Want to know more?

On 19 September 2018, the FCA and the PRA sent a letter to the Chief Executive Officers (CEOs) of the largest banks and insurance companies under their supervision. Through these “Dear CEO” letters the UK supervisors want to make sure that the firms’ senior management and board are fully aware of the key risks associated with the LIBOR reform and that the necessary actions will be taken in a timely manner. As a result, by mid-December 2018, these firms are expected to provide the regulators with a board-approved summary of the firm’s key risks assessment and actions planned to mitigate the identified risks as well as with the formal appointment of the senior manager(s) responsible for the implementation of the transition plan.

Some may think that these “Dear CEO” letters sound excessively alarmist as there is still a couple of years before the LIBOR discontinuation but that would be without understanding the widespread use of those IBORs across financial instruments such as derivatives, bonds, loans, deposit, securisations. Put it simply, those contracts linked to InterBank Offered Rates (IBORs) represent hundreds

and hundreds of trillions of dollars of outstanding volume overall (around $350 trillion of financial instruments tied to LIBOR).

One can easily understand why the UK supervisors want to ensure that its largest financial services players will be ready to move from the existing IBORs towards the new benchmarks – the so-called “alternative risk-free rates” (RFRs) – when the time will come. However the problem might not come from a lack of awareness or involvement from the industry but more from the magnitude of the

reform.

As previously mentioned, the magnitude comes from the range and volume of financial instruments but also, and as a consequence, from the diversity of economic players using them. The latter is as important as the former as it raises the question of the awareness among all the players. Surely, when it comes to issues related to IBORs or financial instruments, one can expect those issues to affect banks in first place. And indeed, these contracts constitute a large part, if not most, of their balance sheets. However, one should not forget that if banks use those financial instruments they also sell them to plenty of counterparts, banking or not.

Insurers are among those counterparts that use, quite importantly, IBORs-referenced instruments for investment purposes, hedging strategy (eg. interest rate and inflation swaps to cover pension’s schemes) or even as part of their valuation requirements. Indeed, the current regulatory discount rate imposed the European Insurance and Occupational Pensions Authority (EIOPA) to insurer’s liabilities is a risk-free rate based on LIBOR. Any change in the LIBOR will then result in a change in the value of the liabilities which will then lead to a necessary recalibration of the associated hedges.

Identical concerns can be raised for corporate companies who buy investment products pegged to IBORs (floatingrate notes tied to IBORs) or enter into derivatives contracts as part of their hedge strategy.

In order to illustrate the variety of impacts of the IBORs reform, let’s consider an example: the bonds referencing LIBOR and, in particular, those which mature beyond the end of 20211. In July 2018, the Working Group on Sterling Risk-Free Reference Rates issued a new paper regarding Sterling bonds referencing LIBOR and the associated risk that may arise from the index phasing-out . The first risk identified was the potential switch from a floating-rate bond to a fixed-rate one. This risk could be triggered if reference banks were to stop providing quotes after 2021 and if it becomes impossible to determine the interest rates from any fallback. In such a situation, the ultimate fallback would result in using the last determined rate for the rest of the bond’s life-time which will have consequences on the investors as on the issuers. For the former, fixed-rate bonds might lose their initial appeal as they would become illiquid and might be less attractive in terms of coupon. For the latter, the switch might raise new risks in terms of Assets and Liabilities or Treasury Management and new needs in terms of hedging strategy. Indeed, floating-rate bonds issuance as investments can be associated with specific hedging strategies through derivative contracts. With the LIBOR disappearing, derivative contracts (hedging instruments) and bonds (hedged items) will be subject to specific and probably different fallbacks which might also be triggered at different times. This can cause a cash-flows mismatch which may then result in additional funding costs for the issuers, unexpected profits and losses or even in the disruption of the hedge effectiveness. Obviously, investors could face the same risk with their own hedging strategies.

Triggering any fallback or even switching from floating to fixed-rate bonds implies a strong prerequisite: the prior bondholder’s consent (individual or quorum) to any amendments to the current terms and conditions of the bond notes. This can prove to be a quite difficult task: depending on the revised conditions and bondholders may or may not be willing to accept the new terms. A correlated risk to this is the litigation risk. Indeed, a switch from floating to fixed rate, or even a switch from LIBOR to an alternative fallback, might end up in a loss for the investors and with it an increased risk of litigation for mis-selling. Through the floating-rate bond example, one can observe many types of risks and strategic questions that might arise. Now, let’s keep in mind the volume at stake, out of the $350 million (or more) notional value of LIBOR-linked contract: 80% are Over-The-Counter (OTC) and Exchange-Traded derivatives2 while bonds belong to the remaining 20%3.

Through derivatives, the modelling and risk management challenges brought by the reform are yet more apparent than in the aforementioned example.

Indeed, using RFRs means new curves and hence new term structures to be built for each of these new rates. During the transition period in particular, basis spreads with the existing IBOR curves will need to be assessed and monitored for each currency and each tenor. Specific controls will have to be implemented and potential IT adaptations might be required in order to enable this multicurve management and monitoring. Modelling issues have a direct impact on the valuation of the IBOR-references instrument and, in fine, a financial impact.

