Regulatory Insights

Expert analysis on the latest regulatory insights in the UK.

Non-Performing Loans (NPL) are bank loans that have either been subject to late repayment by the borrower or unlikely to be repaid at all.

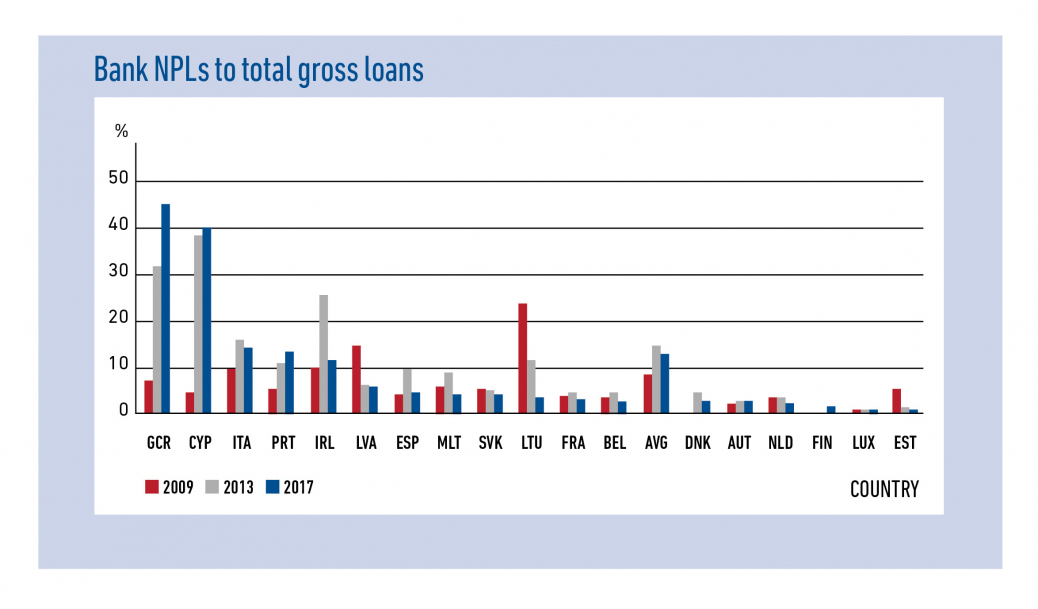

They are typically formed after crises or periods of low growth in weak financial ecosystems. For example, their emergence has been apparent in the Asian and Nordic financial crises of the 1990s, the US savings and loan (S&L) crisis in the 1980s as well as the Great Financial crisis in 2008 [1]. The last financial crisis had a big impact on borrowers’ ability to make repayments and, it was made worse by the following recessions in the EU zone. As a direct consequence, several countries built large stocks of NPLs. Some, such as Greece and Italy – having performed significantly worse compared to the rest, during the period of 2009 to 2013.

Among other things, high levels of NPLs can add constraints on balance-sheets, impact banks’ refinancing and lending ability, reduce banks’ profitability and even have a negative impact on national economic growth.

The below graph shows the evolution of the gross NPLs ratio (NPL / total gross loans ratio) of certain EU countries between 2009 and 2017.

Source: World Bank Data

Although the ratio of NPLs in EU banks has more than halved since 2014 [2], the total volume remains significant and, as a consequence, one of the main points of concern for European regulators who had to step in and impose stricter guidelines to tackle them.

