National contact

Belgium recently introduced a tax relief for inbound expatriates that exempts 30% of their earnings from tax for the first 5 years they are resident there (see Belgium - 30% ruling for further details). The Belgians are the latest in a long line of countries that have introduced personal tax concessions that are designed to attract workers and investment to their country.

The UK also has legislation that when applied can alleviate the tax burden on inbound expatriates, known as overseas workday relief (OWR). However, the rules surrounding this relief are complex and expatriates wishing to claim under the scheme need to carefully manage their finances if they are not going to be open to a challenge from HMRC.

At a time when the UK government is looking to encourage investment and promote a high wage economy, the administrative hurdles created by the relief can counterintuitively result in the UK losing out on global talent and investment to other countries with more simplified expatriate tax regimes.

Bearing this in mind, in November 2021 HMRC consulted expatriate tax practitioners on the case for reform of this relief.

In this article we look at:-

OWR (see RDR4 OWR) is broadly available to non-UK national employees who come to work in the UK. Provided that certain conditions are met, the employee is only subject to UK income tax on their employment income related to their UK workdays.

The portion of their employment income related to their non-UK workdays falls outside the scope of UK tax provided that this part of their income is not remitted (transferred) to the UK. The relief is available for the tax year of arrival and the next two full tax years.

It is the question of determining the amount of earnings that have been remitted to the UK that makes this relief so difficult to manage, and this is often chosen as the area for enquiry by HMRC.

To calculate the income that has been brought into the UK compared to the income that has remained offshore, the legislation contains a complicated set of rules known as the “mixed fund rules”. These can be onerous to comply with as they require a line by line analysis of every single transaction made from a bank account where funds have been transferred to the UK.

Given that employees are likely to make hundreds of transfers out of their bank account each tax year, determining the taxable remitted funds can create a massive headache for both advisers and HMRC.

These complexities can be alleviated where employees set up a separate qualifying bank account specifically to manage their remittances to the UK. This is known as a special mixed fund (SMF – ITA 2007 s809RA-s809RD).

Where the conditions of the SMF rules are met, the employee’s taxable earnings are calculated on an annual basis rather than on a transaction by transaction basis. A comparison needs to be made of the total remittances to the UK from their qualifying offshore bank account in each UK tax year, against the portion of their earnings related to their UK workdays.

If these remittances are equal to or less than their earnings related to their UK workdays, then the employee is only taxed on these earnings and the earnings for non-UK workdays remain exempt from UK tax.

However, implementing this “simplified” bank account/remittance planning is still a challenge for the expatriate as the following conditions must all be met to apply the SMF rules:-

So, whilst OWR is an attractive option, the administration and conditions to qualify for the relief can:-

