Want to know more?

Indeed, unlike the derivatives market, there is no harmonised fallback language reform for loan products across the industry, and different solutions have been proposed by the Loan Market Association (LMA) and by the Alternative Reference Rates Committee (ARRC). Further complexity is added to the transition away from IBOR for loan products as they will need to be renegotiated on a bilateral basis. This is because a similar agreement to ISDA’s protocol which enables a multilateral amendment of derivative contracts does not exist for loan products. As a result, the IBOR transition related to loan products seems more likely to incur economically undesirable outcomes including legal, conduct and operational risk.

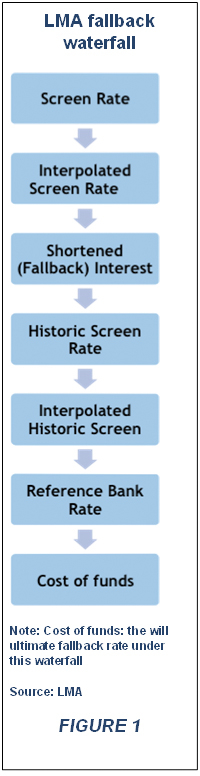

Loan contracts that are governed by the LMA across Europe, Middle East and Africa, are still subject to the historic fallback language waterfall. LMA has not implemented an IBOR fallback language reform yet, thus letting loan contracts fall back to the cost of funds rate[1] (i.e. the rate at which banks fund their assets) in the event of LIBOR discontinuing. This generates significant challenges both for lenders and borrowers. In particular, banks have no interest in disclosing their own cost of funds as it would give information on their credit quality, which might spiral into speculative actions regarding default.

Before even disclosing the cost of funds rate, defining this rate is already a challenge. Loan agreements under LMA give lenders the flexibility to use any funding source, essentially letting them define the new fallback rate. That flexibility is further enhanced by the absence of a dispute resolution mechanism in case a borrower questions the calculation of the rate. For syndicated loans, the situation becomes even more complex as the facility agent would have to get a cost of funds rate from all lenders within the syndicate, having to chase each one and interpret each different calculation method. Due to the reputational risk and increased complexity for lenders and non-transparency for borrowers, the cost of funds rate fosters uncertainty and exacerbates the likelihood of incurring losses for both parties alike.

The cost of funds rate alternative was never intended to be a long-term solution. As such, LMA recently published an exposure draft of a Reference Rate Selection Agreement guiding market participants on how to fallback from LIBOR to Alternative Risk-Free Rates. However, as this is not yet considered a recommended form of the LMA[2], new LIBOR-referenced loan contracts are still subject to the historic waterfall. Alternatively, market participants can follow national working groups’ (such as ARRC or ECB) recommendations on IBOR fallback language for cash products.

Published in 2019, the ARRC’s language appears to meet the criteria for a robust fallback language[3]. The working group has focused on suggesting solutions that will be sustainable in the long term, including fallback triggers that capture a permanent cessation of the benchmark, a waterfall incentivising the use of Alternative Reference Rates and the inclusion of a spread adjustment. The fallback triggers reflect three phases:

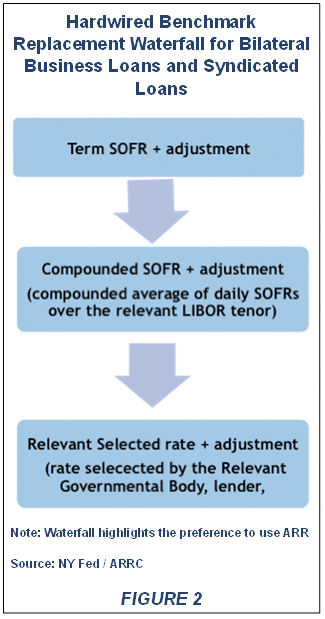

In addition, ARRC has proposed two sets of fallback language waterfalls, the hardwired and the amendment approach. The hardwired (Figure 2) is broadly consistent across securities (with only slight differences) while the amendment approach provides flexibility for reforming bilateral business loans and syndicated loans. While this approach is useful at the current stage of the transition, ARRC indicates that such an approach may become inefficient to use for institutions planning to amend significant volumes of contracts when LIBOR permanently ceases to exist.

ECB’s working group has also published fallback language for euro-denominated cash products (i.e. referencing EURIBOR or EONIA) under principles similar to those described above. These principles should be adopted throughout the loans market as they pave the way for a smooth IBOR transition. A strong fallback language significantly reduces conduct and litigation risk through clearly defined triggers and a robust waterfall.

Although “best” principles have been published and made available to market participants, no significant progress on the IBOR transition of loan contracts has been observed. Some market participants seem to be waiting for a market-wide mechanism similar to the ISDA protocol to emerge. Given the bespoke and “tailor-made” nature of some loan contracts and the legal barriers across the various jurisdiction, such a solution may prove to be challenging to adopt. The solutions proposed are somehow imperfect either because they are short-term solutions (LMA’s current fallback language) or, on the contrary, long-term solutions whose feasibility depends on technical issues to be solved (Term SOFR not developed yet). In the meantime, market participants can only do so much with their legacy loan portfolio as they wait for the final solutions to be formally adopted.

[1] https://www.lma.eu.com/application/files/3815/3855/5150/ACT_and_LMA_LIBOR_Guide.pdf

[2] https://www.lma.eu.com/news-publications/press-releases?id=173

[3] https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2019/LIBOR_Fallback_Language_Summary

26 March 2020

Paving the way for transition towards an IBOR-free world.

The latest IBOR related insights and analysis

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.