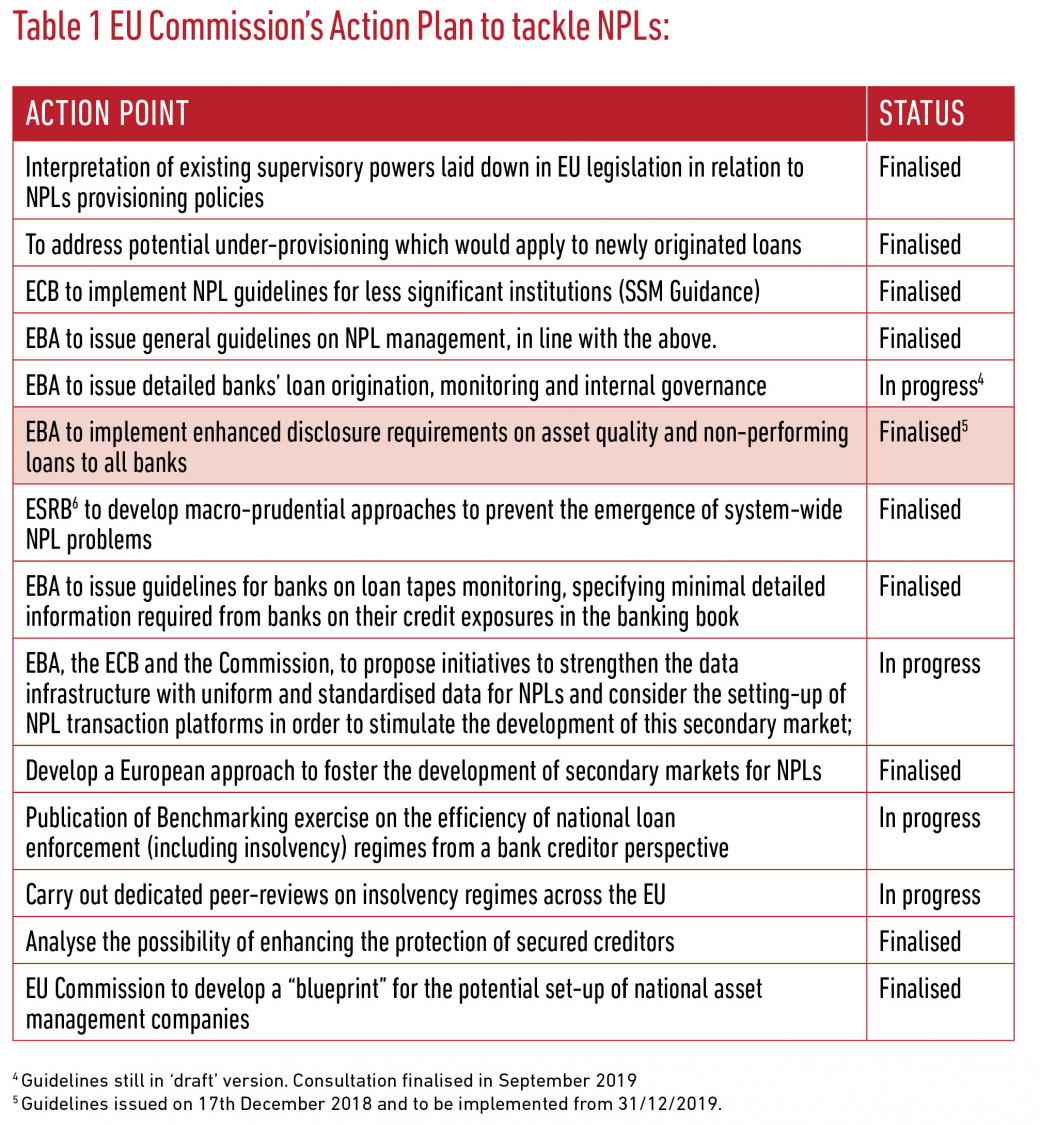

In particular, the European Council implemented an Action plan in July 2017. It was primarily set up to deal with the issue of the high volume of NPLs and track progress towards reducing the stock in the EU area.

Source: Economic Commentary – ‘Bad Loans’ and their effects on banks and financial stability by Olle Fredriksson and Niklas Frykstrom (14 March 2019) and EU Commission webpage: https://www.consilium.europa.eu/en/press/press-releases/2017/07/11/conclusions-non-performing-loans/

Among others, the action plan includes the development of 2 guidelines. One for the management and, one for the disclosure of non-performing and forborne exposures [6]. The latter requires financial institutions to disclose specific information to improve transparency on the quality of banks’ assets and, reduce information asymmetry among market participants.

