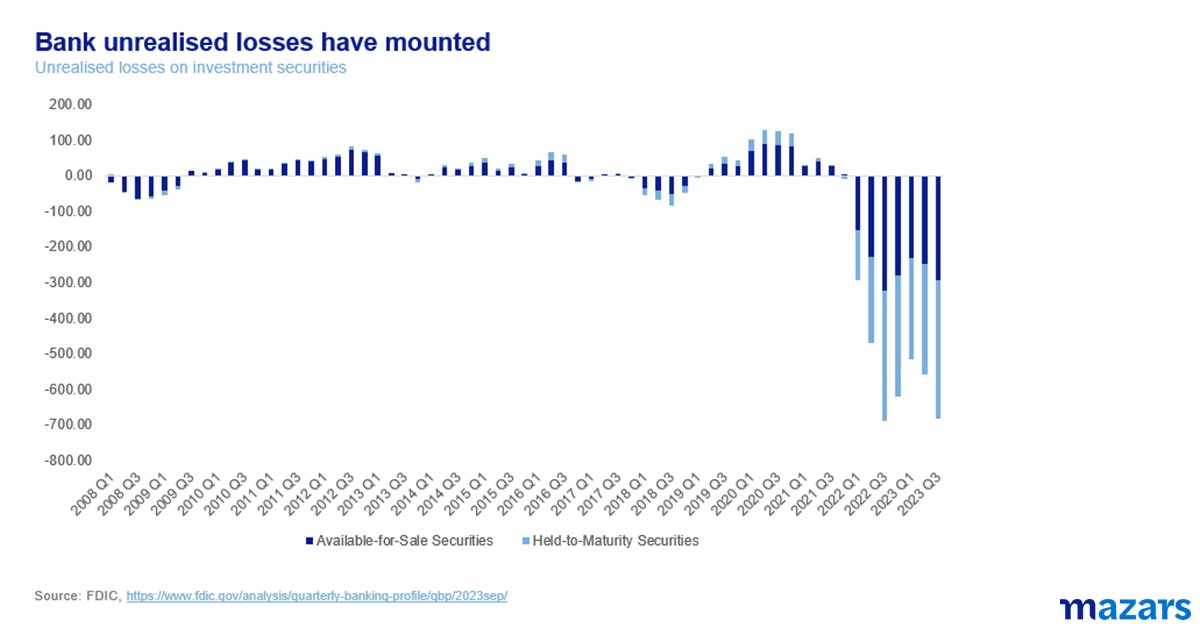

This means that economic conditions will continue to deteriorate for the foreseeable future. Coming out of an era when very-low rates had been assumed to last ad infinitum, it stands to reason that some actors had taken bets on that exact outcome. The combination of an economic slowdown and the abrupt end to the previous regime may uncover unexpected weaknesses in some corners of the market such as commercial real estate, much like it did with US peripheral banks earlier in the year.

What we are talking about is “unknown unknowns”. The question is less about what exact part of the market may be exposed and more about how much damage markets will have to sustain before monetary authorities step in. In 2008, central banks watched as the US subprime housing market crashed, credit froze, and didn’t act immediately even when Lehman collapsed. The lesson was well learned. In 2023, it took one peripheral entity, Silicon Valley Bank, to go under for the Fed to react immediately and print over $300bn. The damage from the former crisis is still with us. The damage from the latter is all but forgotten.

4. Rates will begin to come down in mid/late H2 in the US. Europe will follow.

The rate outlook is murky and data /event-driven. As such, the market’s confidence level in predicting rates is low. At the time of writing (December 2023), US markets are pricing in rate cuts beginning mid-2024. While it is possible, especially if we see a financial accident, our main scenario suggests that rate cuts can’t begin until later in the year. For one, the Fed and the ECB hiked in September in full knowledge that for a hike to take effect it takes nine months to a year. Reversing course earlier makes little sense. Also, while the economy is slowing, there’s little evidence of a deep recession, the kind that would force action sooner rather than later.

Geoeconomic fragmentation considered, we believe that rate-cutting cycles between Europe and the US will not be synchronised. And while European inflation is lower than the US, closer to the 2% mark, EU interest rates at 4.5% aren’t nearly as restrictive as US ones at 5.5%.

So, it makes sense that when the time for cuts is near, the US Federal Reserve will lead the move, with Europe following. In terms of UK rates, despite the economic slowdown, the labour market remains tighter and wage inflation is much higher. We believe that the UK is more likely to ease rates along with Europe, and even after the ECB, rather than with the US, despite the fact that its rate level, at 5.25% is closer to the American one.

