Economically, the purpose of these negotiations is clear: they are largely arranged for the purpose of alleviating lessee cashflow pressures in the current time. However, the accounting for these changes to lease contracts has been less clear under both IFRS 16 Leases (“IFRS 16”) and FRS 102 The Financial Reporting Standard Applicable in the UK and Republic of Ireland (“FRS 102”), with questions arising as to whether a change in lease payments should be accounted for as a lease modification under IFRS 16, or how the change should be accounted for under FRS 102 given that the standard was silent in this area.

Reporting under IFRS

A lease modification under IFRS 16 that does not increase the scope of the lease (i.e. does not change the asset being leased) is treated as a modification to the existing lease, which would inter alia require the lease liability to be remeasured by discounting the revised lease payments using a revised discount rate.

This would generally not cause concern in a normal operating environment where lease modifications are rare. However, this assessment and, in particular, determining a revised (current) discount rate in the current environment, becomes particularly challenging when considering the large volume of lease contracts that may be involved.

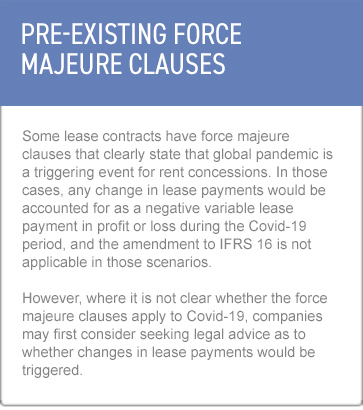

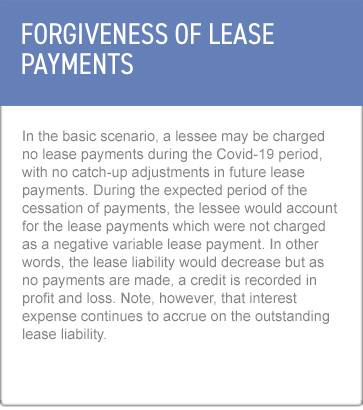

In response to the concerns raised by lessees and other stakeholders, the International Accounting Standards Board (“IASB”) first issued some educational material to assist with understanding IFRS 16, and secondly issued an amendment to IFRS 16 (May 2020) to provide an optional relief to lessees from assessing whether Covid-19-related rent concessions are lease modifications. The amendment, when applied, results in the impact of rent concessions being recognised in profit or loss for the period, with no impact on the right-of-use asset, therefore simplifying the accounting.

Alternatively, if a change were to be accounted for as a lease modification, this would: (a) involve a complex assessment of whether the changes amend the contractual terms of the lease; and (b) result in the impact of the rent concession being accounted for over the remainder of the lease term by adjusting the lease liability, taking account of the revised lease payments discounted at an appropriate rate at the contract revision date, with a corresponding adjustment to the right-of-use asset.

The exemption applies to rent concessions that occur as a direct result of Covid-19 and meet all the following conditions:

- the revised lease payments are substantially the same as, or less than the lease payments applicable before the amendment;

- any reduction in lease payments affects only payments originally due on or before 30 June 2021[1]; and

- there are no substantive changes to other terms and conditions.

[1] In March 2021, the IASB issued an amendment to extend this application period by one year to 30 June 2022. For further details, please refer to our Mind the GAAP blog.

Other key points to remember are:

- the relief only applies to lessees, not lessors, thus lessors are still required to assess whether each rent concession granted to a lessee is a lease modification; and

- the relief must be applied consistently to lease contracts with similar characteristics and in similar circumstances.

Effective date of the IFRS 16 amendment

The original amendment applies to accounting periods beginning on or after 1 June 2020, with the option of early application. The amendment was endorsed by the EU on 9 October 2020. The practical expedient is applicable retrospectively, without restatement of the comparative figures (i.e. impact in the opening equity of the first year of application).

The March 2021 amendment is effective for accounting periods beginning on or after 1 April 2021, with early application permitted.

What does the IFRS 16 relief mean:

Reporting under FRS 102

The Financial Reporting Council (“FRC”) has also issued an amendment for how to account for rent concessions arising as a direct consequence of Covid-19. The amendment inserts explicit requirements into FRS 102 to ensure that FRS 102 reporters account for the impact of temporary rent concessions on a consistent basis and hence prevent any potential divergence in practice.

FRS 102 contains similar conditions, as to IFRS16, for the relief to apply:

- the change in lease payments must result in revised consideration for the lease that is less than the consideration for the lease immediately preceding the change;

- any reduction in lease payments must affect only payments originally due on or before 30 June 2021[2]; and

- there are no significant changes to other terms and conditions of the lease.

[2] In June 2021, the FRC issued amendments to extend the application period of the accounting requirements by one year to 30 June 2022. For further details, please refer to our Mind the GAAP Blog.

However, there are some key differences to the IFRS amendment. Firstly, the FRS 102 amendment is available to both lessees and lessors, so beneficial to both parties within a lease arrangement. Secondly, the FRS 102 amendment is mandatory, whereas the IFRS 16 amendment is optional. Thirdly, due to the fact that the accounting for lease arrangements is fundamentally different under IFRS compared to FRS 102, the accounting requirements are, not unsurprisingly, also different (yet simpler).

The amendments require entities to recognise changes in operating lease payments (for lessees), or income (for lessors), within profit or loss that arise from Covid-19-related rent concessions on a systematic basis over the periods that the change in lease payments is intended to compensate i.e. where there has been a temporary reduction in the lessee’s benefit from the use of the leased asset. This means that the treatment should reflect the economic substance of the benefit of these concessions and their temporary nature.

Because of the differences with IFRS 16, this therefore means that where a subsidiary reports under FRS 102 at individual entity level, but the parent reports under IFRS at a group level, the accounting policies applied by the subsidiary and the group will likely differ and hence consolidation adjustments will likely be required when accounting for temporary Covid-19 rent concessions.

Effective date of the FRS 102 amendment

The original amendment applies to accounting periods beginning on or after 1 January 2020.

The June 2021 amendment is effective for accounting periods beginning on or after 1 January 2021, with early application permitted, therefore helpfully it can be applied to companies preparing their financial statements for 2021 year-ends.

Summation

The amendments to both IFRS 16 and FRS 102 are welcomed as they will alleviate the difficulties of accounting for rent concessions from leases by many. However, specifically for IFRS reporters, there will be questions on whether the measure that is applied is appropriate or whether the IASB has gone far enough and whether relief should be provided for lessors as well.

Both the FRC and the IASB have carved out a special measure in relation to lease payments affected by Covid-19 for a period of approximately one year and these measures certainly provide a short-term beneficial relief to help ensure that the cash flow benefits from the temporary rent concessions are more appropriately reflected in a company’s reported performance.

However, under IFRS 16, given that the complexity in accounting for lease modifications arises mainly from the determination of a current discount rate, a simpler amendment to IFRS 16, which perhaps would have been more consistent with existing requirements in the standard, may have been an exemption from the requirement to change the discount rate.

As to whether the FRC and IASB has gone far enough, part of the answer may depend on the resilience of the world in fighting Covid-19 but placing a definitive time period on affected lease payments may be unwise.