The economy & your investments

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

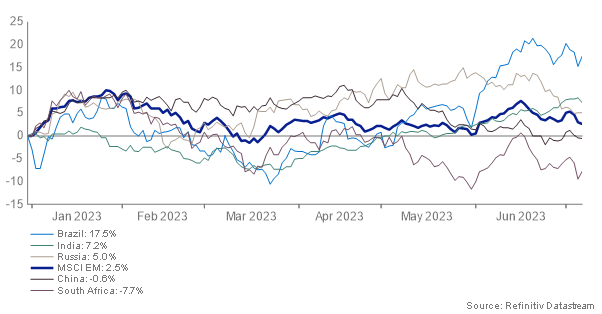

Chinese businesses too were expected to attract increased demand from overseas. Additionally, encouraging economic trends, such as a deceleration in global inflation, meant the MSCI Emerging Markets (EM) Index rose significantly in January. Subsequently, the asset class experienced broad based profit-taking.

After declining in the first half of March 2023 due to concerns over tighter financial conditions and the solvency of US regional banks, a reversal took as fear of contagion began to dissipate and China provided increased support for the internet and gaming sectors.

The story since the first quarter of the year has been somewhat similar. A mixed bag.

One of the main stresses on EM equities was China’s weak reopening. Foreign investors’ expectations were based on the experience of other economies’ pent-up post-pandemic demand. China’s fixed-asset investment, which is an important contributor to growth, grew by only 4% in May 2023, lower than the 2022 average. This is not only true of shrinking real estate investment, manufacturing investment is also growing more slowly than the previous year, when China had a strict countrywide lockdown.

China’s contracting PMI data for May also confirmed the negative sentiment on manufacturing, which should not be surprising given that industrial profits have plummeted in 2023, with close to 20% negative growth in April. Although the poor performance of the manufacturing sector and its divergence versus services is a global problem, China’s case is particularly important because it is the world’s largest exporter its share, more than 20%.

Other EM’s such as South Korea, Asia’s fourth-largest economy, saw its exports fall for the eighth straight month in May due to weaker demand for semiconductors and other related tech equipment. Arguably weaker demand from its largest trading partner, China, has hurt its trade balance the most.

Indonesia’s export and import performance has been very strong. Its economy relies heavily on exporting commodities and it came as no surprise then when Indonesian copper and gold company, Amman Mineral International, did exceptionally well in the country’s biggest public listing in more than a year. The IPO marked a major commodities listing linked to the renewable energy boom in Indonesia. Investors have bet big on materials including copper and nickel — of which Indonesia has in abundance — as the electric vehicle race heats up.

Meanwhile countries such as Vietnam, India and Taiwan have quickly become a vital link in supply chains as business pivot away from China. The accelerating shift to other nearby Asian countries is part of a growing “China plus one” strategy to redraw global supply chains. As rivalries grow between China and the US over technology and security, more companies fear curbs on what and where they can manufacture. As a result, many are supplementing production in China, still the world’s biggest manufacturing hub, with expansion to other countries.

Foreign investment in Vietnam hit decade high last year with Japanese, Singaporean and Chinese companies being the biggest source of said investment into Vietnam.

The brightest spot in the EM’s has been India. India’s GDP growth rate of 7.2% in Q1 2023, surpassed economists’ expectations and confirmed the country’s status as one of the world’s fastest growing economies with an increase in private consumption and services contributing to this.

Indian authorities have courted foreign businesses and investors by presenting the country as a beacon of robust growth amid a global slowdown. Prime Minister Narendra Modi’s first official state visit to the US last month, shaking hands with President Joe Biden and high-profile executives like Tesla Inc.’s Elon Musk, has caught investors’ attention. While India still has a lot of work to do before it can successfully integrate into global supply chains, a favourable geopolitical environment is a key reason why India is boosted by the west’s desperate need for an alternative to China.

All in all, the first half of the 2023 has truly been a mixed bag for EMs. From a macro perspective, headline EM inflation has dropped, but in emerging EMEA and Latin America (excluding Brazil), it remains above central banks' targets. Monetary tightening cycles are at or near the end in most EMs given moderating inflation, weakening growth, and declining long-term U.S. bond yields.

We expect that most EMs will gradually return to their potential growth rates later in 2024 and 2025. But numerous risks could weigh on growth, including slowdowns in the U.S. and Europe, a further setback in China's recovery, sharper global financial tightening, and the Russia-Ukraine conflict dealing another inflationary shock.

Prerna Bhalla, Investment Analyst

On Wednesday 26 July, join our Chief Economist and Chief Investment Officer as they discuss the current economic landscape, both here in the UK and globally.

Join our Chief Economist and Chief Investment Officer as they discuss the global economy, inflation, interest rates, and the investment landscape.

“What if I could tailor my investments to my needs?”

Read our latest news and analysis on the changing markets and economic environment.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.