National contact

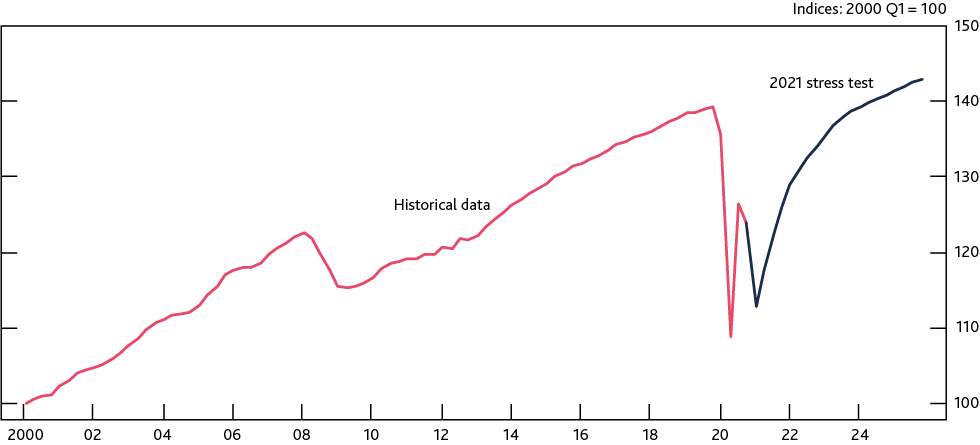

On 20 January 2021, the BoE published the details of their 2021 solvency stress test aimed to assess the major UK banks and building societies against a UK and global scenario that reflects a severe path for the current macroeconomic outlook.

Eight institutions are taking part in the 2021 solvency stress test, as these account for around 75% of lending to the UK real economy. These banks all have a diverse range of business models and some operate across a broad range of international markets. They are:

This year’s Stress Test will simulate a double dip fall in UK GDP, approximating to a further 9% fall in UK output in 2021 Q1.

Figure 1: Level of UK GDP (Source: Bank of England and ONS)

Banks will be asked to test the resilience of their end-2020 balance sheets against the below stresses:

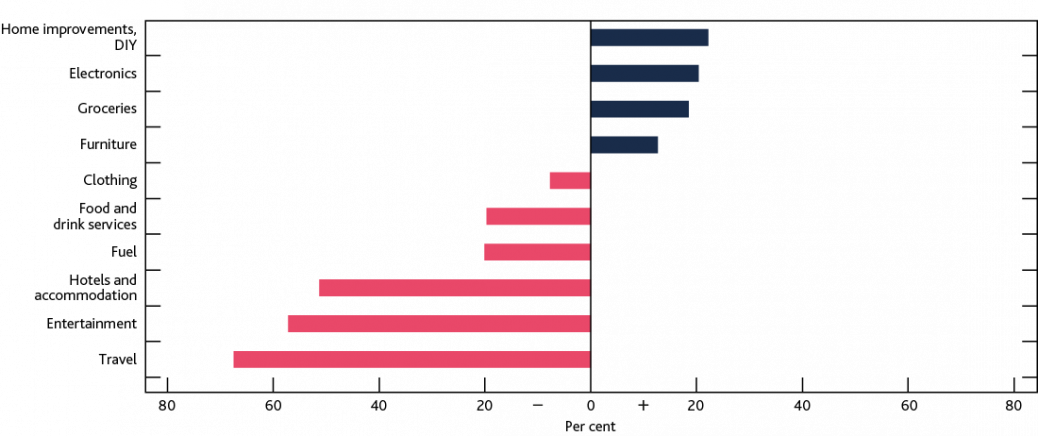

The BoE gives particular consideration to the risks associated with the changes to the economy in the past year. A key focus of the 2021 stress test will be to examine the potential risks to the UK banking system were these trends to continue and become more entrenched.

The stress scenario incorporates an intensification of these changes to the economy, assuming a weaker path for UK GDP in the longer term, driven by changes to consumer habits and production decisions.

Figure 2: Annual growth in spending in selected categories, 2020 Q4 (Source: Barclays and BoE Bank Calculations)

Globally, the scenario assumes weak world trade, with ongoing weaknesses particularly apparent in countries more exposed to vulnerable sectors and more reliant on tourism, high oil prices and/or have greater dependency on external finance.

The results of the 2021 solvency stress test will act as a cross-check on the FPC’s judgement of how severe the current stress would need to be in order to jeopardise banks’ resilience and challenge their ability to absorb losses and continue to lend.

The BoE has also stated that there will be no direct link from the results of the stress test to the regulatory response. However, the outcome of the test will be used:

The timetable for the 2021 solvency stress test will be staggered. As briefly mentioned above, participating banks will need to submit their projections for credit impairments and credit risk-weighted assets (RWAs) in April, instead of the usual deadline of June. The additional stressed projections will be submitted in June, as usual, with bank specific results to be published in Q4 2021.

To help with this change to the usual timetable, and due to the ongoing operational challenges within banks, participating banks will not be requested to submit baseline projections and the ring-fenced subgroups of stress-test participants will not be included in the 2021 tests.

The annual BoE stress test informs the setting of capital buffers by the FPC and the PRA. Firms that are not part of this annual stress test must carry out their own stress testing, and the participating banks will have to submit their findings in April. The PRA publishes a stressed scenario every six months to serve as a guide for banks and building societies designing their own scenarios. Every two years, the BoE also runs an additional scenario intended to probe the resilience of the banking system to risks that may not be precisely linked to the financial cycle – known as the biennial exploratory scenario.

The BoE’s approach to stress testing aims to build banks’ capital buffers up when the economy is growing, so that they can be drawn down during periods in which the economy is in stress. These stress tests are therefore designed to simulate the worst-case scenarios and assess how firms can cope with severe economic scenarios.

Expert analysis on the latest regulatory insights in the UK.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.