5. Quantitative Tightening will end roughly around the time when rate cuts begin. Equity markets will be able to sustain a rally thereafter.

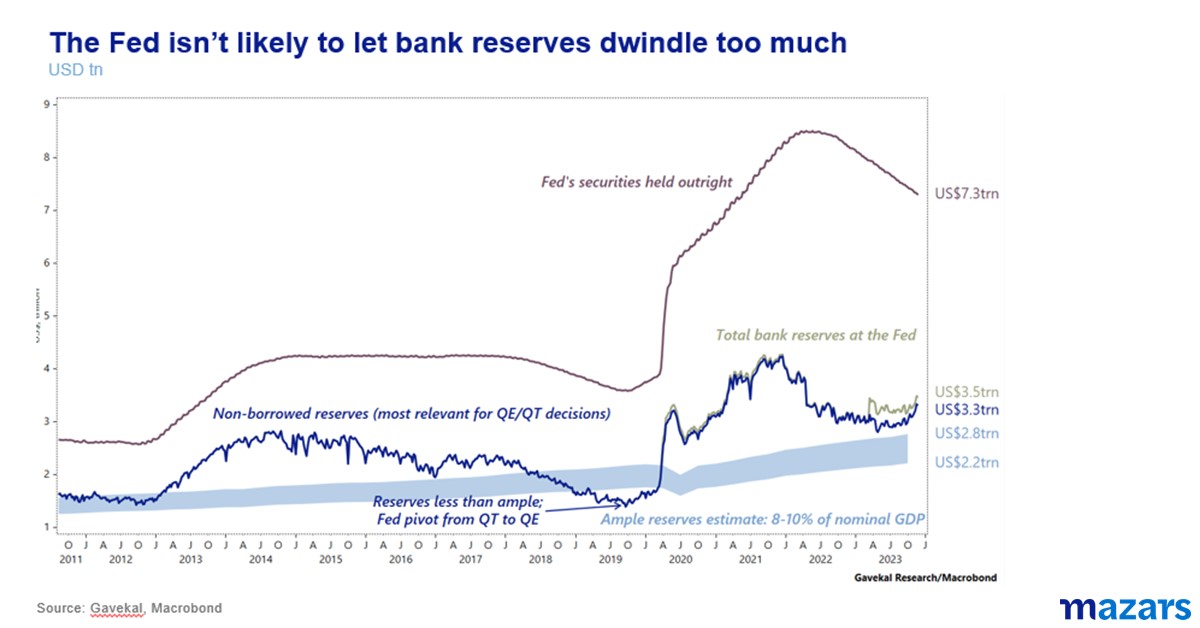

Markets care less about rates and more about Quantitative Tightening. Central banks, which have reduced their balance sheets aggressively in the past year and a half, have been rather silent about discontinuing the practice. Given the high level of rate uncertainty, it is difficult to predict the end of Quantitative Tightening. However, we believe that once rate cuts do happen, they will most probably bring the end of Quantitative Tightening. For one, as Quantitative Tightening persists, the reserves commercial banks hold with the central bank are dwindling. Non-borrowed reserves currently stand at $3.5tn, 500bn above the upper limit of the Fed’s comfort level, which Gavekal estimates to be at 8% to 10% of nominal GDP. However, the more Quantitative Tightening persists, the more those reserves dwindle. Additionally, it makes little sense to reduce commercial rates but to continue tightening monetary conditions in financial markets. The end of Quantitative Tightening should help markets rebound, and possibly even allow a sustainable equity bull market.

6. Short yields to come down, curve to bull steepen

When central banks hike or cut rates, the short end of the curve moves first and faster. When rate cuts begin, we expect that short rates will come down faster than long rates, allowing the yield curve to Bull Steepen (the whole curve comes down, but faster at the shorter end). There’s also a probability of Bear Steepening (the curve moving up faster at the longer end) in case a financial accident forces central banks to cut rates, rather than the economy moving at its present course. Yield curve steepening is necessary for the profitability of financial institutions, credit flow and the ability of pension funds to meet their long-term obligations, and thus it is very desirable by central banks.

We believe this will probably happen naturally. However, even if it doesn’t, the Fed can always choose which bonds it will sell in the open market (longer or shorter-dated) to help achieve its desired outcome, which is the curve steepening.

