Want to know more?

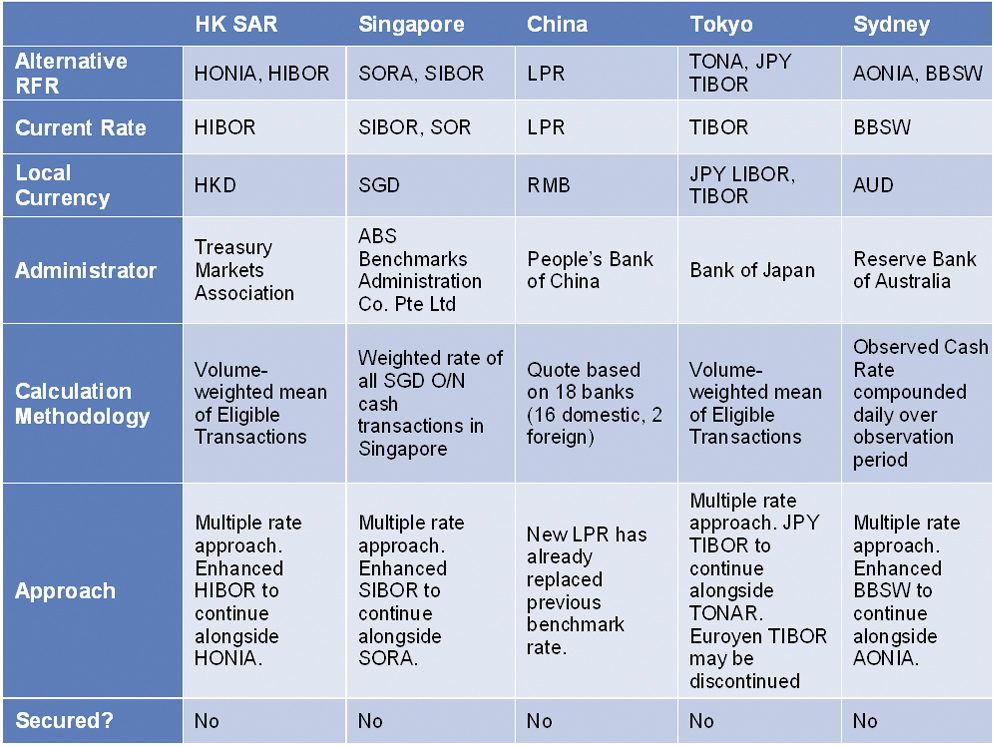

Replacement rates have been chosen but, similar to corresponding markets, are facing challenges as the IBOR cessation date nears. Asia’s major replacement rates are to be the Hong Kong HONIA and HIBOR, the Singaporean SORA and SIBOR, the Chinese LPR, the Japanese TONA and JPY TIBOR, and the Australian AONIA.[1] Unlike the Euro Area and the U.S., Asia’s leading economies have mostly adopted multiple rate approaches, in which they have implemented new RFRs alongside strengthened existent credit-based benchmarks.

Unlike the Euro Area, Asia is not subject to regulation similar to the benchmark regulation (BMR), so most RFRs are set by local central banks. This means RFR implementation across Asia has been more fragmented than what we’re seeing across the European market.[2] Overall, the Asian market has approached IBOR transition at multiple speeds, with multiple approaches. Asia’s leading financial centres which transact heavily on the global markets and support a large number of foreign investors, such as Hong Kong and Tokyo, are moving to keep pace with European and U.S. markets. However, emerging Asian economies which boast more regional clientele are falling behind, notably due to a lack of guidance, modelling experience, and legal expertise available to support transition plans.

Asia will be as affected as Europe and the U.S. once Libor is phased out, if not more so. Asia’s more developed markets will therefore need to watch their own markets and reference rates, as well as correlated international exposures from the U.S. and Europe. Asia’s emerging markets, many of which have pegged large portfolios to U.S. or European rates, will be hit hard should their central banks fail to consider adequate Libor fallback provisions.

