Privately Owned Business newsletter - Dec 2021

Until mid-November the view seemed to be developing that whilst Covid-19 would continue to be an endemic problem, vaccination programs were moving it into the ‘manageable’ box.

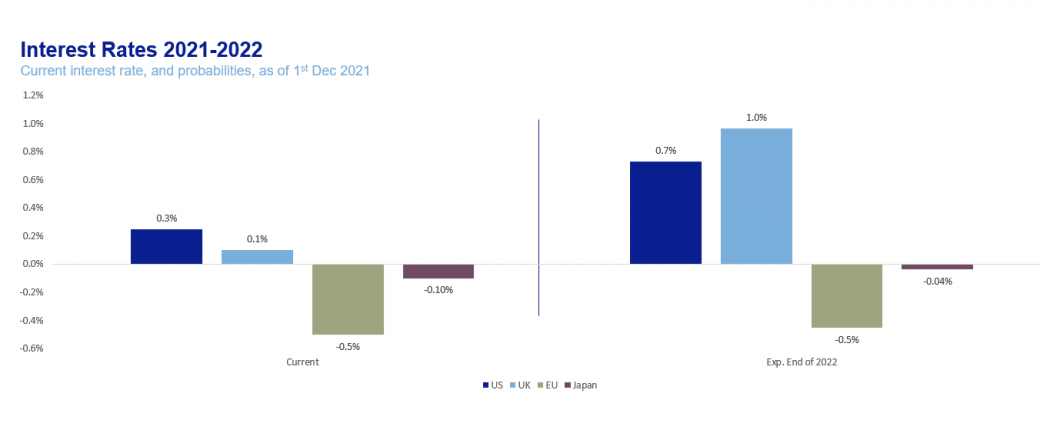

What is the outlook on UK interest rates?

Then, in November, it surprised again, by keeping interest rates stable, with a large majority 7-2. The reason why the British central bank chose to be hawkish, almost a year ahead of its peers in the US and Europe is unclear. The reasons why it backtracked, even more so. What we do know, however, is that we have entered a period of higher rates, and more rate uncertainty.

Currently, markets are pricing in around four 0.25% interest rate hikes until the end of 2022. If it holds true, it will be the steepest (and in essence the first) rate hike cycle in nearly sixteen years. However, we think that there’s an increasing probability that the final rate will be lower than the projected 1%.

The Omicron variant already poses a significant risk to the economy and could force the MPC, the Bank’s rate-setting body to rethink. Also, we believe that the Bank may have wanted to use “hawkish” language on rate to curb inflation expectations and thus constrain wages, rather than actually wanting to raise the cost of money for consumers.

We feel that the move to hike rates may be slightly premature. The UK would be hiking around six months ahead of the US and possibly a year ahead of the EU. Given that the bulk of inflation comes from external supply-side pressures, including labour supply shortages, rising interest rates would do little to curb it. Overall, consumption should be impacted adversely, albeilt marginally, because the impact on homeowners will be spread out over a period of twelve to eighteen months. Overall, rates of 1% in and by themselves will not present a great challenge. But if one adds inflation and higher taxes, following the budget, we see higher rates as further exacerbating consumer sentiment and propensity to buy.

There is likely going to be a measurable impact on consumers, especially homeowners with a mortgage. The impact will be spread out, because 80% of all mortgages in the UK are fixed-rate. However, the bulk are refinanced every two to five years, so within the space of twelve months, possibly 35%-40% of mortgage holders will face the effect of higher rates. Lower consumption might have an impact on the top line (revenue) earnings of businesses, and could further suppress margins.

Conversely, the banking sector, which borrows over the short term and lends over the longer term, should benefit from rising rates.

In terms of bigger investments in the UK, higher rates ahead of the rest of the world would put upward pressure on the Pound. Institutional investors could become more apprehensive and choose other markets where rates are more predictable, and currency will be lower. This could impact support for Sterling assets, stocks, bonds and cash holdings. Having said that, the impact will be marginal. We don’t believe international investors will give up on the UK after this. The country’s track record and G7-economy-status will probably redeem decision-makers in Threadneedle St.

People and businesses which just refinanced for a period of five years should see the least impact in terms of debt. Also, sectors where financing terms are fixed in general. Companies that have lower leverage (debt), like tech, should see only pressure from an earnings perspective, not interest payments. Consumer staples, healthcare, utilities and generally sectors where demand is stable.

Most debt facilities will include a fixed margin alongside a variable element linked to the central base rate. If this base rate increases, so will debt service costs impacting cash headroom and covenant compliance. The first step for corporates and privately owned businesses is to understand the impact of potential increased central rates on your debt service costs and consequently facility headroom.

If facilities are nearing their term, it is worth assessing whether current facilities are fit for purpose and whether an alternative structure or a new provider, will more appropriately satisfy short term and long term funding requirements, as well as locking in better pricing to offset any future interest rate increases.

A 0.25% - 1.00% increase in isolation may be comfortably managed by most businesses, however, it is also important to understand the reasons for the potentially increased rates. As mentioned earlier, a potential interest hike is a consequence of inflationary pressures including supply chains, which has impacted numerous industries. Supply delays, increased shipping costs and staff resources, are all significant issues currently affecting businesses.

The combination of higher debt service costs, supply chain pressures, as well as likely future increases in taxes and repayment of HMRC arrears, means that having the right debt structure and funding partner to support the long term sustainability is integral to continue to trade, grow or exploit new opportunities.

It is important for business owners to spend time forecasting the key factors affecting their business to appraise the impact on cash, availability of facilities and covenant compliance. Having an integrated long term financial forecast will allow businesses to quickly assess the potential impact of the cluster of factors affecting businesses since the start of Covid-19.

There has been a flood of new lenders to the market in recent years aiming to address the previous gap between high street banks and equity providers, which has ultimately given businesses more choice in finding a funding solution that works specifically for them.

Taking the time to scenario plan and improving forward-looking visibility of potential impacts from interest increases, continued supply chain pressures, accelerated growth and several other factors will allow businesses to have productive discussions with lenders. Most importantly, it will assist in having earlier conversations (before it may be too late to negotiate better terms or a more suitable debt structure).

Finally, it is also worth highlighting that the external factors discussed above can lead to opportunities for stable and cash generative / cash-rich entities. Increased rates can benefit those with significant reserves, and also funding difficulties experienced by others can unlock acquisition opportunities for those with surplus cash to gain market share and eliminate competition.

Our Debt Advisory, as part of a global deals practice, can assist with assessing existing debt facilities, helping to appraise the potential impacts of external factors such as interest rises and supply pressures and help to find an appropriate funding solution for you and the future success of your business.

Our global deals practice provides advice to large groups, privately owned businesses, entrepreneurs and investors on acquiring and selling businesses, raising funds and restructuring debt. Our teams have vast experience across a range of sectors and deal sizes. Our fully integrated, the international team allows us to mobilise project teams with unique and specific experience to make your project a success. And with a presence in over 90 countries and territories worldwide, our corporate finance experts can help you connect with targets, acquirers and financial sponsors from across the globe.

If you’d like to get in touch, please use the form below.

Until mid-November the view seemed to be developing that whilst Covid-19 would continue to be an endemic problem, vaccination programs were moving it into the ‘manageable’ box.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.