7. Economies will slow down in H1 and begin to recover in later H2. No deep recession.

The economic slowdown has been well underway since mid-year 2023. However, we believe that, at least in the US and possibly in the UK we won’t see a deep recession. The reason, both countries have been running extended fiscal deficits, exactly to mitigate the worse effects of the slowdown, also ahead of national elections in the next few months. In Europe, the economic situation is tighter and while we don’t expect a sharper slowdown, risks are more elevated. European countries are bound by the Stability Pact, so they can’t run high deficits. In Germany, Europe’s economic locomotive, the decision of the High Court which prevented the government from using Covid-funds as a form of fiscal expansion, exacerbates the economic slowdown, primarily driven by the loss of competitiveness in the auto sector and the high energy costs plaguing the manufacturing industry. And while the ECB hasn’t raised rates as much as the Fed and the BoE, it has reduced its balance sheet by more than $2tn, nearly double the pace of the American Central Bank.

As central banks begin to communicate rate cuts nearer the end of 2024, we expect consumption to pick up, and economic activity to rebound. Manufacturing, which leads economic cycles, has already shown evidence of stabilisation and could begin to recover earlier in the year. The services sector should follow. 2024 and possibly 2025 are still expected to see growth below trend, however, as higher than average inflation and high interest payments eat into real economic output.

8. Inflation to stabilise, bar geopolitical turbulence

Inflation has two components: demand-side and supply-side. Usually, inflation cycles begin with supply-side tensions which then turn into demand (consumer) led pressures. Inflation has become de-anchored from its lows in the previous decade and a half, as the pandemic accelerated de-globalisation and various centrifugal forces. This means that mean-reversion (with the mean around 1% to 2%) to a steady inflation regime remains elusive. Simply put, it’s difficult to see returning to a regime where central banks were trying, and failing, to stoke some inflation. Instead, much like the 1970’s we are looking at inflation in waves. With that in mind, the consensus moves towards a moderate stabilisation at levels around 2.5% to 3.5% in 2024, mostly because consumers are running out of pandemic-related savings and seem unwilling to pay higher prices. However, overall tight employment conditions, China’s economic maturing, geopolitical supply chain shifts and infrastructure investment in the Green Transition and other big projects, as well as a steep yield curve, should keep inflation well above the very low levels we have been accustomed to after 2008. Against this present trend, further geopolitical tensions will threaten to disrupt the course of inflation stabilisation, a course that is far from smooth, and produce yet another wave of price hikes.

9. Consumption to slow down and unemployment to climb, albeit marginally.

In this growth and inflation environment, we expect consumption to slow down in the first half of the year, and begin to recover thereafter, as consumers begin to consider the positive economic effects of rate cuts. Unemployment will continue to climb as the economy slows down, however, it has become evident that poor demographics, the persistent skills gap and low labour participation rates will keep employment conditions tight.