Here are the latest developments related to Asia’s IBOR reform:

The good news for international investors is that Hong Kong’s regulators have sought third-country regulatory equivalence from European benchmark regulators to incorporate both their HONIA RFR and enhance their existing HIBOR rate.[3] The HIBOR equivalence rate is expected to continue with enhanced provisions for both the CNH (Chinese offshore RMB) and CNY (RMB) HIBOR alongside the HONIA. Hong Kong’s regulators achieving equivalence would mean receiving a similar outcome to states in the Euro Area, a boon for European-denominated counterparts of HIBOR and or HONIA users.

Yet challenges do remain. At the time of writing, HONIA OIS curve is not yet existent and HONIA lacks a term structure and sufficiently robust underlying transaction data.. Results from Hong Kong’s most recent May 2019 Consultation continue to be under consideration by regulators, and HK’s Treasury Markets Association (TMA) has shown to be serious about efficiently overcoming HONIA’s weaknesses. Fortunately, Hong Kong’s elected multiple rate approach should sufficiently support market transaction volumes, and we believe that for this reason HIBOR is unlikely to be phased out. However, allowing HIBOR to remain in play also means market participants will have little incentive to actively shift toward the HONIA.

Singapore is actively phasing out its SOR rate as it introduces the SORA as its new RFR benchmark. We expect Singapore to also adopt a multiple rate approach.[4] So far, Singapore has implemented a two-step approach toward RFR implementation. First, Singapore has enhanced SIBOR benchmark, and second, regulators have introduced the SORA for long-term market implementation.

If anything, SOR is most likely to be phased out. SOR is pegged to USD Libor, so, as the U.S. discontinues USD Libor’s publication, SOR will lack the data for its own publication. That being said, Singaporean regulators are also conducting consultations into keeping the SOR by combining SOFR, FX Forward market trades and credit spread along with a new term structure.[5]

At present, SORA is in relatively good standing. It is already transaction-backed and underpinned by a relatively liquid overnight funding market. Published since 2005, sufficient historical data is already existent, allowing for relative ease in relation to developing appropriate pricing and risk mitigation plans. While the SORA market still requires further deepening, generally speaking, Singapore sits in a favourable position. Further SORA consultations are expected to kick off in the first half of 2020, with enhanced SIBOR reform also expected for 2020.

China has recently implemented a new loan prime rate (LPR) as it seeks interest rate liberalisation, allowing market forces greater influence over its benchmark.[6] China’s new rate reforms are aimed at lowering borrowing costs as its domestic economy continues to slow.

The LPR was originally introduced in 2013 as an interest rate setting for China’s commercial banks. However, the LPR has faced controversy as market participants have complained the rate does not reflect market dynamics as much as it should. The new, modified LPR is instead linked to the People’s Bank of China’s (PBoC’s) medium-term lending facility (MLF). The PBoC introduced the MLF in 2014 as a lending facility of longer-maturity funds of typically three months to a year to Chinese banks, with the express intention of allowing the MLF to be a mechanism to inject liquidity into its economy.[7] The MLF has proven to be especially useful of late as the economy has slowed. As the MLF rate is determined by broader commercial bank demand for central bank lending, theoretically, PBoC regulators setting the LPR higher than the MLF rate should give borrowers access to rates which better reflect market fundamentals.

While China is changing its benchmark at an auspicious time, these benchmark reforms are unlikely to be fuelled by Libor cessation concerns in neighbouring economies. More likely, China’s new LPR is a direct product of domestic economic concerns. For this reason, we believe this development is linked to cyclical monetary policy.

Japan has also opted for a multiple-rate approach aimed at replacing and enhancing its current Libor-linked benchmarks. Currently, the Japanese system supports the JBA Tibor (Euroyen) and the JPY Tibor. As the JBA Tibor has links to Euribor, we expect it to be completely phased out upon the Libor cessation date. However, we expect the JPY Tibor to receive further enhancement and continue to be published past the end of 2021. Additionally, we know the Bank of Japan (BoJ) is expected to implement the TONA as its new RFR.

