Want to know more?

28 January 2020

The main issue is ‘price-walking’. This is unfair price differentiation where insurers impose a “loyalty penalty” on existing customers by increasing renewal prices each year. As a result, customers who fail to switch end up paying higher prices than newer customers with similar risk and ‘cost to serve’ characteristics. The cost to serve is the actual cost incurred in providing the service to a customer (e.g. acquisition and claims handling overheads). This form of price differentiation tends to impact vulnerable groups such as elderly and low-income consumers who are less likely to shop around.

Pressure from Citizens Advice and the Competitions and Markets Authority prompted the regulator to increase its focus on pricing practices within the general insurance market. In response, the FCA developed its stance through its discussion of fair pricing and feedback (FS19/04), review of pricing practices in household insurance (TR18/4) and accompanying Dear CEO Letter. Most recently its pricing practices market study interim report (MS18/1.2) sets out a number of potential remedies.

The potential remedies include: restrictions on pricing practices, restricting or banning the use of auto-renewal thereby making it opt-in only and easier to decline, strengthening the product governance rules and improving communication with customers.

The FCA has already made some attempts to tackle this issue. For instance, the renewal disclosure rules mean that renewal quotes must now contain the price customers paid the previous year as well as the renewal price.

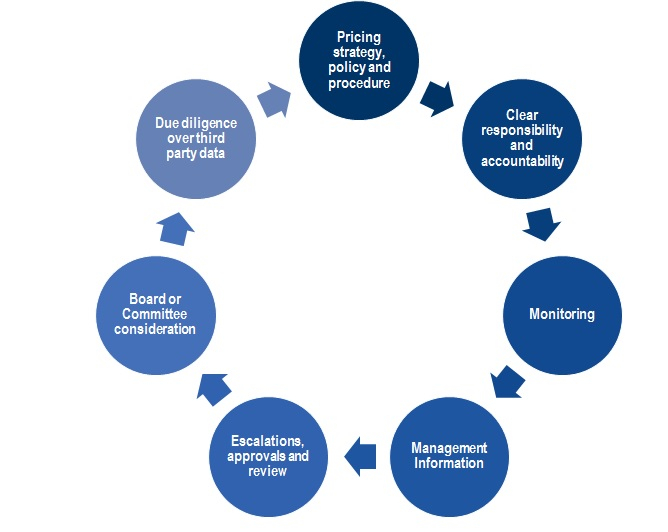

The existing requirements and expectations for firms are set out across the FCA Handbook, primarily from:

There is also a clear link to the FCA’s work on value in the General Insurance (GI) distribution chain and its GI value measures. Manufacturers are expected to consider the value their products present for the target market and the impact of the distribution chain on the overall value – this should include the price charged.

The FCA plans to publish its final market study report, alongside a consultation paper on any proposed remedies, in Q1 2020.

Our Regulatory Compliance team can address any questions or queries you may have, so please feel free to get in touch:

With a growing financial services practice, our team delivers tailored professional services to our asset management, banking and capital markets, insurance and real estate clients.

Mazars is a leading provider of audit and business advisory services with over a hundred years of experience within the insurance market, both in the UK and internationally. We began as specialist bookkeepers to Lloyd’s insurance market and we have evolved to become an important and recognised audit and advisory firm in the insurance industry.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.