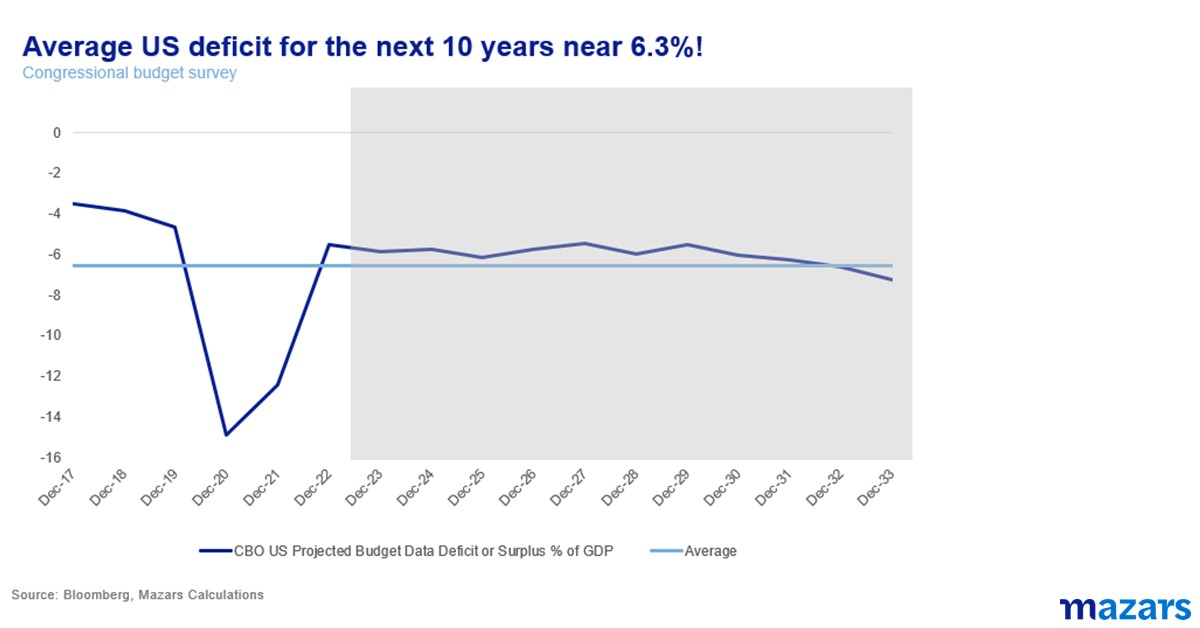

10. Deficits will persist, and debt will continue to climb.

Global debt to GDP is 340%, nearly 120% higher than it was two decades ago. Despite high levels of GDP and interest payments exceeding output growth, many countries have opted to maintain high levels of fiscal spending to mitigate the effects of the economic slowdown. The OECD has already issued a warning that the trend may not be sustainable.

We believe that we are reaching levels where debt is issued to pay for debt, a process that is self-accelerating. Although at some point fiscal restraint is necessary, pushing countries towards primary deficits, the economic slowdown precludes a return to fiscal prudence at least in the next few months. If anything, fiscal easing causes inflation to run higher, reducing the amount of the real debt burden. We think that nominal global debt will continue to climb in 2024, and we are looking for signs of whether the pace is accelerating or decelerating.

11. China will rebound.

Although the scenarios vary, we believe that China will see the smoothing of its real estate market crash and a slow return towards growth normality. Economic growth, much of which is still manufacturing-based, is already somewhat rebounding, which can be corroborated by improving industrial data in Asia and other sources.

Additionally, the government and central bank have been stimulating the economy for the past few months, which should translate into improved consumption in the near future. Having said that, geopolitical fragmentation brings a slow removal of China from the heart of the global supply chain, which should have some significant repercussions in terms of trend growth. This geopolitical shift should cap the economic rebound, somewhat, in 2024, but overall we think the year will be a better one for the world’s biggest manufacturer and second-biggest economy.

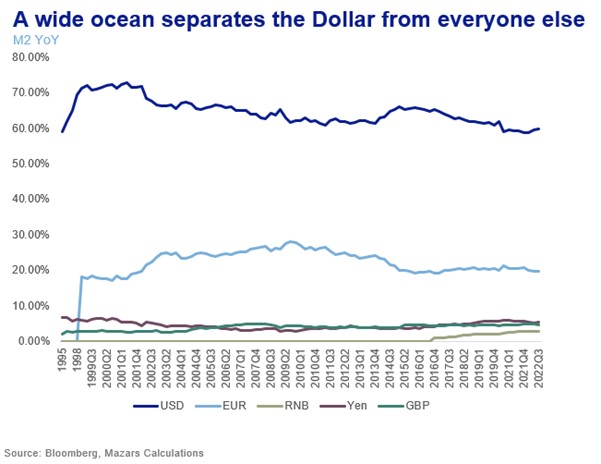

12. The Dollar will remain the world’s reserve currency

Despite efforts to dislodge the US Dollar from its natural perch, at the top of the global currencies food chain, we believe that the Greenback will remain the world’s choice as a global reserve in the next year, and years to come. Despite China amassing gold reserves and some deals in Asia to trade commodities in local currencies, China and other economies still hold huge amounts of Dollar reserves. 58% of all global reserves are in Dollars. Reducing that number abruptly creates a supply problem for all other currencies. Additionally, if the Dollar’s value were to lower due to massive de-dollarisation, then the value of most countries’ reserves would drop dramatically. In behavioural terms, the stability of the Dollar is still deeply ingrained within consumer mentality. Foreign Currency Bond issues are predominantly carried out in US Dollars. Where inflation is very high, like Argentina and Turkey, consumers seek to save Dollars instead of local currency. This has also held true for many currency crises in Asia. While we see the de-dollarisation narrative increasing as a result of high deficits, we believe that lacking a viable competitor, the US dollar will likely remain in vogue for the foreseeable future.

George Lagarias, Chief Economist

*This article was originally featured in the FT Adviser

Register for our upcoming economy webinar

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

December 2023. Consumption is a key component of any modern society. It accounts for over 65% of GDP and is one of the most important indicators for assessing the health of an economy, with fluctuations in consumer confidence being a key indicator for predicting the speed of a recovery or the depth of a recession.

When we talk about risks, by definition we mean events or developments outside our base scenarios. The following risks are not, thus, our prediction of what will likely happen in 2024. Instead, we focus on how certain areas of politics and the economy may develop adversely enough to disrupt the base-case scenario and lead to different outcomes.