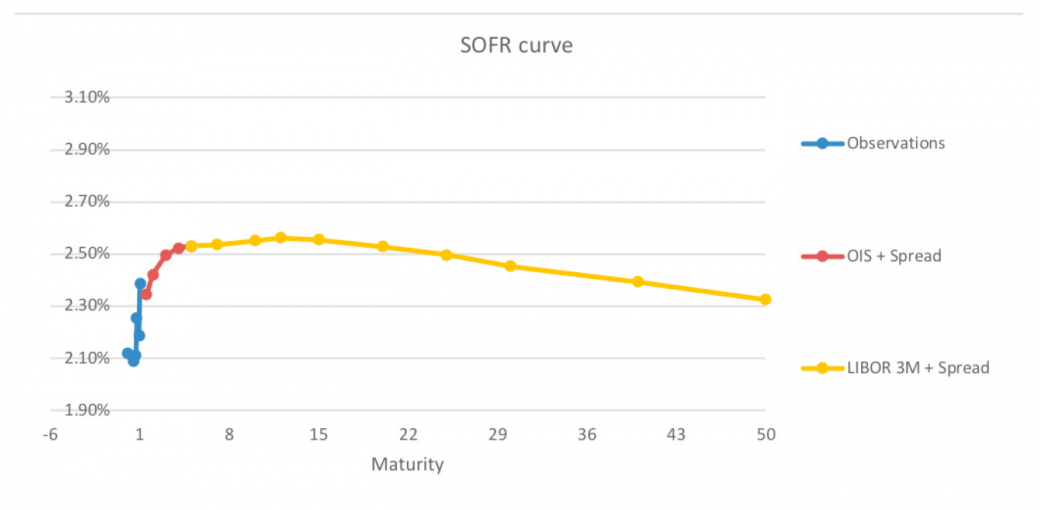

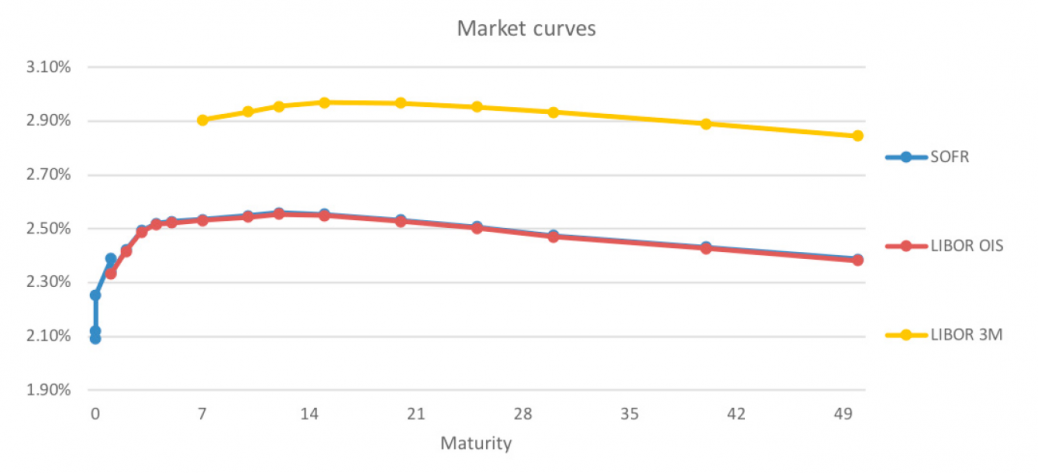

While the first SOFR OTC swap happened in July 2018, there is no convention set up for SOFR curve structure yet. At the moment, the SOFR market curve is not something anyone can rely on as it is based (FED fund rate) and add-on. The below SOFR curve has been built based on market observations (0-18 months), OIS curves (18 months-7 years) and LIBOR 3M (7 years and beyond) to which spreads have been applied.

In this example, a 40% gap would be observed between the fair-value of a swap LIBOR 3M/Fixed rate and the fair-value of a swap SOFR / Fixed rate – assuming a 2% fixed rate.

Beyond the valuation impact, a very important point in the above example is the current absence of observability of the SOFR market curve (in particular beyond m18 months) which may result in significant regulatory implications, in particular in light of the revised minimum capital requirements for markets risks and the punitive regime that will be applied to non-modellable risk factors.

The extent of the IBORs reform will certainly shake the financial and economic sphere. Risks to be taken into account are widespread across all economic players and the clock is ticking. Perhaps is it ticking faster than anticipated as the possibility of a hard Brexit scenario could jeopardise the LIBOR status within the European Union under the new Europe’s Benchmark Regulation (that will enter into force in 20201). Overall it might not be an understatement to say that this reform puts financial stability at risk and preparing for the transition is not an option, it is an emergency.

13 November 2018

Paving the way for transition towards an IBOR-free world.

The latest IBOR related insights and analysis

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.