Key Contacts

Whilst there are clear challenges ahead, a major positive is that the debt landscape is different than in 2008. There is an environment that encourages continued lending (e.g. record low interest rates, government schemes to support lenders) and there are several alternative options available to borrowers that did not exist before including challenger banks, alternative asset-based lenders, debt funds with committed capital, family offices and specialist finance providers.

As a Deal Advisory team, we are speaking regularly with our bank and debt funder contacts to understand the situation and challenges they face, and how they are trying to support businesses. The message has actually been fairly consistent across the board with some of the key themes being as per the follows. However, there are subtle differences between each lender, especially when it comes to interpretation of some of the rules of the Coronavirus Business Interruption Loan Scheme (CBILs).

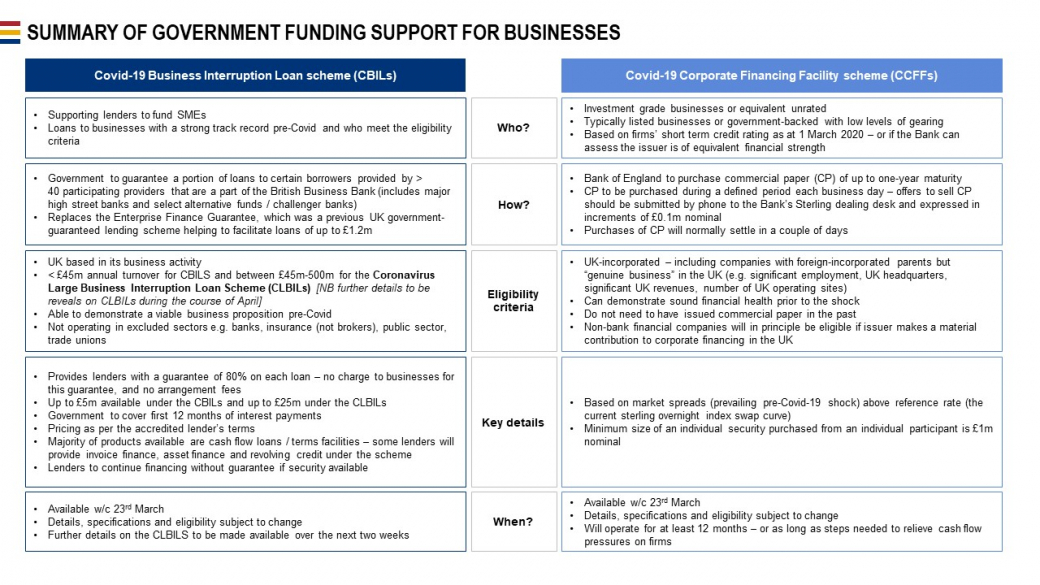

The government has introduced the below schemes to help business funding:

A comparison between these schemes is detailed below.

If you would like to know more about your loan scheme options, please get in touch with us here and Josh, Paul or a member of the team will be in touch.

Cash Flow Management is essential during this pandemic. Mazars will share advice, guidance and practical support from our business experts to help you understand what help is available and how you can access this.

Expert advice throughout the life cycle of the deal

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.