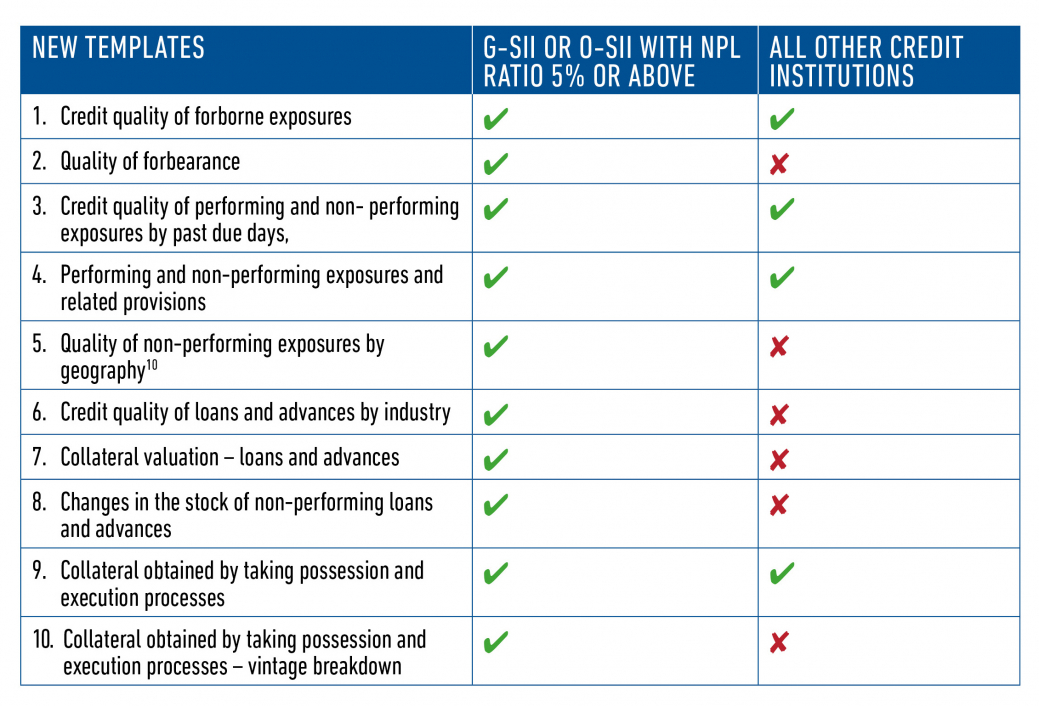

The main challenge is in this information being mostly new, compared to the current framework. In particular, the last set of guidelines [7] on disclosure requirements covered a broad range of areas (e.g. overview of Risk-Weighted Assets (RWAs) and credit risk management) and only slightly addressed Non-Performing and Forborne Exposures. In addition, in the new EBA Guidelines, an extra set of templates is required from institutions with a significant proportion of NPLs (gross NPL ratio of 5% or above).

Disclosing new information implies that it will be a challenge for financial institutions to fully align with these guidelines, as they will have to adjust existing internal processes.

From January 1, 2020, the Guidelines will replace two of the existing templates [8] (the Ageing of past-due exposures template and the Non-performing and forborne exposures one).

The following table provides an overview of the new templates required:

Firms considered as ‘global systemically important’ (G-SIIs) or as ‘other systemically important’ (O-SIIs) and those being characterised as ‘significant’ [9] should disclose these templates on a semi-annual basis (vs annual basis for other credit institutions).

Institutions should prepare the information to be disclosed according to the new EBA guidelines. They will be applicable in the EU State Members from 31st December 2019.

The EBA has tried to lighten up the burden on institutions, by clarifying that the relevant definition of NPEs is the EBA definition included in the ‘Implementing Technical Standards on Supervisory Reporting’. As such, institutions should already have their reporting systems ready to provide similar information. Nevertheless, most of the information is being requested for the first time. As a result, credit institutions will have to review their reporting process to ensure completeness and reliability of information provided, as well as consistency with other reporting requirements.

________________________________________________

Expert analysis on the latest regulatory insights in the UK.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.