In the short term, JPY Tibor will continue to be the predominant benchmark. However, as calculation methods and market liquidity improve, we expect the BoJ to implement a longer-term approach to create a robust term structure for the TONA, which will allow it to stand as a strong benchmark in its own right based on futures and overnight index swap transactions.

However, significant hurdles remain. Notably, TONA futures trading is currently suspended, eliminating a possible data source for TONA term structure development.

Australia’s central bank is also expected to adopt a multiple-rate approach. Australia’s current rate, the Bank Bill Swap Rate (BBSW), is to be strengthened and co-exist alongside the AONIA, Australia’s new RFR. Australia is a prime candidate for Libor transition: both of its rates are currently supported by deep underlying markets and robust transaction data.[8] While the BBSW will continue to exist, we believe the extent to which it will be utilised post-Libor cessation hinges on how global markets utilising products such as cross-currency basis swaps will transition away from Libor.

A lack of centralised consensus and uniform regulatory measures amongst Asian regulators has left Asia’s emerging economies in the cold. We find these developments concerning, given these markets are likely to be the most unprepared and hardest hit by Libor’s cessation. Additionally, the USD significantly influences Asian markets, so stakeholders in the region would be wise to keep apprised of SOFR developments in the coming months and years.

Progress has been uneven and far slower than leading jurisdictions, with many local RFR approaches still to be settled on, let alone for there to be strategies in place for actual RFR implementation. For example, Malaysian authorities have yet to settle on a new rate, while the Philippines have completed an early round of reform consultations. Overall consensus for Asia’s emerging markets is that IBOR transition consultations have either yet to begin or are in their infancy.[9]

Overall, Asia’s IBOR transition remains quite challenging, not to say a concern. At best, it has been regionally fragmented. Asia’s leading jurisdictions have made significant progress and will plausibly have feasible fallbacks in place by Libor’s cessation in 2021. Asia’s emerging markets, on the other hand, seemingly have a long way to go. Significant challenges remain, and Asia will be an interesting space for major developments as cessation nears.

“Progress towards IBOR reform in Asia Pacific has more recently been on a “wait-and-see” approach and at various speed levels. Although local banks are aware of IBOR reform, a number have not yet conducted an impact assessment. U.S. and EU banks based in the region show greater progress, due to IBOR implementation being centralised in jurisdictions where the reform is under higher scrutiny by regulators. Undeniably, banks, regulators and industry bodies need to accelerate the transition to RFR, particularly because the Asian market is fragmented with different calculation methodologies, different timelines and levels of dependency between jurisdictions. Bank boards of directors in Asia Pacific should establish a robust governance project and conduct a comprehensive impact assessment as soon as possible to design an informed strategy for implementation. Acting now will enable to improve the mitigation of risks related to the transition and avoid higher implementation costs due to a squeezed timeline.”

[1] https://www.bis.org/publ/qtrpdf/r_qt1903e.htm

[2] https://www.bloomberg.com/professional/blog/end-ibor-asia-take/

[3] https://www.risk.net/derivatives/6807521/hong-kong-seeks-european-equivalence-for-hibor-and-honia

[5] https://www.bloomberg.com/professional/blog/sofr-impact-asia-getting-know-new-benchmark/

[6] https://www.icbc.com.cn/ICBC/EN/FinancialInformation/RMBDepositLoanRate/RMBLoanPrimeRate/

[8] https://www.rba.gov.au/mkt-operations/resources/interest-rate-benchmark-reform.html

[9] https://www.risk.net/derivatives/6691926/banks-quiet-on-libor-legacy-transition-say-asian-clients

Article written by Sophia Chiang and Pauline Pélissier.

17 December 2019

Paving the way for transition towards an IBOR-free world.

The latest IBOR related insights and analysis

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.