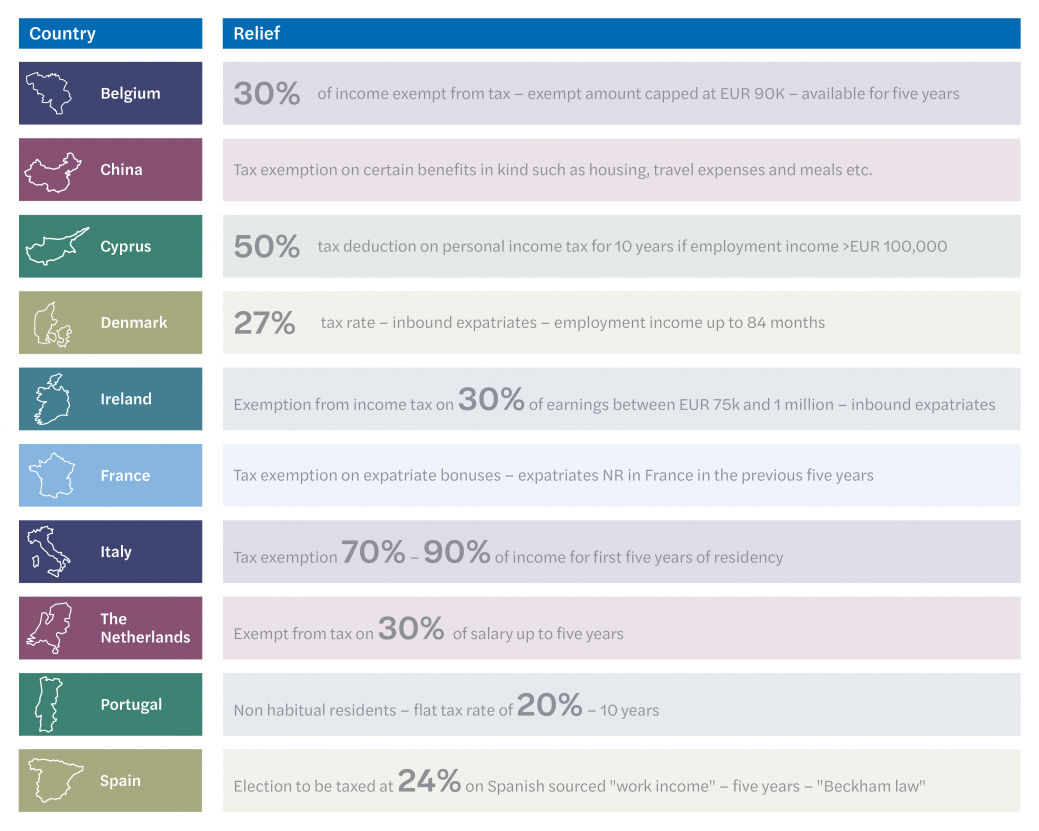

The following shows a selection of the expatriate tax regimes available from a variety of countries.

Unlike OWR, these tax reliefs generally do not require employees to keep part of their earnings offshore, i.e. in most cases, the employee can remit the funds to their country of residence without incurring a tax charge on these earnings.

HMRC are looking at a range of ideas that can broadly be distilled down to the 4 options below:

Options one and two would simplify the position, and option one would place non-domiciled expatriate employees on the same footing as a UK domiciled employee.

Additionally, this could be welcomed by an electorate that is becoming increasingly troubled by tax avoidance and expects tax fairness. It would also avoid the technological investment required by HMRC to digitalise OWR as part of its Making Tax Digital ambitions.

However, this could result in UK businesses losing out on attracting both global talent and investment, or having to increase these employees’ reward packages to compete with businesses situated in countries that do provide attractive expatriate tax reliefs.

The third option would be the most attractive for UK businesses (help them attract global talent) and should be simple to legislate for. However, the government would need to weigh up the cost of a loss of tax revenue (from increased OWR claims), vs the potential economic gains from inward investment into the UK and these employees spending these remitted funds in the UK.

The fourth option would have similar advantages and drawbacks to option three but has the added disadvantage that the legislation would need a significant rewrite.

Both options three and four would require significant investment by HMRC were it to digitalise OWR. Identifying, designing and implementing technology to identify and track remittances is likely to take some time to come to fruition. Additionally, this would require increased global information-sharing agreements and is complicated by the increasing use of cryptocurrencies.

OWR is complicated to administer and significant amounts of time are invested by businesses, tax professionals and employees to comply with the rules.

Making an amendment to the legislation that does not require employees to keep their earnings related to their non-UK workdays offshore to obtain OWR would be a welcome simplification, but is likely to result in increased claims and may therefore be politically unpopular.

It would however help the UK remain competitive compared to other countries that offer expatriate tax reliefs, and the economic benefits created from increased inward investment and employees spending their remitted funds in the UK could outweigh the costs to the exchequer of increased OWR claims.

For further information please get in touch with a member of the Mazars UK global mobility team.

In a fast paced, globally connected and competitive world, businesses need to make the most of all the assets at their fingertips in order to remain resilient and thrive.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.