National contact

Why investors putting trust and funding into admin

It’s fair to say that LivingBridge (then known as ISIS) backed MBO of Equiom (then known as Anglo Irish Trust) sparked a deluge of interest and investment into the sector. It also started a trend of renaming and rebranding that has continued at such a pace that I frequently have to suffix my description of a company with “the business formerly known as…”.

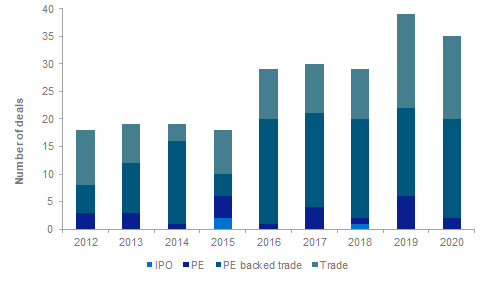

In 2006 I don’t think anyone would have predicted the level of activity that would still be going on in the sector in 2020, but as the chart below shows, there has been strong and continuous growth in M&A over the last eight years with 2019 being the most active year on record. This has been driven by PE investment in the sector and also continued consolidation as we move towards a “Big 4” or “Magic Circle” like model of major global players, similar to that seen in the accountancy and legal professions:

The question is, what is driving this continued activity and interest? Well, there are a number of factors at play:

The success of the listed players has created an extremely attractive exit route for larger Private Equity investors and has also created demand for acquisitions of smaller, independent players, creating capital appreciation opportunities throughout the value chain and size range in the sector; and

Even as we continue to move towards a market structure dominated by a small number of global players, there continues to be a market opportunity for smaller, independent specialists who can focus on a specific niche and develop a more dynamic, entrepreneurial offering which then becomes attractive to the larger players when it reaches sufficient scale. This clearly creates ongoing M&A activity and appetite for PE to continue to invest, helping smaller, owner-managed businesses grow and develop into attractive acquisition targets.

In 2010 I couldn’t see how the market could continue to be as active as it had been – now I can’t see how it won’t continue to be for the foreseeable future.

Sources: CapitalIQ, MergerMarket, Pitchbook, Company Websites and Mazars Intel

If you would like to speak to a member of our M&A team, please click button below to arrange a call.

Mazars Deal Advisory - 2020 review and outlook for 2021

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.